Last Warning

Tokyo just spent ¥8.5 trillion defending the yen in eight days. The line still breaks.

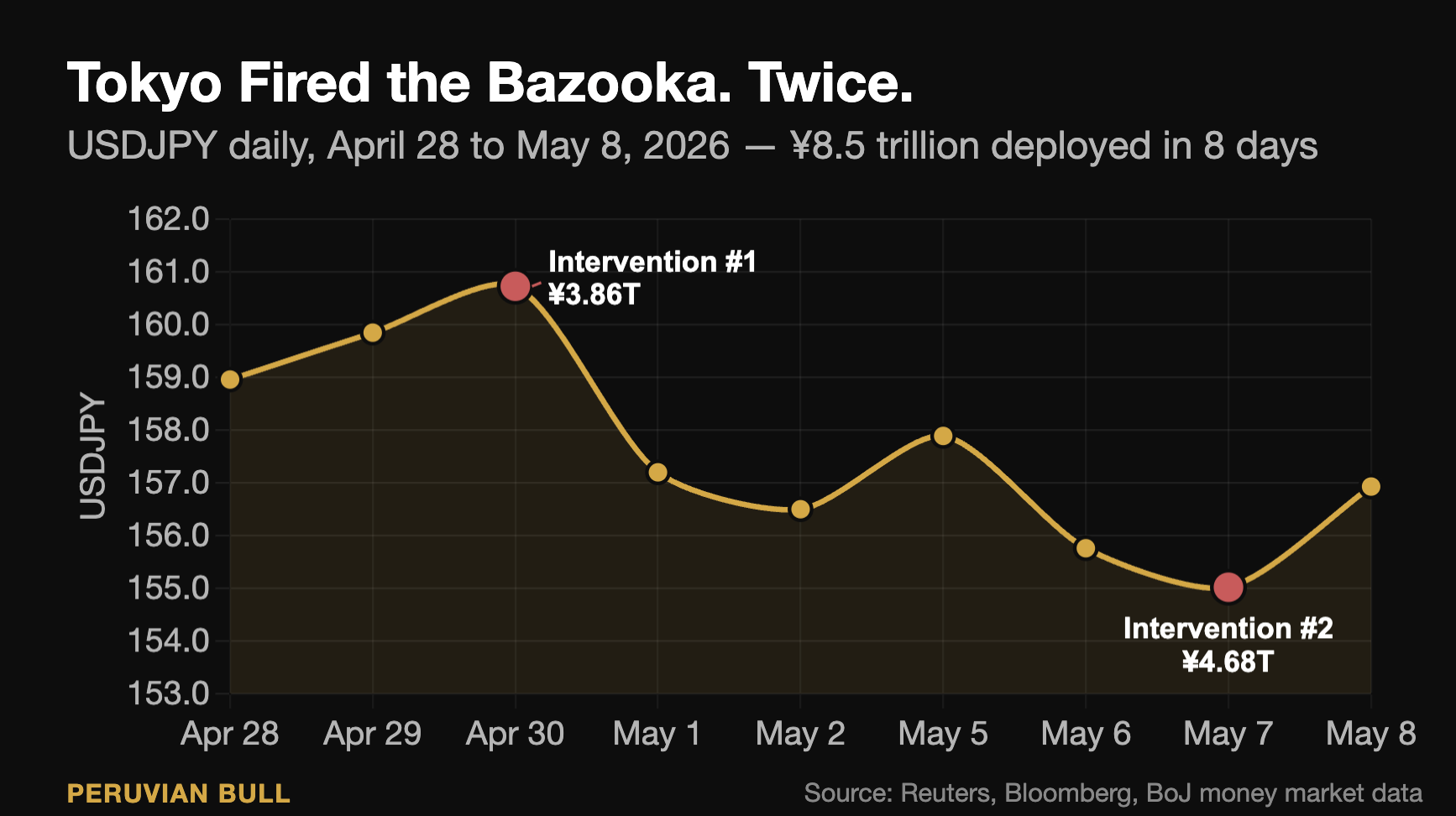

On April 30, 2026, USDJPY printed 160.73, the highest level since the July 2024 intervention.

Japan’s Ministry of Finance, executing through the Bank of Japan, fired the bazooka. Per Bloomberg’s analysis of BoJ current account data, authorities deployed roughly ¥3.86 trillion ($24.7 billion) on dollar-selling, yen-buying intervention. The yen surged 3% on the day, its biggest gain in almost two years.

By May 7th, after a second operation worth approximately ¥4.68 trillion ($30 billion) per Bloomberg’s read of BoJ accounts, total deployed in eight days reached roughly ¥8.5 trillion, around $55 billion. BofA’s Shusuke Yamada estimates the full series may ultimately reach ¥11 trillion (~$72 billion) before it’s done, potentially making it the largest intervention episode since 2022.

The yen briefly traded as strong as 155.02 per dollar.

It’s already back to 157, grinding higher again as I write this.

This is what their ammunition produces in the current environment: a 5-yen rally that is already 80% faded inside a week. The April-May 2024 intervention episode spent ¥9.79 trillion across two operations (a record ¥5.92T single-day on April 29 and ¥3.87T on May 1) and held the line for several weeks before yen weakness resumed. The July 2024 follow-up spent ¥5.53 trillion and held for the better part of a year. The April-May 2026 episode is on pace to match or exceed 2024 in total yen deployed, but the half-life of the price action is measured in sessions, not months.

Japan can theoretically do this another 30 to 40 times before exhausting reserves. But per IMF freely-floating exchange rate classifications, Japan can only conduct two more interventions by November without triggering scrutiny that could result in formal reclassification of the yen as a managed currency. That matters. The yen’s status as one of the world’s three major currencies depends on it being freely floating. If Tokyo crosses the IMF threshold trying to defend 160, they jeopardize the structural reason anyone holds yen at all.

For readers who have followed this substack through Tokyo Drifting, Panic in Tokyo, The Japanese Maginot Line, Burning Yen and Sanamania, the structural setup needs no re-introduction. What is new is that intervention is now demonstrably failing in real time, the energy backdrop is the worst it has been since the 1970s, and the bond market is already pricing in the consequences.

I will not sugarcoat it: the 160 line is going to break, and the next time it breaks, Tokyo’s response options collapse to two: a panic BoJ hike that detonates the bond market, or sit back and watch the yen go to 165, then 170. Neither path leaves the global rate complex intact.

Let’s walk through what happened leading up to this event.

On April 23rd, Finance Minister Satsuki Katayama issued “stark and forceful” remarks about disorderly moves. USDJPY dipped briefly, then resumed grinding higher. April 28th, post-BoJ press conference, she stated authorities were ready to respond “around the clock.” USDJPY printed a 5-day high of 158.96 immediately after. April 30th, the verbal warning came at 160.73, and within hours the bazooka actually fired. Bloomberg’s revised estimate, based on BoJ current account data released May 8th, pegs the operation at around ¥3.86 trillion ($24.7 billion), the first real intervention since July 2024. The yen surged 3% intraday, briefly trading down to ~157 from the 160 highs.

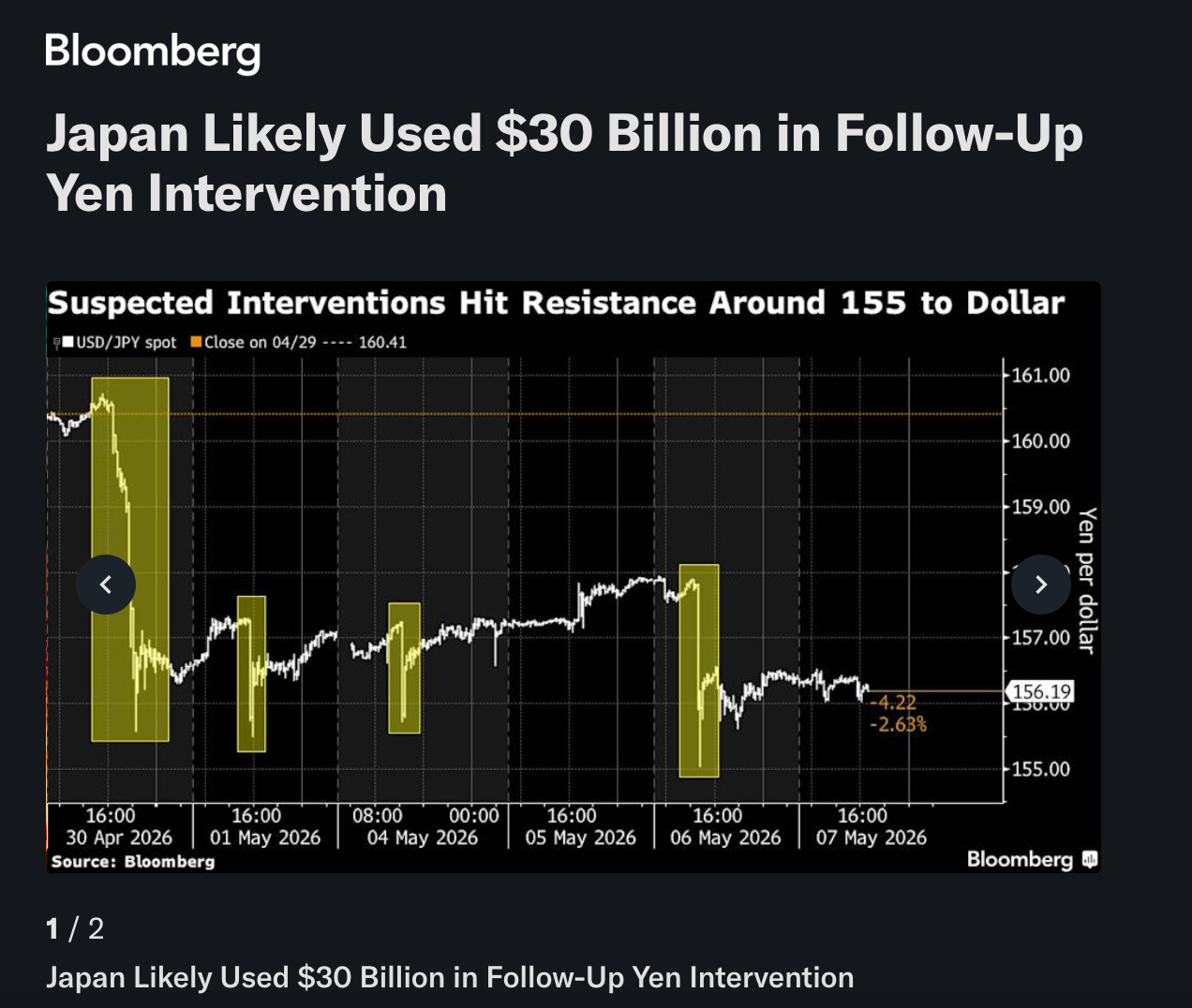

Then May 7th, the first business day after Golden Week. The BoJ’s projection for next-day money market conditions indicated a ¥4.51 trillion net outflow, versus brokerage forecasts of a ¥166.7 billion increase. Yen-buying intervention works by the BoJ soaking up yen from markets, so any outsized shortfall in funds is the cleanest signal you get of an unannounced operation. The implied size: roughly ¥4.68 trillion, around $30 billion. The yen spiked from 157.87 to 155.02, a 1.8% move in a session.

That means there have been two interventions in just eight days, totaling ¥8.54 trillion. And USDJPY is grinding back to 157. (I know I said this before but it bears repeating just how useless these interventions are.)

SPONSOR:

Bitcoin is freedom money, but only if you control your keys.

Partnering with Bitcoin Well, the world’s first publicly traded non-custodial Bitcoin company, ensures this freedom.

They send Bitcoin directly and instantly to your wallet.

No middlemen. No permission needed. Whether you’re stacking sats or making large moves via their OTC desk (Infinite by Bitcoin Well), you remain in control. Self-custody is essential.

Ready to buy Bitcoin the way it was intended? Head to bitcoinwell.com and enable your independence. Use this link https://app.bitcoinwell.com/signup?referral=peruvianbull to sign up and start stacking today!

Now let’s get back to it!

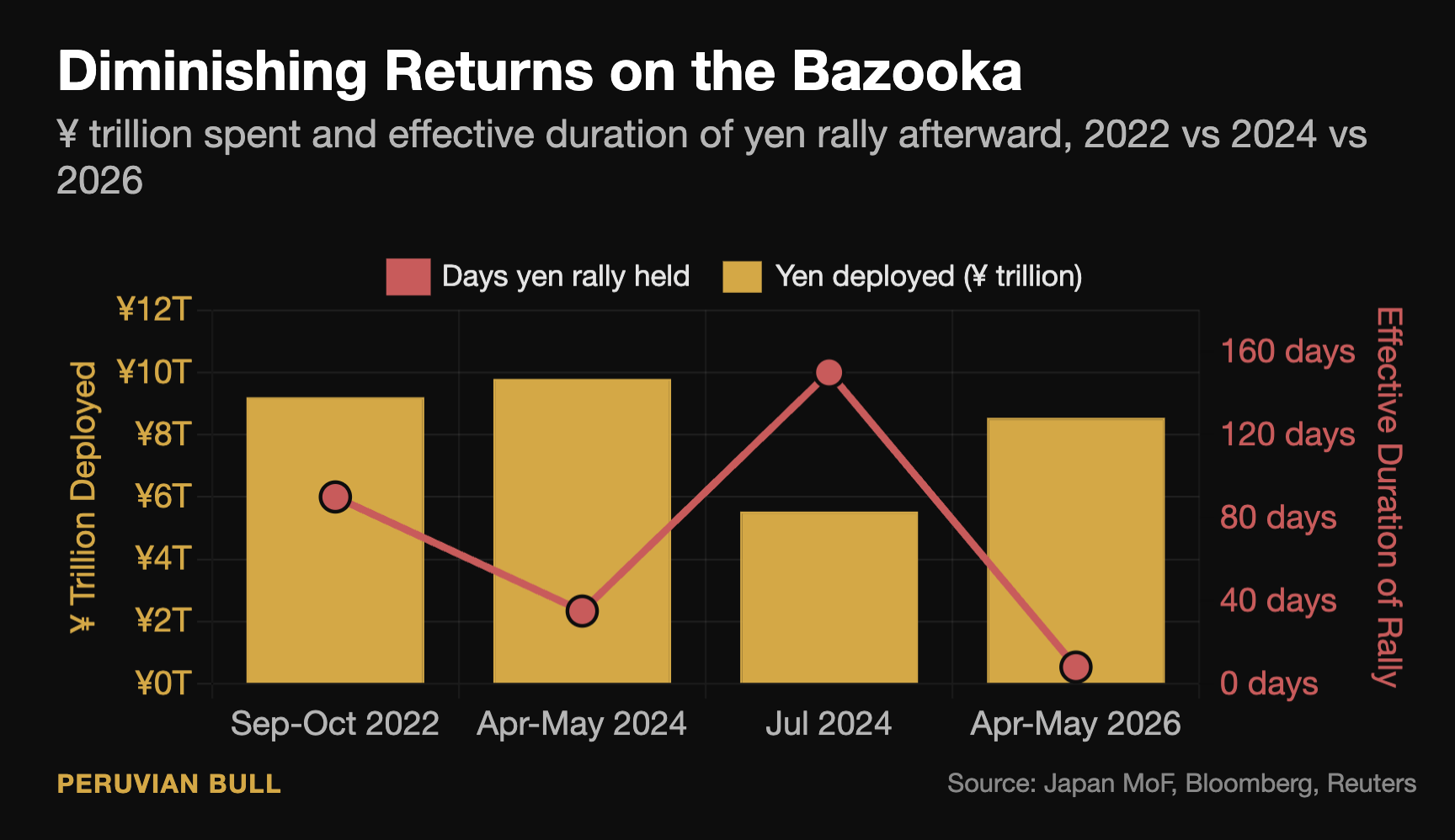

Compare the historical context. The September-October 2022 intervention episode was the first in decades, totaling ¥9.2 trillion across three operations, and it produced a 15% yen rally that held for about three months. The April-May 2024 episode totaled ¥9.79 trillion across two operations, with the single-day record of ¥5.92 trillion on April 29 and another ¥3.87 trillion on May 1, helping drive the yen up by 5% from the 160.245 low. The July 2024 follow-up burned ¥5.53 trillion and bought roughly five months before yen weakness fully resumed.

April-May 2026 is on pace to match the 2024 episode in size: ¥8.54T spent so far against a ~¥9.8T 2024 total, with BofA estimating the full series may reach ¥11T. But the price action lasted eight days. Five days. Whatever it lasts when you’re reading this.

The 2026 episode marks the first FX intervention under the Takaichi-Katayama administration, and it tells you something important about their pain threshold. They moved at exactly 160, which was the same political tripwire used in 2024. But the marginal effectiveness has collapsed. Per Bloomberg’s analysis of the BoJ accounts, applying BofA’s rough rule of thumb of approximately 1 yen of USDJPY movement per ¥1 trillion deployed, ¥8.54T should have produced an 8-9 yen rally. The actual move from peak (160.73) to trough (155.02) was 5.71 yen, and most of it has already been given back.

Here’s the cruel arithmetic: in 2022, ¥9.2 trillion bought a 15% yen rally that held for months. In 2024, ¥9.79 trillion bought a 5% rally that held for several weeks. In 2026, ¥8.54 trillion has bought less than 4% and it’s fading in days. Each episode produces a smaller market reaction with less persistence, even as the absolute yen weakness gets more acute. The speculative position on the other side of the trade is structurally larger, more confident, and faster to fade Tokyo’s interventions.

Why Intervention Doesn’t Work Without Rates

In simple terms, FX intervention sells dollars from Japan’s reserve stack and buys yen in the open market. That puts immediate downward pressure on USDJPY. But it does nothing about the interest rate gap that makes the carry trade profitable in the first place. Intervention is treating the symptom while the disease keeps progressing.

The BoJ policy rate is at 0.75%. The Fed funds rate is at 3.50% to 3.75%. The differential is 275 to 300 basis points. The 10-year Japanese government bond is at 2.38%. The 10-year U.S. Treasury is at 4.29%. On any reasonable hedged basis, the carry differential pays you to short yen and own dollar assets. Intervention does not change this math.

Which is exactly what the market is showing. Within hours of the May 7th intervention, USDJPY started rebuilding. Per CNBC’s analyst quote that captured this perfectly: “Intervention without changing domestic monetary policy is like tapping the brake while keeping your right foot firmly on the accelerator: at best, your passengers have a little fun, at worst, you’re burning through your brake pads.”

The only way to actually defend the yen is to close the rate gap. Either the Fed cuts aggressively (markets price 93-96% odds of a Fed hold on June 17th, so this is not happening) or the BoJ hikes faster than the market expects. The April 28th BoJ meeting saw three dissenters, the largest split since Ueda took office, all wanting an immediate hike to 1.0%. Markets now price 66% odds of a June 17th hike.

But even a hike to 1.0% leaves the differential at 250 bp. Even a hike to 1.5%, which nobody is pricing, leaves it at 200 bp. The math doesn’t get fixed without a Fed pivot, and there is no Fed pivot in the room.

And here is where the energy story breaks the BoJ’s back.

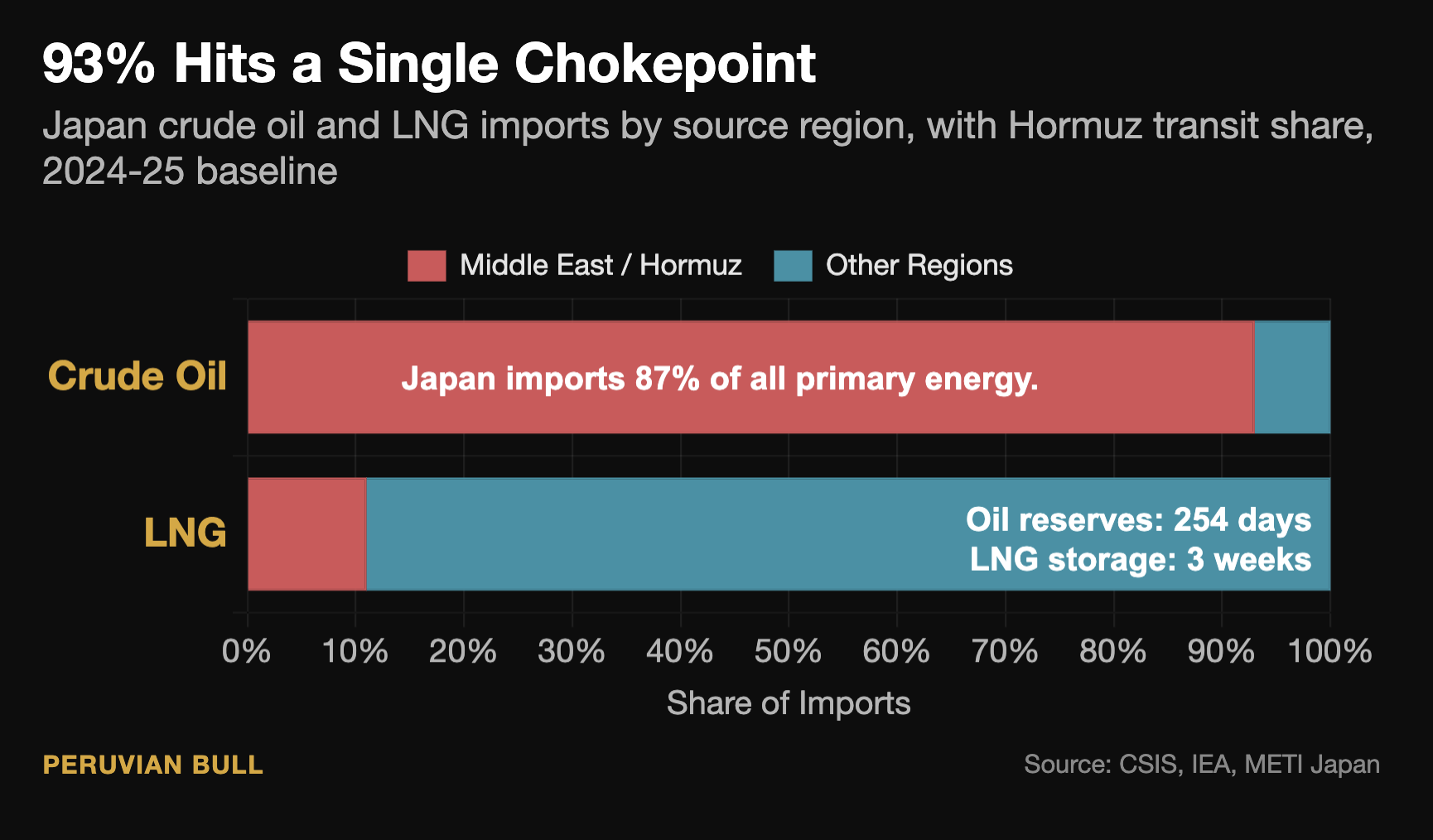

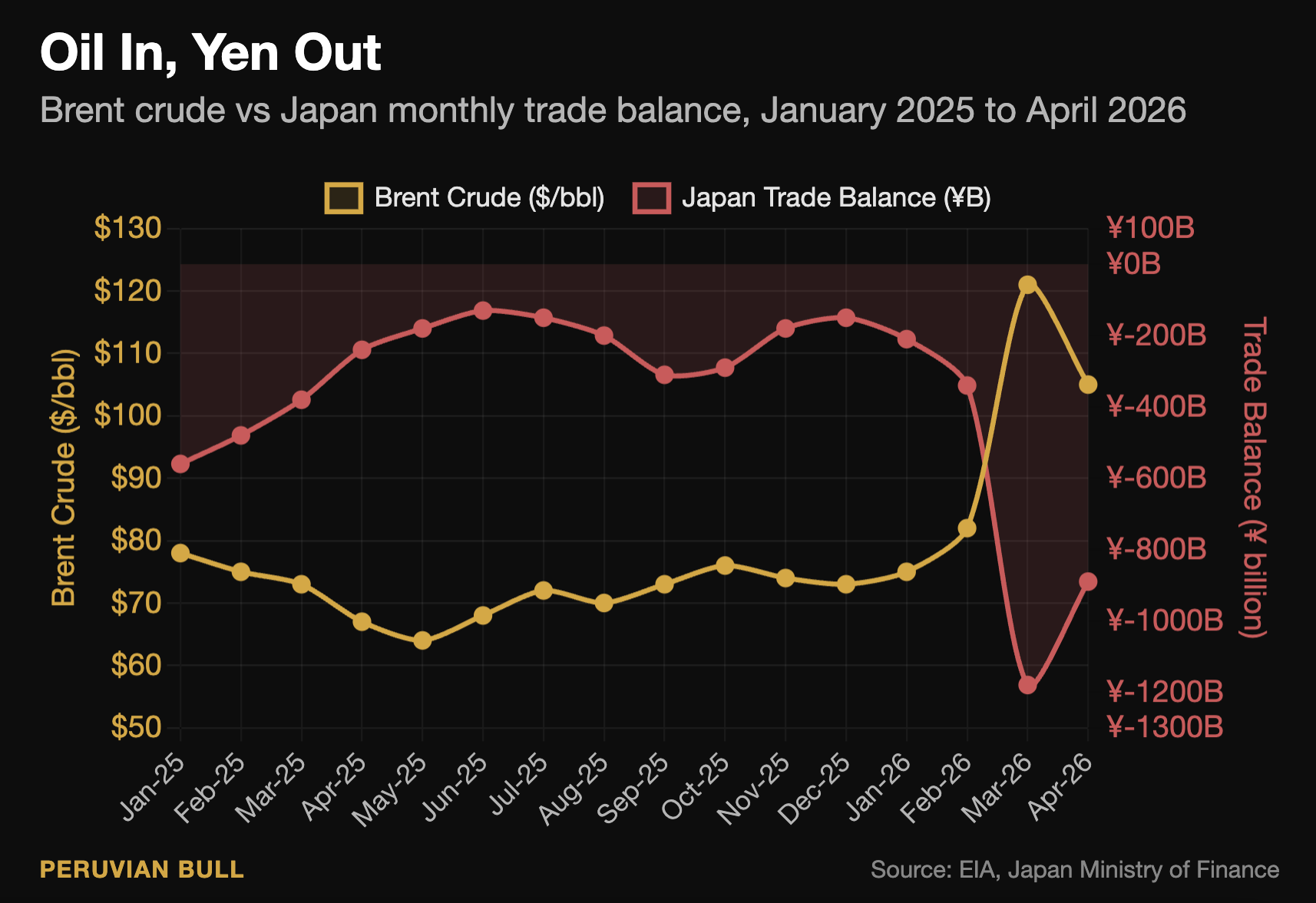

On February 28th, 2026, the United States and Israel attacked Iran. By March 4th, the Strait of Hormuz was effectively closed, shutting off the route through which roughly 20% of global oil and LNG transit. Brent crude surged past $120 per barrel before retreating. QatarEnergy declared force majeure on its LNG export contracts. Even after the April 8th US-Iran ceasefire, shipping volumes through the strait remain far below pre-war levels. Brent today is around $99, settling into a structurally higher range than the pre-war norm.

Japan is the most energy-vulnerable major economy on the planet. The country imports 87% of its primary energy. Roughly 90% of crude oil and 93% of total oil imports come from the Middle East, with the vast majority transiting through Hormuz. About 11% of LNG imports also come through the same chokepoint.

When Hormuz closed, Tokyo started releasing strategic reserves immediately. On March 16th, the Japanese government began releasing 80 million barrels of oil, equivalent to 45 days of domestic demand. Japan holds 254 days of oil stockpile in total: 146 in the national reserve, 101 in mandatory private reserves, 7 in the joint Middle East producer program. That is genuinely impressive infrastructure.

But oil is not the worst problem. The worst problem is LNG.

Japan generates 30 to 40% of its electricity from LNG. Unlike crude oil, which can be stockpiled cheaply in tank farms, LNG is held in cryogenic storage that is expensive to build and maintain. Japan holds about 3 weeks of LNG inventory for power generation.

Past that, the country starts blacking out industrial demand to keep hospitals and homes lit. The government was openly preparing for industrial rationing scenarios in March. With Qatari LNG output stranded behind the Hormuz blockade and Asian LNG spot prices doubling on the conflict shock, Japan has been paying record prices for whatever non-Qatari cargoes it could secure on short notice.

This is the structural reason the yen cannot be defended at 160. Every dollar Brent ticks higher, every yen JPY weakens, raises Japan’s import bill in compounding fashion. Energy goods drive the trade balance, which drives the yen. And the yen weakness drives energy prices in yen terms, which feeds back into the BoJ’s inflation prints, which now forecast 2.8% core CPI for FY2026, up from a 1.9% forecast just three months ago.

(Again, I covered this already in a viral tweet and a prior substack piece, go back and read in depth if you need.)

USDJPY now has a 0.72 rolling 20-day correlation with WTI crude. Read that again. The yen and oil are essentially the same trade now. Long oil is short yen. Short oil is long yen. The macro hedge fund crowd has figured this out and is positioning accordingly.

Prime Minister Takaichi flew to Australia on May 4th and signed a joint declaration on energy security with Anthony Albanese, focused on supply chains for energy and critical minerals. The political class understands the exposure. The problem is that you cannot diversify away from Middle Eastern oil in months. You cannot rebuild LNG storage capacity in months. You cannot restart 15 idled nuclear reactors in months. Structural energy shifts take a decade. Tokyo has weeks.

What you can do in weeks is intervene in currency markets to mask the symptom. Which is why ¥8.5 trillion just moved.

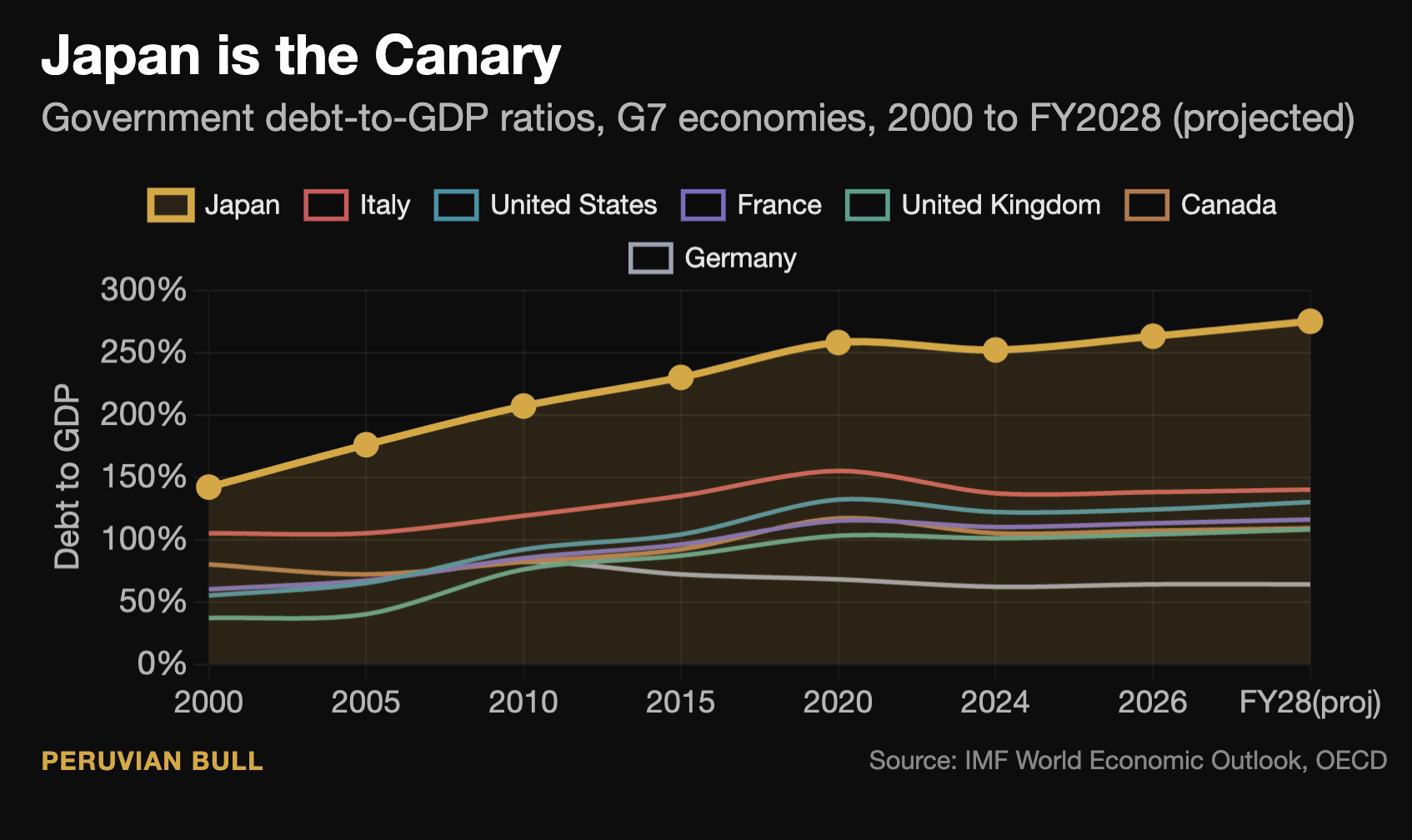

The bond market priced the energy and intervention story months ago. The 10-year JGB hit 2.537% on April 30th, the highest in nearly 30 years. The 30-year reopening cleared at 4.876% in late April. The 40-year, which made global headlines punching through 4% on January 20th and peaking at 4.21%, is currently around 3.89%. These are repricing levels for a country that is now genuinely contemplating what 1,344 trillion yen of debt looks like at 4% rolling yields.

The fiscal arithmetic is brutal. Total accumulated central and local government bonds are projected at 1,344 trillion yen by end of FY2026, nearly twice GDP. The FY2026 initial budget passed cabinet at over ¥120 trillion. The ¥21.3 trillion supplementary stimulus, the catalyst for the January bond market revolt, went through. Each basis point higher in long-term yields translates to roughly ¥134 billion in additional annual debt service on rolling debt.

The most damning number is what the life insurers are sitting on. Per Bloomberg’s analysis from late 2025, Japanese life insurers may be holding ¥27.2 trillion in super-long bonds valued at least 30% below par. Unrealized losses on domestic bond holdings at giants like Dai-ichi and Nippon Life swelled to an estimated $60 billion (¥9 trillion) in early 2026, large enough that the Financial Services Agency accelerated its scheduled balance-sheet review. Sumitomo Life has formally adopted a hold-to-maturity strategy on portions of its JGB book just to avoid recognizing the losses on the income statement.

¥27.2 trillion in super-longs at least 30% below par.

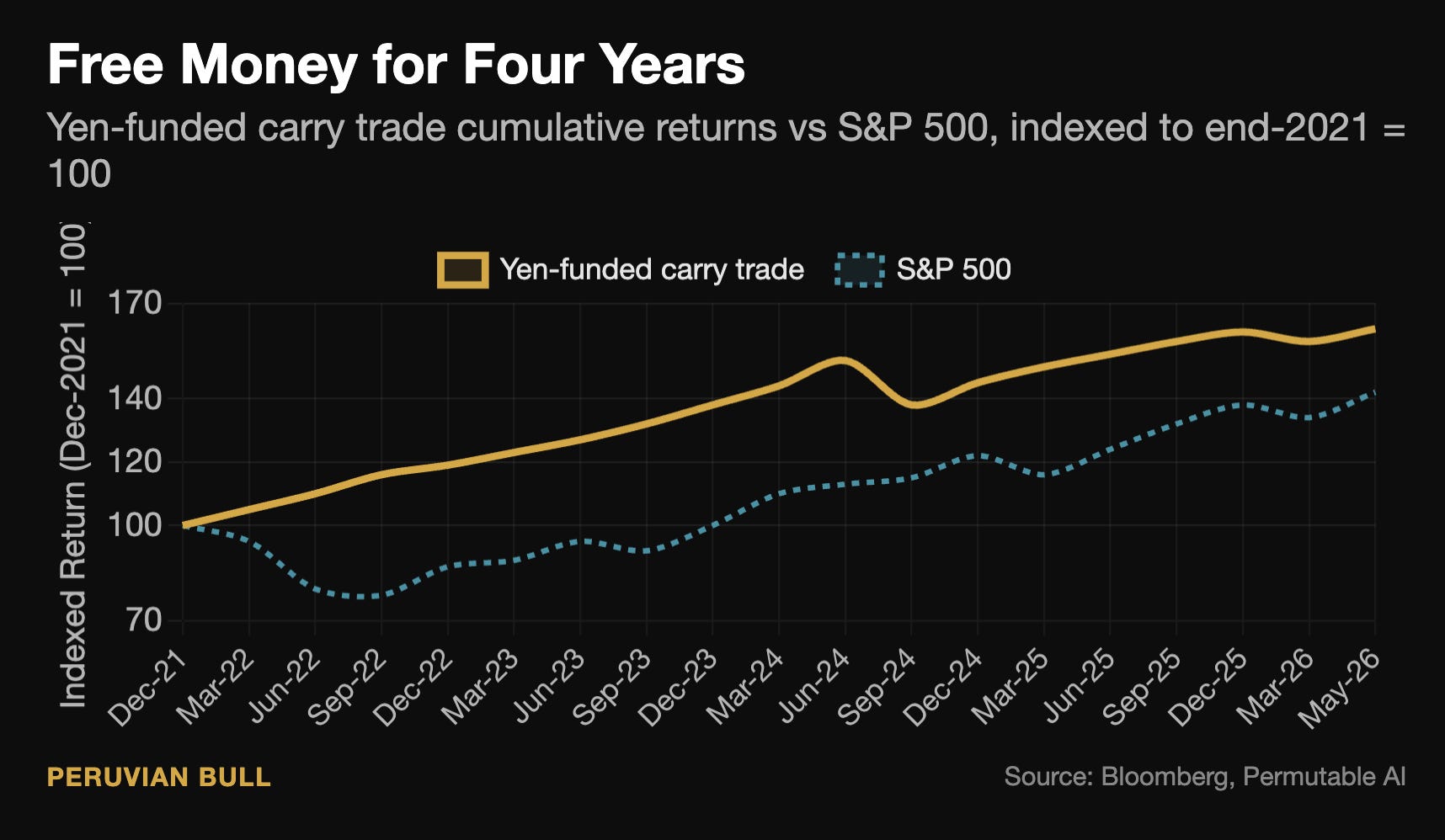

The life insurers were the buyer-of-last-resort for super-long JGBs through the YCC era. They lengthened duration in 2020-2024 in preparation for the J-ICS economic-value solvency regime that took effect in April 2025, and now those legacy positions are crushing them. They have stopped buying. Foreign investors have stepped in and now account for roughly 65% of monthly cash JGB transactions, up from negligible single digits a decade ago. Japan is now being financed at the margin by the same carry traders who are short the yen. When the carry unwinds, those flows reverse.

Japanese foreign reserves stand at $1.16 trillion at end of March, and Japan remains the largest foreign holder of U.S. Treasuries at $1.2 trillion per recent TIC data. The intervention war chest has been drawn down by roughly $67 billion in the past eight days. Capital outflows from Japanese retail and institutional investors have been described by Jesper Koll and other Tokyo-based analysts as relentless, driven by domestic fixed-income returns that remain unattractive on a real-rate basis even after the BoJ’s hike to 0.75%.

The traders shorting yen to fund USD-denominated trades are also the same flows propping up the long end of the JGB curve through hedged duration buying. When (not if) the carry unwinds, it will simultaneously bid the yen, dump U.S. Treasuries, and dump the JGB long end. Three markets that have been operating somewhat independently will reprice together.

The August 2024 unwind, which produced the largest single-day Nikkei drop in history at 12.4%, was triggered by a BoJ rate hike to 0.25%. That was a 25 basis point move, off a starting USDJPY of roughly 145. Today the BoJ is contemplating moving from 0.75% to 1.0%. Same magnitude, but with a starting point of 157, with a 21-month high of 160 in the books. And $99 oil, with ¥27 trillion of underwater life insurer super-longs.

The trigger conditions are stacked deeper than they were in summer 2024.

And no contradictions last forever.

There is no single catalyst that could cause this all to break. There are several plausible triggers, any one of which could fire, and several of which could fire simultaneously. This is the dangerous shape of the setup: when too many fuses are lit at once, you cannot meaningfully hedge any of them, and you certainly cannot tell which one fires first.

Crude breaks $110 again. The April 8th US-Iran ceasefire is holding only barely; ship traffic through Hormuz is still far below pre-war levels. If Iran resumes attacks on tankers, or if the Houthis hit infrastructure at Bab al-Mandeb (which I covered in The Tollbooth), or if Saudi production gets caught up in Iranian retaliation, $110 prints fast. At $110 oil, Japan’s import bill spirals and USDJPY easily prints 162-165. The correlation math is mechanical.

The BoJ pauses in June. Markets price 66% odds of a hike. If Ueda capitulates to Takaichi’s pressure (which Bloomberg Economics explicitly flagged as a risk factor), USDJPY rips through 162 within an hour of the announcement. Conversely, if Ueda hikes by 50bp instead of 25 to “get ahead” of the curve, the carry unwinds violently in the other direction.

A messy ultra-long auction. The next 30-year and 40-year JGB auctions are the real tells. A bid-to-cover under 2.0 on the 40-year, or a tail of more than 2 basis points, is a screaming sell signal. With foreign investors providing 65% of cash JGB liquidity, even a modest pullback at auction has no domestic backstop. Life insurers are at capacity. Banks are at capacity. The BoJ is in QT.

Warsh-driven dollar move. Warsh takes over the Fed on May 15th. If his first communication signals continued balance sheet runoff, the dollar strengthens against everything. The yen breaks regardless of what Tokyo does. This is the cleanest tail risk because it is entirely outside Japan’s control.

Hormuz reopens but LNG doesn’t. Even if oil flow normalizes, the Qatari LNG infrastructure damage has lasting effects. Restarting gas liquefication takes weeks to months. If Japan’s three weeks of LNG storage starts to run thin into a hot summer with industrial demand peaking, you get electricity rationing, manufacturing disruptions, and a panic bid for spot LNG that drives yen weakness through a different channel than crude.

If Japan loses control of the yen, defined as USDJPY breaking and holding above 165 or the BoJ being forced into a panic emergency hike, the consequences spiral globally within days, not weeks.

Yen-funded carry trades unwind. U.S. tech, EM equities, and high-beta credit all reprice simultaneously. Japanese institutions repatriate Treasuries to plug holes in their domestic books, putting upward pressure on U.S. 10-year yields just as Warsh is trying to chair his first FOMC meeting. The Fed gets caught between a funds rate that’s too high for growth and a long end that’s too high for fiscal capacity. The cleanest policy response involves some flavor of balance sheet expansion, which Warsh is on record opposing. The contradiction at the heart of the new Fed regime breaks open at exactly the moment Tokyo is in crisis.

Japan was always the canary. They ran the same playbook the U.S. is on, just twenty-five years earlier: zero rates, QE, YCC, fiscal expansion, monetization. They went first into deflation; they’re going first into the unwind. What happens to Japan in 2026 is the U.S. preview for the early 2030s.

The Treasury has to borrow over $2 trillion this year. Japan was the marginal buyer for years. Japan is now spending its reserves to defend its own currency and starting to draw down Treasury holdings to do it.

The doom loop has a new participant, and it’s the country that used to bankroll everyone else’s deficit.

Follow me on Substack and Twitter for ongoing coverage of the JGB market, the carry trade, and the broader monetary endgame.