Godzilla Returns

The Japanese in a desperate bid to save their falling currency, have now begun hiking rates. USDJPY has begun collapsing, and with it, the carry trade that held up their massive overleveraged economy.

Are the Japanese finally choosing to save the currency at the cost of everything else?

On July 31st, in a surprise move the Bank of Japan hiked interest rates by 25 basis points, or a quarter of one percent. Markets were expecting only a 10bps increase, so this move caught them off guard, along with the hawkish wording of the policy statement from BoJ Governor Ueda.

Following Ueda’s news conference, the Japanese currency appreciated to a range of 150 to 151 yen per dollar. This was a big change from the day before, when USDJPY was trading at 154 yen. In the month of July alone, the government reportedly spent around $36 billion intervening in currency markets to support the yen, as per data released on Wednesday.

These currency interventions have come because the BoJ has sleepwalked into a trap. As I’ve covered in-depth before, all countries (except for global reserve currency holders like the United States) face something called the Impossible Trilemma. Countries can pick two of the three corners; but must give up the third corner as a sacrificial lamb. All 3 corners cannot hold, at least not in the long run.

Most countries need a free flow of capital- this is called in economics an “open capital account”- open bank accounts that allow transfers and settlement of currency across the border, including credit and short term debt instruments that are cash-like in nature, such as Repos. For Japan, this is crucial as they are heavily involved in world trade.

Independent Monetary Policy is still important, but not as crucial as an open capital account for most foreign nation states. This is not to say it has no value, as a home economic crisis can spur a country to shift from the status quo and that can be beneficial to saving their domestic financial system. The question remains, who is the monetary policy “independent” from? The answer, quite clearly, is the Federal Reserve.

Recall that as the dollar is the global reserve currency, it is used in 53% of all international trade invoices, 80% of inter-regional trade settlement, 58% of global forex reserves. The eurodollar system, which are offshore dollars, is in excess of $100T in derivatives, bank balances, loans, and credit instruments. The entire globe is tied to the dollar. Like I laid out in my piece Sword of Damocles:

“The Fed, knowingly or not, is basically in charge of the global financial system. They may shout, “We raise rates in the US to fight inflation, global consequences be damned!!” – But that’s a hell of a lot more difficult to follow when large G7 countries are in the early stages of a full blown currency crisis.

The most serious implication is that the Fed is responsible for supplying dollars to everyone. When they raise rates, they trigger a margin call on the entire world.”

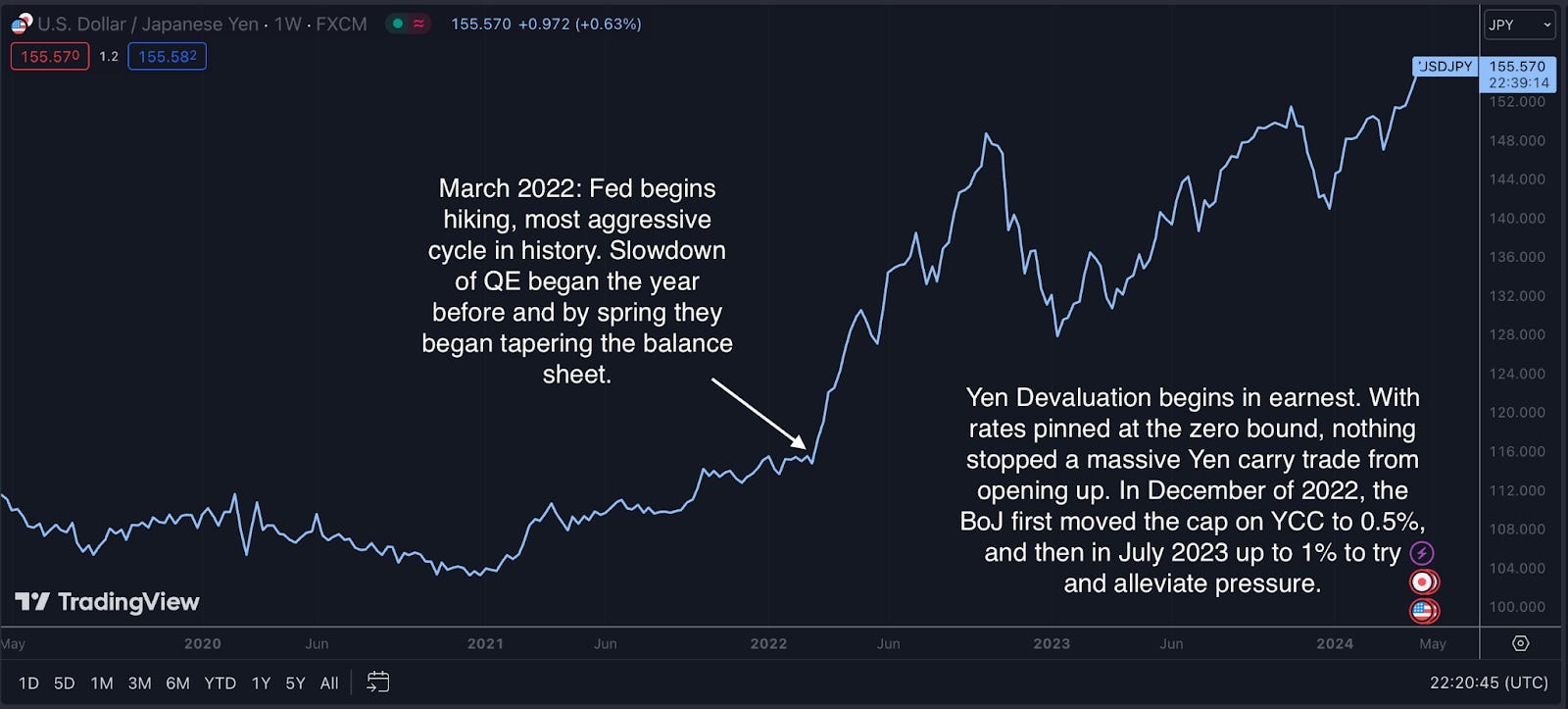

When the Fed began their hiking cycle in March of 2022, we saw massive pressure building on the Japanese financial system, and this resulted in their currency starting to blow out.

This pressure continued throughout the spring and summer of this year. In late April, the BoJ held a disastrous press conference that saw USDJPY move up by 3 yen just during the course of the discussions. Officials quickly panicked and authorized two Yenterventions, one after the other in quick succession. In total, the Ministry of Finance, working with the central bank, spent 9T Yen, or around $55B USD, in currency interventions between these two moves. Recall that they have around $100B USD in liquid cash and $1T USD in Treasury bonds, both of which could be used theoretically to defend their currency, keeping it around the 150-160 level.

The goal with these interventions was simple: blast the shorts with as much firepower as possible, as randomly as possible, to instill fear and prevent new carry traders from opening positions. Remember that carry trades borrow in one currency and lend or invest in another, capturing the spread between the two and pocketing it. They often lever up this trade to juice returns, so carry is a short vol strategy. Typically, carry traders will hedge one or both sides of their trade so that chances of being margin called are low or non-existent; however the cost of setting up and maintaining swaps to do so eat into the carry profits.

Japan was a large funding mechanism for carry traders first because of their zero-bound interest rates, which make it extremely cheap to borrow in Yen- at one point with certain time deposits rates were even negative, which meant borrowers got paid to take out loans. But the other reason why Japan built up such a massive carry trade- (which Deutsche Bank analysts estimated at a staggering $20T USD equivalent!) is because of the lack of volatility in the monetary policy itself.

The Bank of Japan was adjusting their QE, their YCC bands- but the actual base interest rate, the one charged for reserve loans from the central bank itself, had not changed. This is crucial since just like the Fed Funds rate, the BoJ policy rate is the benchmark upon which all other rates are judged. When it moves, the entire rate complex moves- at least in theory.

As this rate has remained at negative 10 basis points since 2016, there has been essentially zero volatility on one entire leg, the funding leg, of the carry trade. This makes carry much more profitable than it otherwise would be, as traders don’t have to pay to hedge this risk, or have to worry about getting blown up. The stability provided here by the Bank encouraged more and more carry traders to jump in headlong into this trade, which ultimately put the aforementioned pressure on their currency, so much so that it devalued 50% within two years.

The Japanese public is the one paying the price, of course. And the central bankers, who are accountable to no one, continued this insane policy for years.

This pressure continued in July, and on the 11th, the Ministry engaged in yet another Yentervention. Market analysts estimated this one at 5.71T Yen, but the Ministry of Finance confirmed at the end of the month that it was 5.53T Yen, or about $36.8B USD, a bit larger than either one of the first two in late April and early May of this year.

Japanese authorities usually don’t confirm immediately if they’ve intervened in currency markets but often warn they’re ready to step in if there’s too much “speculative trading”. Again, they have a lot of dry powder for this, with $1.23 trillion in foreign reserves as of late June. The weak yen is highly unpopular with the public and might be a key issue in the ruling party’s leadership elections in September.

However, any future intervention will be under new leadership, as Masato Kanda finished his term as Japan's top currency diplomat on Tuesday. Atsushi Mimura, the new vice finance minister for international affairs, mentioned in an interview that intervention is still an option.

Now the geniuses at the helm of Japanese monetary policy have tried a new tactic: raising rates. On Wednesday July 31st, the Bank of Japan raised its benchmark interest rate to 0.25%, continuing to wind down its monetary-stimulus policy that has been in place for most of the past 25 years. The rate was previously between 0% and 0.1%, having just moved from negative just afew months ago. (Credit to Reuters for the image below)

Additionally, the bank announced plans to gradually cut its government bond purchases by half, reducing them to ¥3 trillion a month (around $20 billion) by early 2026- essentially a “taper” of the easing that they have long been undertaking.

Markets had expected no change to rates, so this hike was a shock to all participants. BOJ Governor Kazuo Ueda didn't rule out another rate hike this year and stated that the bank is ready to keep raising borrowing costs to what's considered a “normal level” for the economy. This tough stance pushed the dollar below 151 yen for the first time since March.

Under Ueda's leadership, the BOJ has raised rates by a total of 35 basis points in just four months. Wednesday's hike was the biggest since a 25 basis point increase in February 2007, the last major policy tightening before a long period of extreme monetary stimulus designed to boost sluggish aggregate demand.

The hike had immediate consequences. As we see above, the Yen immediately started appreciating against the dollar, steadily dropping to 146 against the dollar. All the USDJPY carry traders, who are functionally short the Yen on the funding leg, now are getting stopped out as the steamroll begins. All this leverage, which was pushing the Yen into the 160s, is now unwinding in spectacular fashion, much to the chagrin of Ueda and others who desperately wanted to stop the currency crisis in its tracks.

However, the cost to be paid will be steep. Recall that after the last two decades of zero interest rates and yield curve control, Japanese public debt to GDP stands at a whopping 263% and the private debt to GDP north of 120%. If the BoJ actually wants to normalize rates with the Fed, their federal government would be paying 13% of their annual GDP alone in interest expense.

13 PERCENT.

The market reactions have already been severe.

On Friday morning, the benchmark Nikkei Stock Average was down 4.0% at 36,588.75 after dropping as much as 5.3% earlier. In the past five years, the index has seen a daily drop of more than 4.0% only at the start of the Covid-19 pandemic. The Nikkei 225 closed a massive 5.8% lower, marking its biggest daily drop since March 2020.

Earlier this year, the Japanese stock index had finally hit record highs, boosted by stronger corporate earnings due to a weak yen, the return of modest inflation, and improvements in corporate governance. It had retaken the critical 38,000 level that was reached in 1990, before the slow rolling deflationary collapse had crippled the economy.

That is quickly coming undone, as we can see in this 3 month chart using 1H candles. In fact, the entire year’s gains have almost been completely wiped out due to the price action from the last few days.

Fund managers had a knee-jerk flight to “safety” by buying Japanese financials, who could “profit from the weaker yen”. This worked Thursday as the Japan bank ETFs were up 1% as the rest of the market sold off, but this soon reversed. Friday saw a bloody day for virtually every single Japanese financial firm, with the average company losing a whopping 10% in a single day.

Elsewhere in Asia on Friday, markets fell sharply. South Korea’s Kospi dropped 3.7%, Australia’s S&P/ASX 200 fell 2.1%, Hong Kong’s Hang Seng Index fell by 2.1%, and China’s Shanghai Composite was down 0.9%.

This is the deflation they wished for. Remember, it is possible to get a stronger currency, but it comes at a steep cost. The brilliant central planners are going to have to brace for a much worse repeat of the 1990s crisis, since this time debt to GDP is much higher and their demographic situation is even worse.