Endgame #2

More currency shenanigans in China and Japan; the US bond market rout worsens

Welcome to Endgame, the short monthly newsletter covering the biggest events in macro and how they tie into the Dollar Endgame. Let’s get started.

Japan

Japan’s currency issues continue to worsen this month, with USD/JPY crossing 148 and nearing the 150 redline where the Bank of Japan intervened last year. Despite several moves to alleviate the pressure, including raising the cap on the 10yr JGB in their program of Yield Curve Control back in July, the market has continued to lay on pressure on the Yen, testing Ueda’s resolve to hold the line on the currency at the same time it attempts to cap yields in the bond markets.

This is critical for Japan as they are dealing with mounting debt costs and immense pressure in their bond market, which has been testing the cap on the 10yr yield. The Bank of Japan already owns 60% or more of certain issuances of government debt, and each test of the cap increases this figure.

Market participants are patiently waiting for another intervention. When it will come is anyone’s guess, but likely 150 is the redline that the BoJ will not accept as this is where it repeatedly defended the currency last year. Either way, understanding what happens with the Yen moving forward is key to global markets. Japan has almost a trillion dollars worth of US Treasuries, and around $100B in a capital account in USD. If they are forced to defend the cap, this means selling US government bonds in the face of falling bond prices, pushing domestic interest rates even higher.

Brent Johnson, MacroVoices Interview, August 31st, 2023:

“In many ways, I think the Yen is the key to everything. But what the Yen is doing right now is, as it weakens, it puts an incredible amount of pressure on China, which is not only a regional trading partner but also a regional trading competitor. And as Japanese goods get cheaper in yen terms, it puts pressure, it makes it easier for foreigners to buy Japanese goods than to choose Chinese goods. And China's already dealing with some severe deflationary pressures in their real estate market. I think we're getting to the point where China is going to have to seriously consider either bailing out their entire real estate market or implementing some other programs to help it, and that would lead to the yuan weakening, I believe.”

On Friday, September 22nd, the Bank of Japan reaffirmed its commitment to ultra-low interest rates and its determination to continue supporting the economy until inflation consistently reaches the 2% target. Governor Ueda indicated that the bank does not have immediate plans to scale back its substantial stimulus program. Further exacerbating the issue was the recent FOMC meeting where the Fed decided to pause interest rate hikes, but Powell indicated that he may hike rates further should economic data come in strong and inflation remain elevated.

This put further pressure on the Yen as the low interest rates held in Japan means that carry trades will continue to be put on, pressuring Yen lower and pulling USD higher. Carry trades have already been covered here, but basically they happen when investors can arbitrage differences in interest rates between currencies, borrowing in one (Yen) at low rates to lend or buy bonds in another (USD). Since Japan’s 10yr yield is capped at 1%, and the US 10 year yield is currently at 4.5%, there is immense profit potential to be had by arbitraging the rate spread.

Here’s a chart of the 10yr spread between US Treasuries and JGBs. It’s at record highs not seen since the intervention crisis of last year.

Bond Market

The US bond market has been getting clobbered this month, with record lows in multiple instruments. The selloff is continuing as the Fed appears to remain steadfast in its commitment to fight inflation, meaning rates will be higher for longer and support for debt instruments remains some ways away.

The 30yr Treasury sold in 2020 at $1.01 on the dollar is now trading at $0.47. The Fed owns 19% of this issuance.

Bloomberg Aggregate Bond Index has also seen yields spike to record highs, as bonds globally have sold off pretty hard. The metric has seen a 14% loss total since the beginning of the year, which may not sound like much but in the levered world of bonds this is a significant loss. Also factor in that the vast majority of passively and actively managed portfolios are run as risk parity.

The 60/40 risk parity portfolio is like the industry standard “Goldilocks” of investments – it puts 60% of your money in fixed income bonds, and the other 40% in riskier assets, like stocks. The purported goal here is to balance out the risk so that volatility is dampened and total returns are upheld. By spreading your money across different types of assets, this strategy aims to give you a decent shot at solid returns without the wild ups and downs you might get with a regular 100% equity portfolio. However, this portfolio assumes an inverse correlation between stocks and bonds- which has only been true for the last 30 years or so. That isn’t the case if you go back to the 1970s or the 1930s.

What happens when that isn’t the case?

It’s not just the extreme long end of the curve that is selling off hard. The 10yr Treasury yield has risen to the highest level in more than a decade, and the 2yr Treasury is at levels not seen since June of 2007, right before the first rumblings of the financial crisis began to hit Wall Street.

A serious question all investors should be asking themselves is why are bonds still selling off if Inflation is Canceled™ and the Fed is done hiking. Apparently not enough people are pondering this question as equities remain within a stone’s throw of the yearly highs.

In Europe, the 10-year German Bund, considered the regional benchmark, saw its yield climb to 2.81 percent, marking its highest level since 2011. Furthermore, some officials have indicated a possibility of further rate increases. On Monday, Chicago Fed President Austan Goolsbee stated that above-target inflation presents a greater economic risk than a restrictive monetary policy.

The Fed may ostensibly want bond prices to fall and interest rates to rise to combat inflation and slow credit growth, but they haven’t considered the paradoxical effect this would have on Treasury issuances. As I have covered before in my piece The Monetary Event Horizon, the United States is entering an exponential debt spiral.

Any interest rate hikes only accelerates this debt spiral, as ⅓ of the debt is being repriced in just the next year. A week ago, the debt passed $33T.

Within 5 business days it was up another $100B.

Furthermore, in the next week the Treasury is set to auction $360B of debt- mostly in the form of short term instruments; bills and notes.

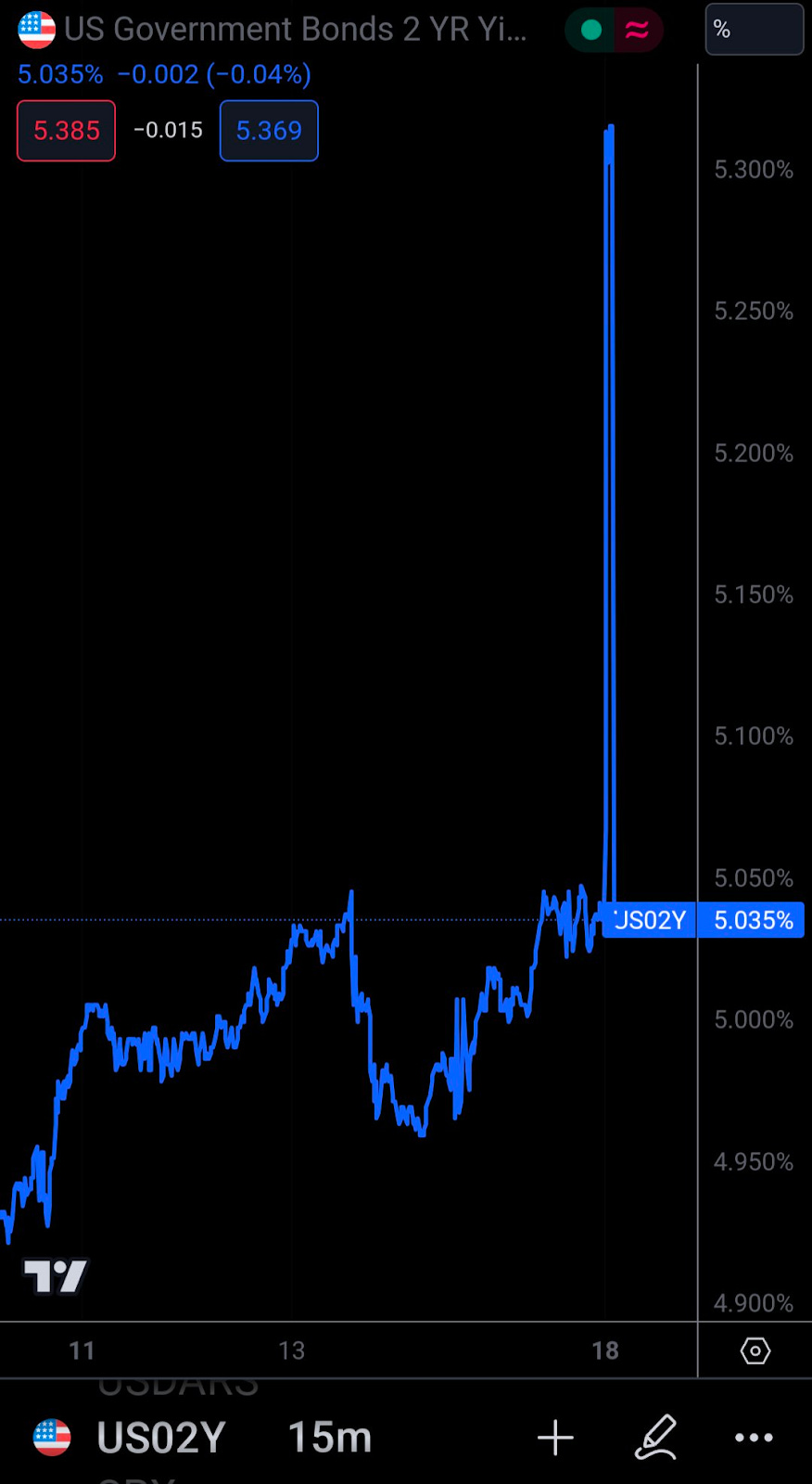

Another thing to note is strange glitches have been occurring with the US 2 Year Treasury yield. On September 18th, the yield ripped up more than 27 bps and then was slammed back down within minutes. Joe Consorti pointed out that this was an issue on TradingView and other bad data providers that didn't know Japan was closed for trading today. Bloomberg Terminal showed nothing.

Then, over a week later on the night of September 26th the yield plummeted within minutes before stabilizing.

Weird.

China

Currently, it appears that the imbalanced Chinese economy is experiencing a significant slowdown due to a substantial property market decline. Addressing the issues in the property sector may require several years, possibly even a decade, to resolve- leading some experts to say that widespread bailouts are needed if deflation is to be avoided. We touched on this issue in depth in a recent piece, but to reiterate, home prices are falling by 20% or more in major cities and housing developers like Evergrande have filed for bankruptcies, with Country Garden (the largest developer) near default on several of their offshore dollar bonds. Foreign investment in the country is down 80% from the same level last year.

Chinese economist Hao Hong noted that 18 trillion yuan ($2.46 trillion) worth of Chinese property were sold two years ago. He said managing 10 trillion this year, or five to six trillion yuan worth of sales further down the road, would be considered “lucky.”. According to UBS, the number of new property construction projects in July plummeted by 65% compared to the second half of 2020. UBS also anticipates that property sales and construction will stabilize at only 50-60% of the peak levels seen in 2020-21. Given that the property sector contributes around a quarter of China's economy, this suggests persistent weakness in demand and the possibility of a future economic scenario similar to Japan's.

With the Yuan weakening to the critical defensive position of 7.3 to the dollar, many citizens are flocking to gold. The majority of the Chinese working-class lack the ability to purchase US dollars or products priced in US dollars as a safeguard against the depreciation of their currency. The surge in interest has propelled spot gold prices in China to their highest levels in 13 years and has caused the gap between the domestic and international gold prices in China to widen to the widest point in a decade. As of Monday, the spot price of gold stood at over 473 yuan (US$64.71) per gram, resulting in a difference of approximately 4.7 percent between the two prices.

Silver is also being drained at record levels from the Shanghai Exchange warehouses as institutions also hoover up the precious metal in preparation for a potential breaking of the currency peg.

In mid-September, the retail cost of gold from prominent brands like Chow Tai Fook, Chow Sang Sang, and China Gold had climbed to 600 yuan per gram, yet consumers remained undeterred from buying. A post discussing the increasing prices of gold jewelry on the Chinese microblogging platform Weibo garnered over 48 million views within just one day of being published.

The public is afraid of further currency turmoil, and are turning to one of their only avenues of protection against such a threat. China has a substantial ($800B) amount of USDs in stock to defend their currency, but this only lasts so long.

Government Shutdown… Again?

We’re here.

Again.

It seems likely that Congress will initiate a government shutdown on October 1, 2023, as it is not anticipated to approve the 12 appropriations bills necessary to fund government operations before the beginning of the new fiscal year. According to the Antideficiency Act, which was originally enacted in 1884 and later amended in 1950, federal agencies are prohibited from expending or committing funds without congressional appropriation or approval. When Congress doesn't pass all 12 annual appropriation bills, federal agencies are required to halt all non-essential operations until Congress takes action. This scenario is commonly referred to as a government shutdown. If Congress passes a subset of the 12 appropriations bills but not all of them, only agencies without appropriations are affected, leading to what's known as a partial shutdown.

On Wednesday, Republican U.S. House Speaker Kevin McCarthy dismissed the Senate's proposal for a temporary funding bill, edging Washington closer to its fourth government shutdown in the past 10 years, with only four days remaining. This would result in the temporary layoff of hundreds of thousands of federal employees and the halt of various government services, including economic data releases and nutrition benefits, until Congress successfully passes a funding bill that President Joe Biden is willing to sign into law.

The standoff has begun to attract the attention of ratings agencies, with both Moody's and Fitch warning it could damage the federal government's credit-worthiness.

Just a few months ago, in June, the government was nearing shutdown as the debt ceiling approached and Treasury Secretary Janet Yellen was forced to undertake extraordinary measures to avoid technical default. This included issuing one day Treasury bills to the tune of $59B and cutting off redemptions from government employee retirement funds- as we covered in depth on this substack. If the government actually shuts down again, this won’t affect the Treasury because the debt limit has been made “unlimited” until January 2025. But this will drastically affect economic growth and GDP as 2 million employees would essentially get furloughed and payments to many government contractors would be halted.

Here’s a snippet of a recent JP Morgan report on what occurs with a government shutdown. I was unable to get the full report as it is only available to private wealth managers and high net worth individuals or institutions subscribed to their research.

As I have laid out before, many seem to forget that government spending is a key additive component in the equation for GDP. If Federal outlays stop, for whatever reason, this by default means GDP falls, all else being equal.

We will have to wait and see what happens. On with the clown show.