Central Casting

Trump’s pick for Fed Chair has a vision for the central bank that could reshape markets; but does reality care about his vision?

On January 30th, President Trump announced his nominee for the most powerful unelected position in global finance. The pick: Kevin Warsh, a 55 year old former Fed Governor, Morgan Stanley dealmaker, and longtime partner at Stanley Druckenmiller’s Duquesne Family Office. Trump, never one to miss a branding opportunity, called him “central casting” for the role. Markets went haywire. Gold cratered 9% in a single session, its worst day since 2013; the dollar ripped 0.85% higher; and equities wobbled as traders scrambled to re-price the entire rate path under a new regime.

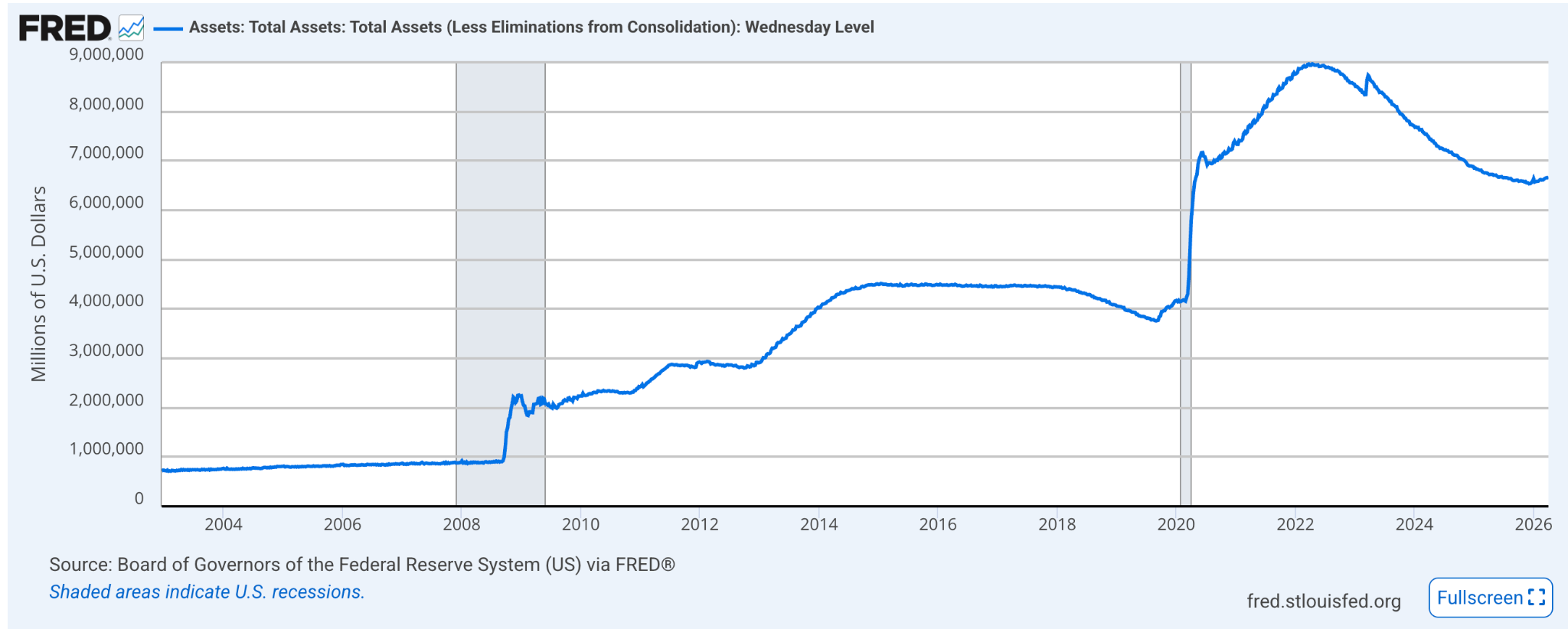

For those of you who have followed my work, you know I’ve been tracking the Fed’s slow march toward fiscal dominance: the point at which monetary policy becomes subservient to the Treasury’s financing needs. As I laid out in The Quiet Pivot and Not So Stealthy QE, the Fed has been drifting in this direction for years, whether it admits it or not. The $6.7 trillion balance sheet sitting at the Eccles Building right now is the physical manifestation of that drift. And now a man who has spent fifteen years railing against exactly this kind of institutional bloat is about to inherit the whole mess.

The question isn’t whether Warsh wants to shrink the balance sheet and restore what he calls a “narrow central bank.” He clearly does. The question is whether the math will let him.

Source: FRED, Federal Reserve Bank of St. Louis

Warsh’s biography reads like it was engineered in a lab to produce a Fed Chairman. He was first a Stanford undergrad, and graduated Harvard Law cum laude, before doing additional coursework at MIT Sloan and Harvard Business School. Then, he did seven years in Morgan Stanley’s M&A department before joining the Bush White House as Special Assistant to the President for Economic Policy. In January 2006, President Bush nominated him to the Board of Governors of the Federal Reserve. He was 35 years old: the youngest governor in the Fed’s history.

SPONSOR:

Bitcoin is freedom money, but only if you control your keys.

Partnering with Bitcoin Well, the world’s first publicly traded non-custodial Bitcoin company, ensures this freedom.

They send Bitcoin directly and instantly to your wallet.

No middlemen. No permission needed. Whether you’re stacking sats or making large moves via their OTC desk (Infinite by Bitcoin Well), you remain in control. Self-custody is essential.

Ready to buy Bitcoin the way it was intended? Head to bitcoinwell.com and enable your independence. Use this link https://app.bitcoinwell.com/signup?referral=peruvianbull to sign up and start stacking today!

Now let’s get back to it!

Less than two years later, the global financial system was in free fall. Warsh became Bernanke’s primary liaison to Wall Street during the 2008 crisis, the man shuttling between the Eccles Building and lower Manhattan trying to figure out which institutions were arguing their book and which were delivering real intelligence. At a March 2008 FOMC meeting, Warsh warned that

“the business model of investment banks has been threatened, and I suspect the existing business model will not endure through this period.”

That was six months before Lehman.

But here’s what matters for forecasting the kind of Fed Chair he’ll be. Throughout 2008, even as the system melted down, Warsh kept warning about inflation.

March:

“On the inflation front, there is little reason to be confident that inflation will decline.” June: “Inflation risks continue to predominate.”

September, with Lehman’s corpse barely cold:

“I’m still not ready to relinquish my concerns on the inflation front.”

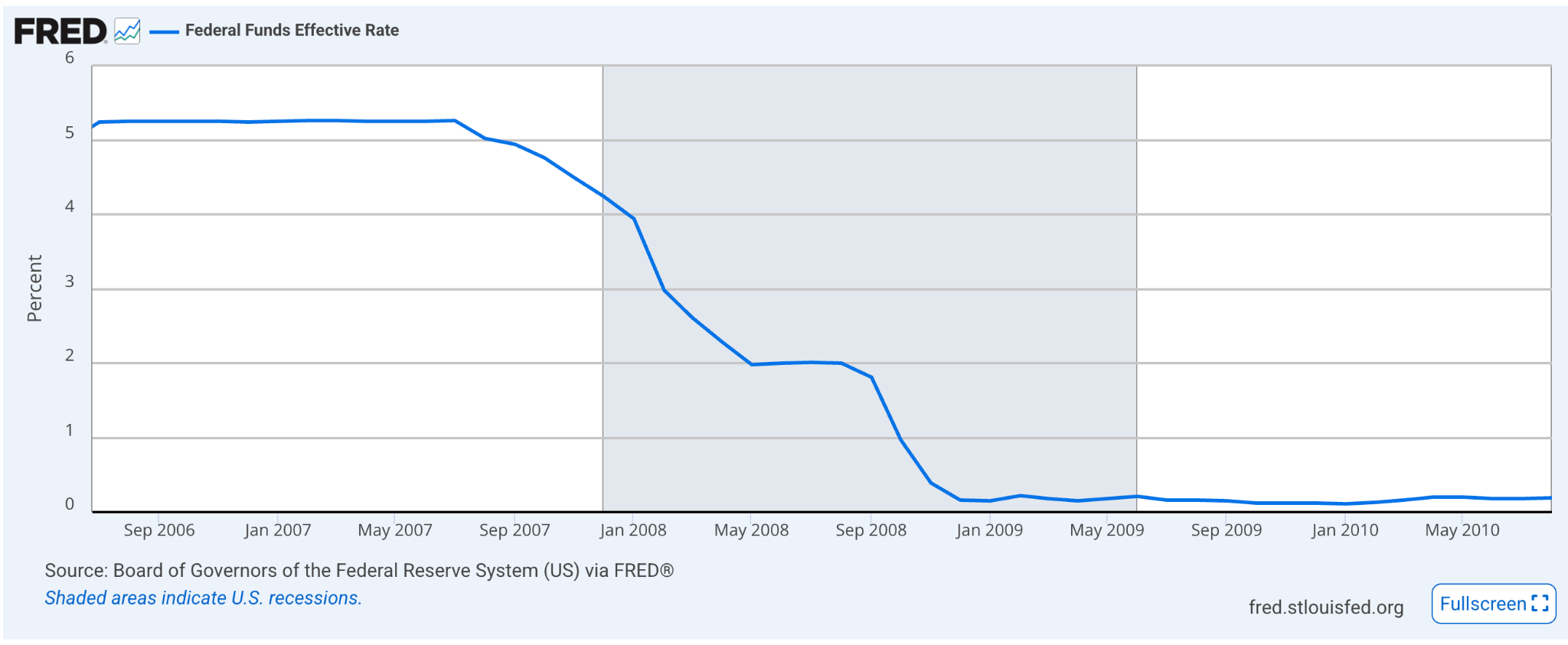

He supported the initial crisis interventions: the emergency facilities, the first round of asset purchases, and the doubling of the balance sheet from $1 trillion to $2 trillion. He backed the firefighting. What he could not stomach was what came after.

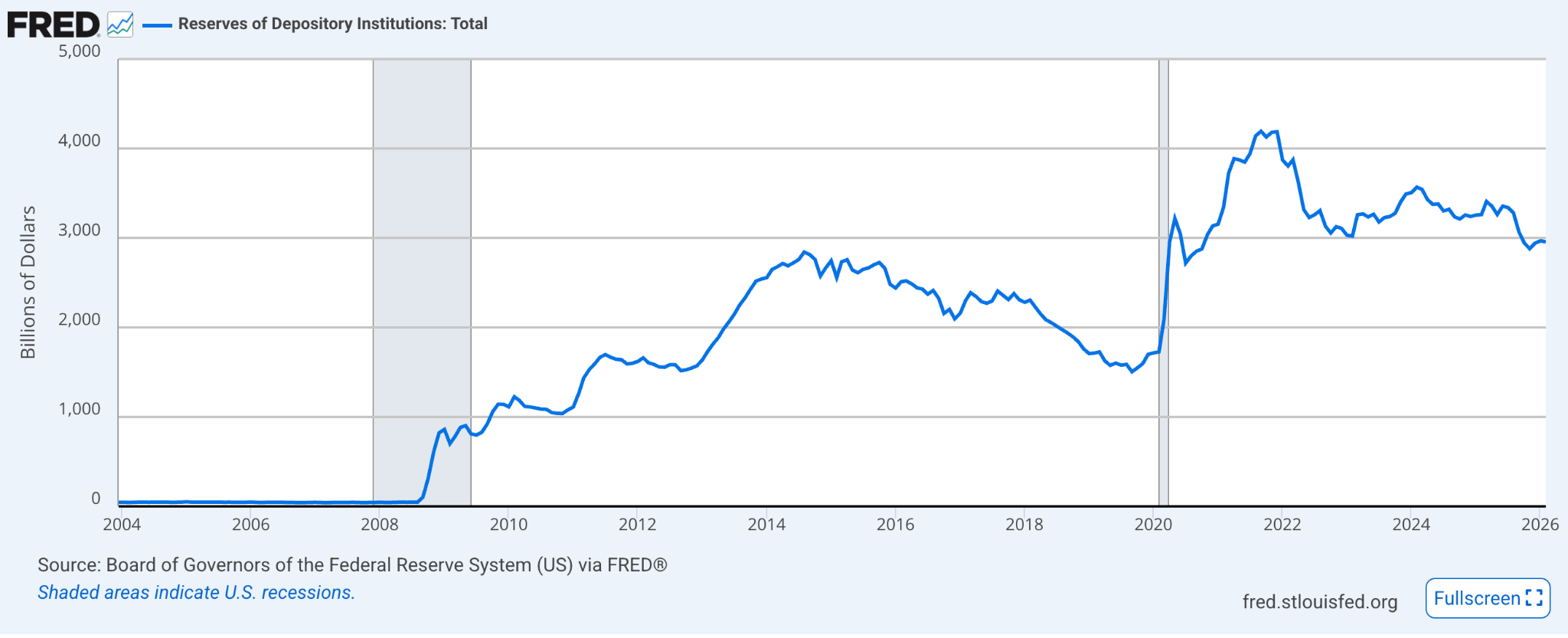

Source: FRED, Federal Reserve Bank of St. Louis

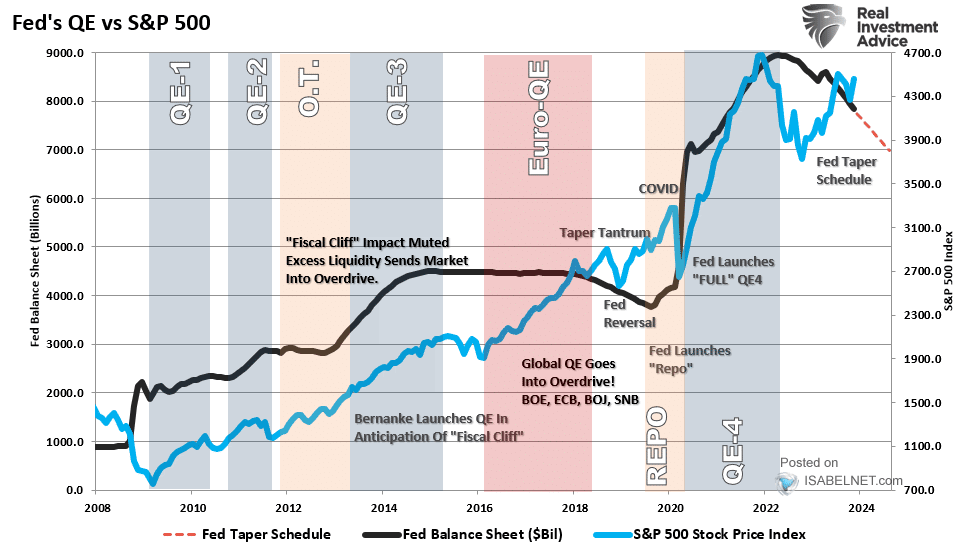

When the crisis passed and markets stabilized into 2010, Warsh expected the Fed to retrace its steps. Instead, the FOMC began debating QE2. Warsh was deeply opposed. As Bernanke wrote, Warsh believed that “monetary policy was reaching its limits, that additional purchases could pose risks to inflation and financial stability.” He worried that buying Treasuries in a period of relative stability would blur the line between monetary and fiscal policy, turning the Fed into a financing arm of the federal government.

History vindicated the concern. QE became what Warsh later called “a near permanent feature of central bank power and policy.” The balance sheet went from $2 trillion to nearly $9 trillion. Congress added $5 trillion in cumulative deficits during a period of relatively full employment; free money is a hell of a drug. Warsh resigned in spring 2011, delivering the line that would define his post-Fed identity: “In my view, forays far afield, for all seasons and all reasons, have led to systematic errors in the conduct of macroeconomic policy.”

He walked out at 41 with a clear thesis: the Fed had become too big, too powerful, and too enmeshed in fiscal policy. He spent the next fifteen years making that case, first as a partner at Druckenmiller’s Duquesne Family Office (where he sat alongside the world’s most famous deficit hawk for over a decade), and simultaneously at Stanford’s Hoover Institution, where he issued an independent report on monetary policy reform to the Bank of England that Parliament actually adopted.

The Druckenmiller connection matters enormously. Druckenmiller publicly warns constantly about runaway fiscal deficits and the moral hazard of permanent QE; he deeply admires Volcker. Scott Bessent, now Treasury Secretary, is also a Druckenmiller protégé from their Quantum Fund days. Druckenmiller has said he’s “excited about the partnership between [Warsh] and Bessent.” Ray Dalio called the pick “a great choice.” So you have a future Fed Chair who spent 13 years as a macro investor alongside the world’s most famous deficit hawk, about to work in tandem with a Treasury Secretary trained by the same man. That is not an accident. That is a worldview.

One more connection worth noting: Warsh is married to Jane Lauder, granddaughter of Estée Lauder and daughter of Ronald Lauder, who has been a close friend of Trump’s since they were undergraduates together at Wharton. Ronald Lauder donated $5 million to MAGA Inc. Make of that what you will.

The conventional wisdom is that Warsh is a hawk. Citadel Securities identified 13 speeches during his Fed tenure expressing concern about upside risks to inflation, which is striking because core PCE was rarely above 2.5% during that period while unemployment hit 10%.

But Warsh 2026 is not Warsh 2010. He now believes that AI will drive a massive productivity surge allowing strong growth without inflation. As Druckenmiller said on announcement day: “Kevin right now very much believes you can have growth without inflation... He’s very open minded to the so-called Greenspan view.”

This is the key. He’s proposing something more radical than simple hawkishness or dovishness: lower rates AND a dramatically smaller balance sheet. Cut the price of overnight money while pulling the Fed’s footprint out of the Treasury market. Allianz Trade’s research team summarized it precisely: Warsh combines “a dovish view on interest rates with a hawkish approach to the Fed’s balance sheet, which could drain liquidity from a highly leveraged financial system.” He has argued publicly for transitioning from the current “ample reserves” framework back toward “scarce reserves”: effectively rewinding to the pre-GFC monetary architecture.

For readers of this Substack, you know what the balance sheet means for asset prices. As I laid out in Net Liquidity, if you divide the S&P 500’s performance by the Fed’s balance sheet since the GFC, the line is basically flat: no real growth in stock prices since 2008, just money printing.

Warsh wants to reverse this. And that is a MUCH bigger deal than where the overnight rate sits.

Source: FRED, Federal Reserve Bank of St. Louis

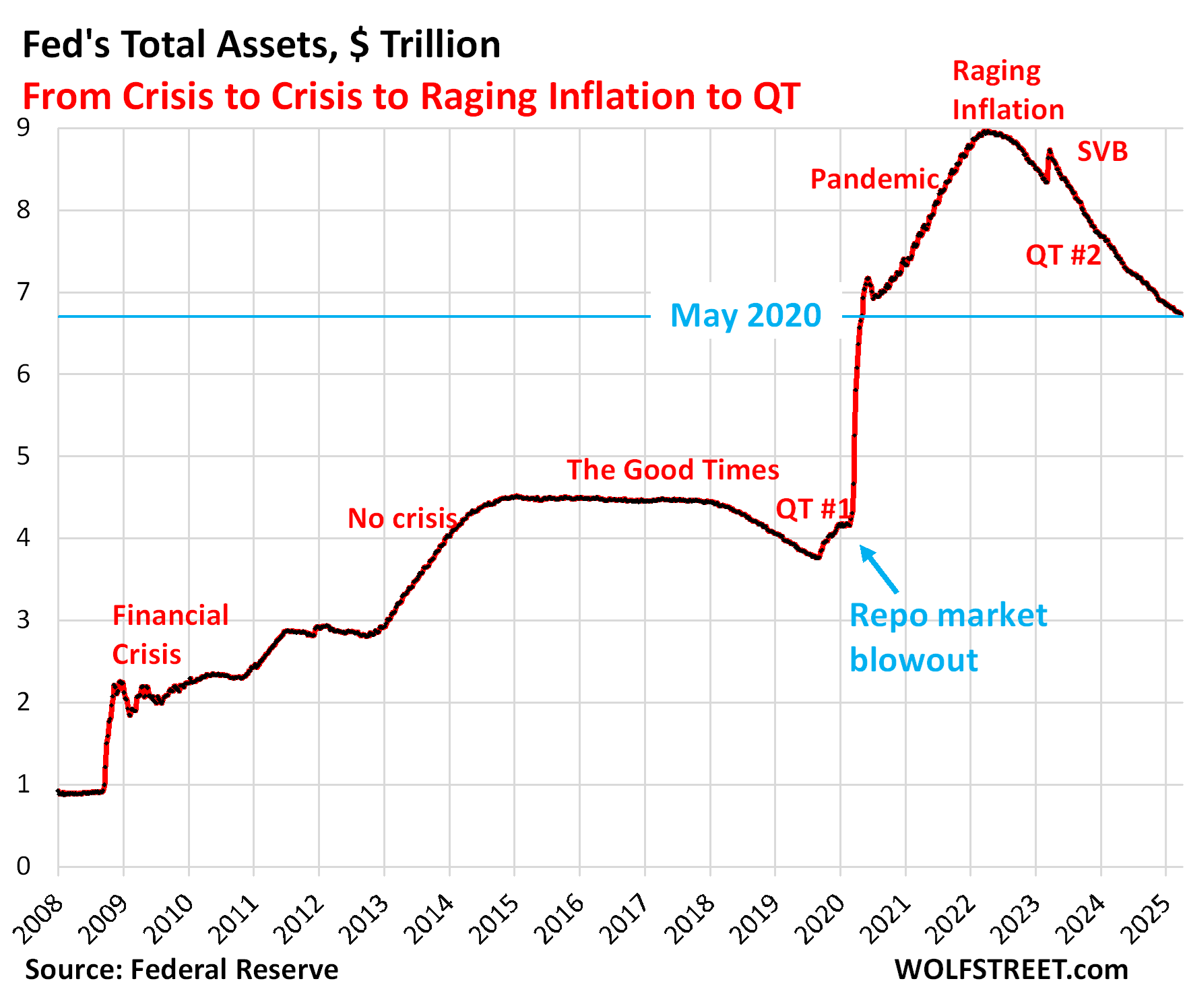

The Fed’s balance sheet at $6.7 trillion is, as Dallas Fed President Lorie Logan noted last week, still 21% of GDP: down from a post-pandemic peak of 35% but well above the pre-pandemic 19%. Warsh’s diagnosis that the Fed has become too large a player in financial markets is shared by serious people across the political spectrum. But diagnosis is not prescription.

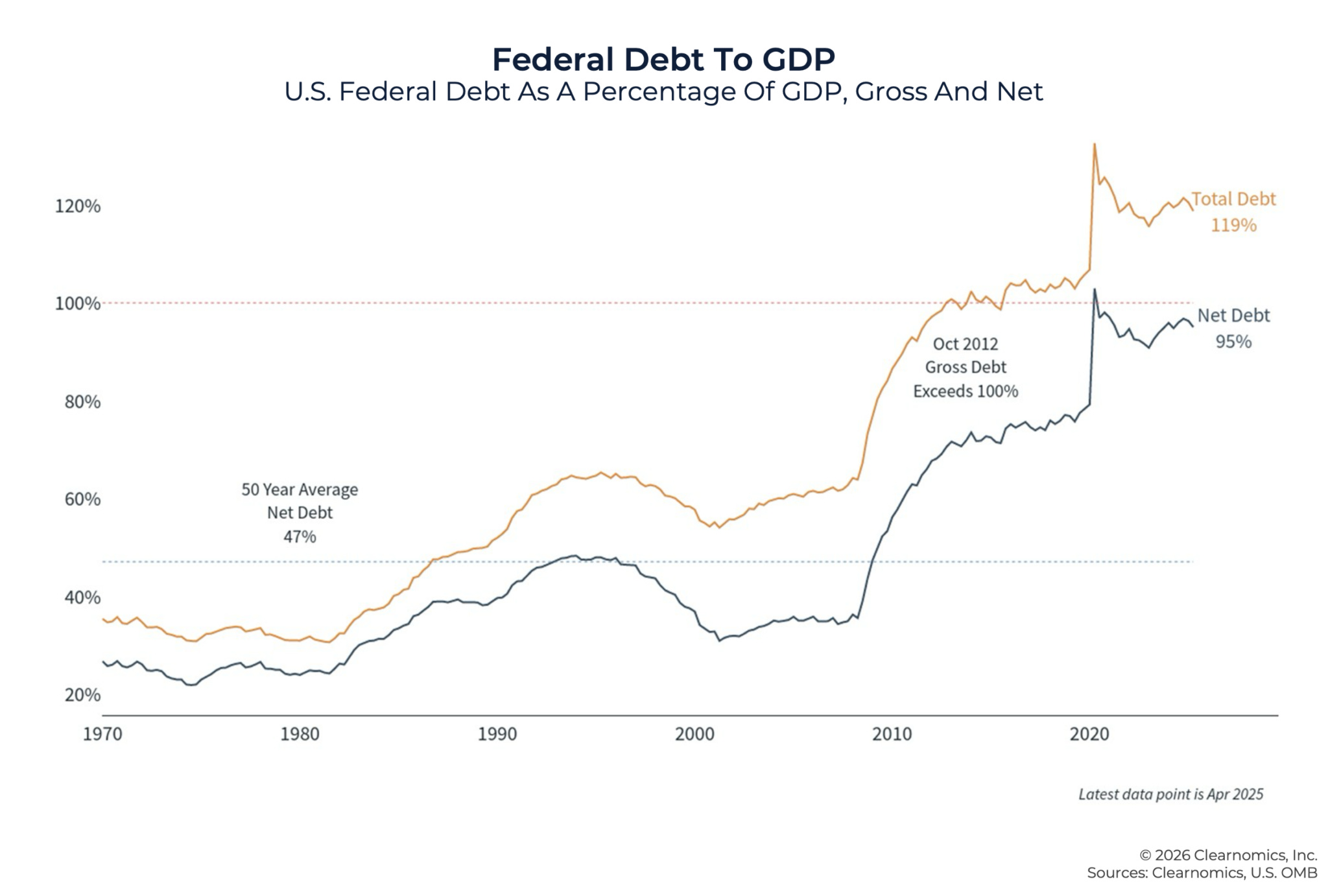

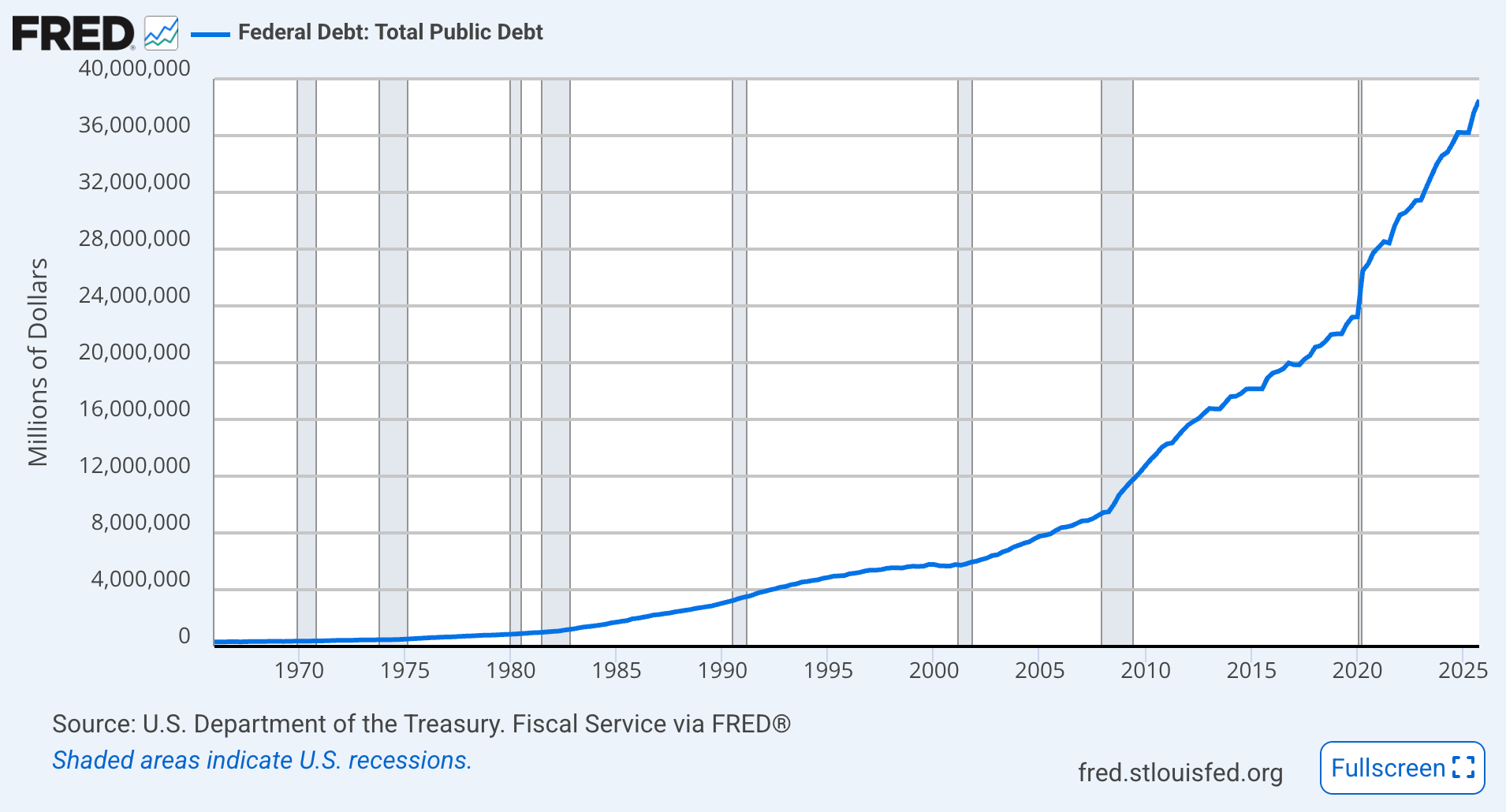

Here’s where the Dollar Endgame thesis collides directly with the Warsh vision. Federal debt is approaching $40 trillion. Annual interest costs run roughly $1.6 trillion. The Treasury borrows close to a trillion dollars every quarter. We’ve crossed the Rubicon into fiscal dominance, though nobody wants to admit it.

If the Fed stops absorbing Treasuries, someone else has to. With foreign central banks rotating out of long duration US debt and domestic institutional demand structurally constrained, pulling the Fed’s bid at the exact moment the Treasury is issuing record quantities of new debt is a recipe for a bond market dislocation. Dallas Fed researchers published an essay last week showing that returning to scarce reserves would mean running reserves from 9.5% of GDP to below 7%: the level that triggered the 2019 repo market meltdown. They warned that “episodes of money market volatility will likely become more frequent.”

The math doesn’t care about your monetary philosophy. Drain $3 trillion in reserves while the Treasury issues $8 trillion in gross debt over four years, and something gives. Either yields spike (destroying Warsh’s rate-cutting ambitions and blowing up the deficit through higher interest costs), or the Fed quietly reverses course (destroying Warsh’s credibility). The balance sheet is not a policy choice anymore. It’s a load-bearing wall.

Source: US Treasury / FRED

None of this matters yet, because Warsh isn’t confirmed. The Senate Banking Committee hearing is set for April 16, eight days from now. But Republican Senator Thom Tillis has vowed to block the nomination until the DOJ drops its criminal investigation of Jerome Powell over the Fed’s $2.5 billion headquarters renovation. Republicans hold a 13-11 committee majority; all Democrats are opposed; Tillis voting no deadlocks it. He’s retiring in January 2027 with zero incentive to cave.

Powell’s term as Chair expires May 15. He has said he’ll stay on until Warsh is confirmed, but if the probe drags on, we get a zombie leadership situation: a lame duck Chair presiding over a central bank everyone knows is about to change hands. Trump joked at the Alfalfa dinner that he’d sue Warsh if rates didn’t come down. Senator Warren asked Bessent whether Warsh would be investigated by DOJ for not cutting rates at Trump’s direction. Bessent’s answer: “That is up to the President.”

Not exactly a ringing endorsement of Fed independence.

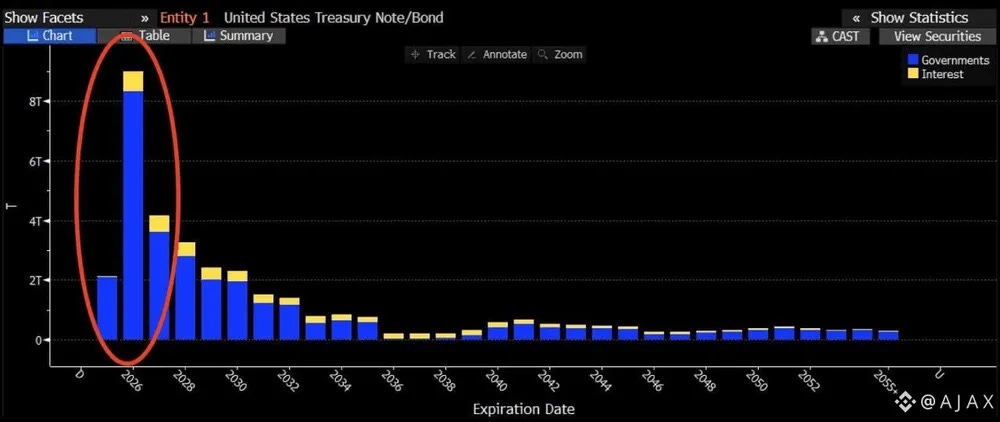

And it’s no wonder. There’s over $8 trillion of marketable debt rolling over this year, far exceeding anything coming for the next decade. Trump needs lower rates now.

Source: US Treasury, Quarterly Refunding Statements

But, the near-term rate path changes very little. Markets price two to three cuts in H2 2026, bringing fed funds from 3.5%–3.75% to roughly 2.75%–3.0%. The Iran oil shock may push the timeline out; Allianz Trade now expects September rather than June. But the direction is clear.

The bigger deal is the balance sheet. Sustained QT at a time of historic Treasury issuance is a direct collision course with fiscal dominance. Banks and financials should outperform initially; a steeper yield curve plus rolled-back Basel III Endgame capital requirements is the dream setup for net interest margins. Rate-sensitive sectors get more complicated: if the long end keeps rising because the Fed is pulling its bid, mortgage rates could go UP even as the overnight rate falls.

Gold got slaughtered on announcement day, and the logic was straightforward: a credible, hawkish-sounding chair reduces the perceived probability of imminent money printing. But for readers of this Substack, I’d caution against reading too much into the move.

The structural case for gold has nothing to do with who sits in the Fed Chair. It has to do with the $39 trillion in debt, the $1.6 trillion in annual interest costs, and the impossibility of growing your way out of a debt spiral when the government is the largest debtor in the system. Warsh may slow the timeline, but he cannot change the destination.

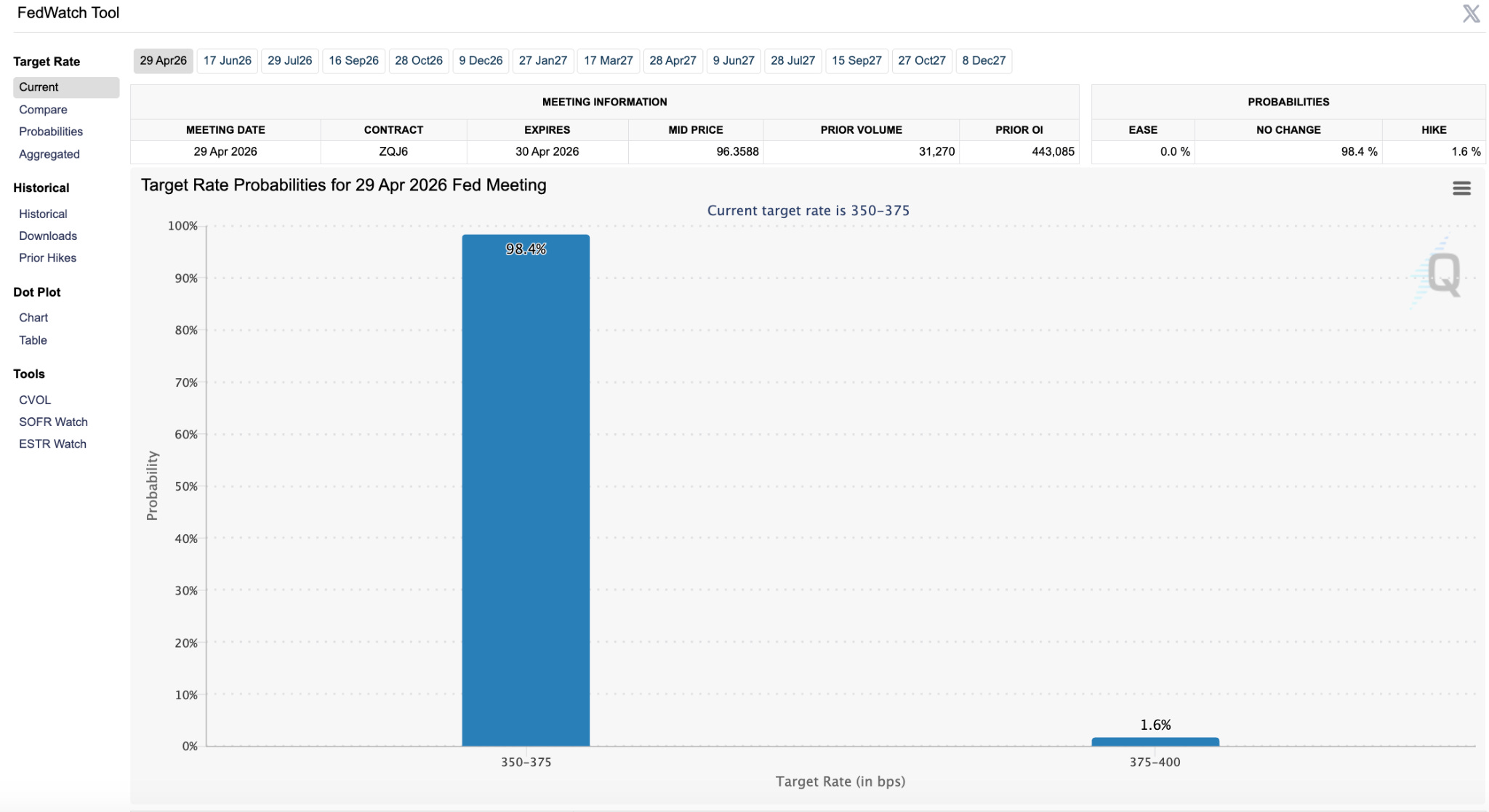

Source: CME FedWatch / Federal Reserve

Every Fed Chair enters the Eccles Building with a philosophy, and every one of them eventually has to choose between that philosophy and the market’s veto power. Greenspan came in as a gold standard sympathizer and left as the architect of the Greenspan Put. Bernanke came in as a deflation expert and left having created permanent QE. Powell came in as a balance-sheet hawk and left having presided over the largest monetary expansion in history.

Warsh has been inside the Fed before, and he left because he didn’t like what it was becoming. He’s had fifteen years to sharpen his framework. But the constraints are the constraints.

The latest definition of inflation is the rate at which the Fed steals your money.

Such a good read, this is vital stuff to know about!