China's Gamble

Will China devalue to prop up their faltering real estate market?

China, the world’s second-largest economy, is at a critical juncture. Over the past two decades, the country’s rapid rise has been fueled by debt, industrialization, and export-driven growth. Chinese Premier Xi Xingping has been at the forefront of this economic revolution, pushing for increased investment in infrastructure, manufacturing, and most importantly- real estate.

But the cracks in this bubble are becoming increasingly visible. Sluggish GDP growth, plummeting bond yields, and a collapsing real estate sector are all signs of an economy under extreme duress. Meanwhile, the yuan is under immense pressure, hovering near multi-year lows against the dollar, as capital flows out of the country at an alarming pace.

As I’ve written extensively in China’s Hidden Banking Crisis and China Teeters, the country’s economic troubles are rooted in a deeper structural problem: an over-leveraged system running out of willing borrowers. Over the past 15 years, Beijing has leaned on three successive engines of debt-fueled growth—corporates, households, and now the government. Yet, as each of these drivers has reached its limits, the options for stabilizing the economy have narrowed. Today, the People’s Bank of China (PBOC) faces a terrifying choice: defend the yuan at the cost of depleting foreign reserves or allow a controlled devaluation that risks exacerbating capital flight.

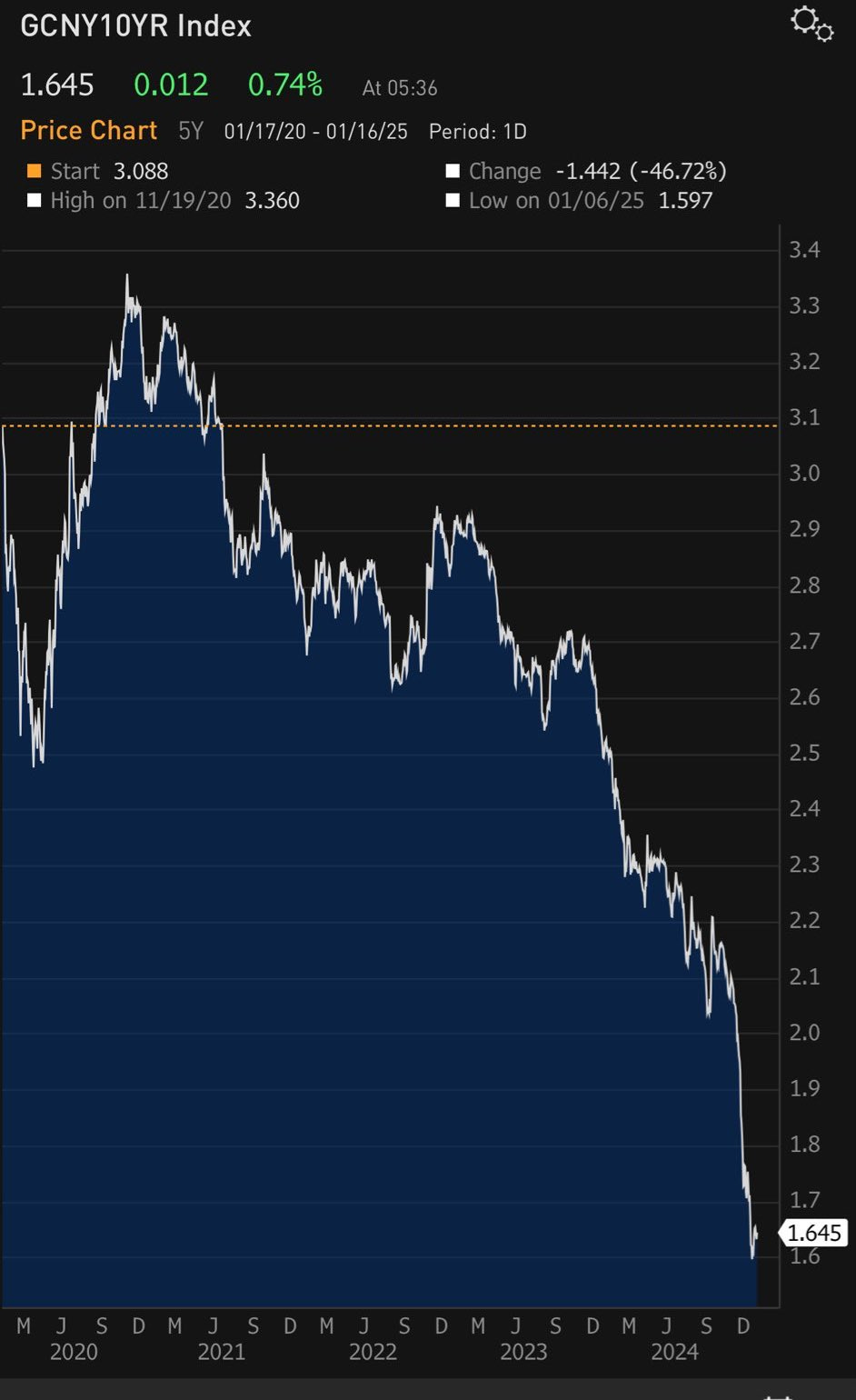

Right now, the Chinese bond market is flashing warning signs of deflation, as yields on 10-year government bonds dip below 2.6%. This stands in stark contrast to U.S. Treasuries, which yield over 4%, creating a nearly 3% spread that is driving investors to exit Chinese assets. Kyle Bass, noted hedge fund manager and China analyst, tweeted this on Jan 16th:

He included the following chart, which I had to cut and crop separately since the image was too big:

The panic in the bond market is setting in as investors are flocking to government bonds as a safe haven asset. However, the purchases of state debt aren’t a stamp of approval on the fiscal stability of the CCP or its creditworthiness, rather the widespread belief on the ground is that the PBOC will have to begin large-scale liquidity injections and the first place it will go to buy securities is the government credit markets. Participants are simply front-running their central bank.

The real estate market, which accounts for an estimated 70% of household wealth, is in freefall, further dampening consumer confidence. Amid these headwinds, the PBOC’s repeated interventions to prop up the yuan and stabilize markets appear increasingly futile.

As covered in China Unleashes a Liquidity Wave, Beijing has rolled out its largest monetary stimulus since COVID-19 to counteract these pressures. The PBOC slashed reserve requirements and key interest rates, injecting over 1 trillion yuan ($142 billion USD) into the banking system through "stealth easing." To prop up the crumbling real estate market, mortgage rates were cut, down payment requirements were lowered, and funding for converting unsold housing into affordable units was expanded.

Yet, even with these interventions, the real estate crisis persists. Developers like Evergrande and Country Garden are facing severe liquidity crunches, and a massive 48 million pre-sold homes remain unfinished, threatening the financial stability of millions. Since 70% of household savings is tied up in real estate, consumer confidence has taken a major hit.

Beyond housing, China is also pouring liquidity into its stock market, introducing a 500 billion yuan swap program and 300 billion yuan in low-interest loans for share purchases. These efforts triggered a historic market rally, with the Shanghai Composite surging 8% in a single day, its largest jump since 2008.

While these moves have temporarily boosted investor sentiment, deep structural imbalances remain. The question now is whether Beijing’s stimulus measures can genuinely revive growth—or if they are merely delaying an inevitable reckoning.

SPONSOR: I’ve talked a lot about the value of Bitcoin and its use case as fiat currencies inflate away. As such, I'm proud to have Onramp as a sponsor supporting this newsletter, a firm at the forefront of pioneering a trust-minimized form of Bitcoin custody.

With Onramp Multi-Institution Custody, assets live in a segregated, cold-storage, multi-sig vault controlled by three distinct entities, none of which have unilateral control.

To learn more about Onramp's custody solutions, and financial services like inheritance planning, connect with their team or schedule a consultation. You can use this link to get a discount on their services.

Now let’s get back to it!

The Three Phases of Chinese Leverage

China’s economy has long relied on leverage to fuel its meteoric rise, but the nature of that leverage has shifted over time—and not in a sustainable direction. As MacroAlf highlighted in a detailed thread, China’s debt-driven growth has unfolded in three distinct phases, each more precarious than the last.

The first phase, spanning from 2010 to 2016, was powered by corporate borrowing. Massive investments in infrastructure and industrial expansion drove GDP growth, but it came at the cost of ballooning corporate debt. By 2016, corporate leverage had reached unsustainable levels, forcing the government to pivot.

Keep reading with a 7-day free trial

Subscribe to The Dollar Endgame to keep reading this post and get 7 days of free access to the full post archives.