Major Signals are flashing Code Red in the Shadow Banking System

Reverse Repo at $2T is Just the Tip of the Iceberg

As I am sure everyone saw, the Fed’s O/N Reverse Repo figure is at a record $2 Trillion, shattering all previous records. The amount and diversity of participants is evidence that this is a systemic issue for Money Market Funds/Banks/Broker-Dealers- not just a few large SHFs needing Treasury collateral. The real issue is worse. Much worse. There are signs that the entire banking system is straining under the weight of the massive liquidity injections from the Fed.

Let’s take a trip-

RRPs

Reverse Repos are extremely similar to short term cash loans. The Financial Institution (most often a Money Market Fund (read here if you don't know what MMFs are) takes $1M of cash, and gives it as a loan to a counterparty, who coughs up $1M of Treasuries as collateral to the MMF. Then the MMF gives the Treasury back to the counterparty at the maturity date of the RRP contract (in this case, the maturity is only one day) in exchange for the payback in full of the original loan. (These have been covered at length in other DDs, read this if you’re still confused)

(Money Market Funds are massive- they manage nearly $5 Trillion dollars as of the end of 2020)

The end result from a RRP is that the MMF is able to use its cash in order to secure Treasuries, and the counterparty gets a loan they can use to cover a short term obligation. The terms Repo and Reverse Repo are interchangeable, they just mean opposite sides of the Repo trade.

(Another way of thinking of it is the entity borrowing the cash (loan) and giving collateral can be called a “Repo Party”, the entity lending cash and receiving collateral can be called the “Reverse Repo Party”. Sorry if these terms are confusing)

Credit to u/leisure_rules for this great explanation:

As many have pointed out, this massive figure is concerning because it is a symptom of a serious issue in the market. MMFs typically operate by taking cash and lending into the “money markets”, aka short term (cash-like) loans, such as AAA+ corporate debt, T-bills, or overnight bank loans. Some MMFs are “government MMFs”, meaning they have to put the majority of their funds into government securities with short durations (SPAXX for example, as pointed out by u/Criand)

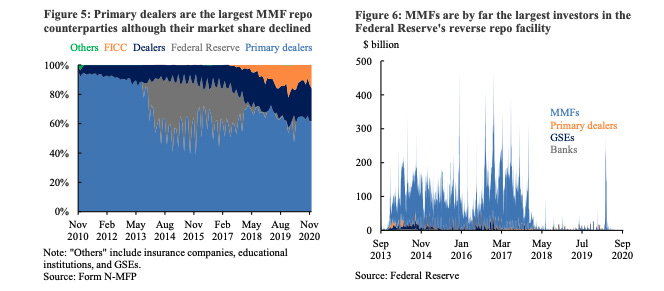

The MMFs are the largest investors at the RRP Facility- accounting for more than 80% of total volume. Since the govt MMFs have to invest the vast majority (99.5%) of their funds into T-bills (another name for short duration treasuries), they are scrambling to park as much money as possible into the RRP facility to maintain their legally required ratio of T-bills to cash.

Typically, these MMFs trade Repos with primary dealers (basically these are banks that are allowed to directly buy Treasuries from the Federal Government- primary dealers are also explained in Part 3.5 of my Dollar Endgame Series) as these researchers explain-

“MMFs conduct the great majority of their repo investments with securities dealers, and primary dealers in particular. Nondealer counterparties include insurance companies, educational institutions, government-sponsored enterprises (GSEs), and the Federal Reserve. Some MMF repos are centrally cleared and novated to the Fixed Income Clearing Corporation (FICC).”

“Access to MMFs in the repo market facilitates a range of dealer’s financing and market making strategies, indirectly connecting MMFs to a broader set of activity in the financial system. As of December 31, 2020, MMFs held $877 billion of repo investments, or 82% of the total, with securities dealers. Of that amount, $642 billion repo investments were with primary dealers. Historically, primary dealers have been by far the largest MMF repo counterparties.” (Source- SEC Money Market and Repo Research Paper- also where I get these charts).

As stated above, MMFs are Repo counterparties for dealers/banks/corporations. Thus, the MMFs are lending cash to the dealers, and receiving T-bills as collateral (occasionally other types of collateral). Remember, a Repo from the counterparty’s (MMFs) point of view is basically a Reverse Repo since they take the opposite side of the Repo trade. MMFs always want to LEND cash in order to get T-bills and debt securities, or just buy them outright.

All these transactions occur in the “Money Markets”- the opaque, hidden and secretive world of plumbing that runs throughout the entire financial system. Reporting here is very spotty- large parts of the markets are lightly regulated, and very few people actually know what is going on in them. This is concerning since large parts of the financial system rely on these markets- for example large corporations such as General Electric, PG&E, and even McDonalds use this markets to roll their short term debt, ensuring that they can borrow enough cash to pay bills each month.

Because this world is so unknown and opaque to most in the financial world, this market has been coined the “shadow banking system”. This is because entities in the system, such as MMFs, ACT as banks (ie depositors put money in, MMFs loan cash to corps/banks for collateral (Reverse Repos). Some retail clients of MMFs can even write checks from their MMF account, just like a checking account!) but they are NOT REGULATED like banks- thus, MMFs (along with other institutions) are called “shadow banks”.

They fall under much lighter regulation standards as “collateralized debt funds”. Post-2008, there was an effort to more tightly regulate these funds as banks/bank substitutes, but the bill failed (See: The Payoff- Why Wall St Always Wins).

In the midst of the 2008 Financial Crisis, Zoltan Pozsar, a Senior Analyst who was hired to work at the New York Fed, started diving deep into the Shadow Banking System. Obsessed with understanding it, he worked day and night for weeks, building a map of how it works, which NO ONE had ever done before. Here it is pictured below, from his seminal paper “The Rise and Fall of the Shadow Banking System”

As you can see, this system is INCREDIBLY complex. The map pictured above is just the executive summary map. The real map is very big (4ft by 3ft or so). I saw the real map in an online research paper years ago, but now it appears that the link to it is broken on the NY Fed’s website (same issue with a FT article). Weird.

If anyone finds it, please let me know. (Extra Credit Reading- Shadow Banking: The Money View by Pozsar)

This system is huge- trillions pass through it every day, and it directly touches most major banks, insurance corporations, broker-dealers, MMFs, and even some pension/hedge funds. Pozsar is one of a few experts who have a deep understanding of how this system works.

Beginning in May 2021, usage of the Fed's RRP facility began to rise. First it hit $400B, then $800B, before soaring above $1T in August 2021. MMFs were scrambling to get their hands on quality collateral. This rush was so strong it dwarfed RRP usage during March 2020.

The problem would not be alleviated with time. A year later, RRP usage would rip above $2T and has been holding steady around $2.2T since then. Part of the reason could be attributed to collateral shortages within the system, but it can also be due to the rising award (interest) rate granted to those who use the RRP facility to park their cash. The rate has been rising and currently sits at 4.80%.

The RRP award rate effectively helps to set a floor to interest rates as financial institutions can lend to the Fed (with basically no counterparty risk) and receive a risk-free return. Thus, when lending to other banks/FIs, they can charge the award rate plus a premium. Think about it from an MMF's perspective: why load up on Treasuries, which opens you up to interest rate risk, when you can just continually loan and re-loan cash to the Fed and get T-bills as collateral, satisfying your regulatory obligation? Plus, you get an award rate.

This scramble was conducted by MMFs in order to get their hands on quality "Tier 1" collateral- Treasuries, Agency MBS, and notes constitute the vast majority of repo collateral.

If this all sounds confusing and murky, it's because it kind of is. I worked with a former Senior Repo trader to create this very basic map of the Fed's Repo Facilities:

All these transactions occur in the “Money Markets”- the hidden and secretive world of plumbing that runs throughout the entire financial system. Since this world is so opaque to most in finance, it has been coined the “shadow banking system”. This is because entities in the system, such as MMFs, ACT as banks but they are NOT REGULATED like banks- thus, MMFs (along with other institutions) are called “shadow banks”.

For example, depositors put money in, and MMFs loan cash to the Fed/banks for collateral (Reverse Repos). Some retail clients of MMFs can even write checks from their MMF account, just like a traditional checking account!

In the midst of the 2008 Financial Crisis, Zoltan Pozsar, an Analyst at the New York Fed, started diving into the Shadow Banking System. Obsessed, he worked day and night for weeks, building a map of how it works, which NO ONE had ever done before. Here it is pictured below:

As you can see, this system is INCREDIBLY complex. The map pictured above is just the executive summary map. The real map is very big (4ft by 3ft or so). You can read his seminal paper here: https://economy.com/sbs

This system is huge- trillions pass through it every day, and it directly touches most major banks, broker-dealers, MMFs, and even some hedge funds. Pozsar is one of a few experts who have a deep understanding of how this system works. Now as Treasury rates have soared in the past few quarters, banks have incurred MASSIVE unrealized losses on their Hold to Maturity (HTM) bond portfolios. At the same time, MMFs, which invest a majority of funds into T-bills, have seen income rates soar as interest rates rise.

The danger here is that MMFs are not insured by the FDIC or NCUA. However, there is an implicit Fed backing on MMFs after the Reserve Primary Fund broke the buck in 2008. The Fed stepped in and extended guarantees to the rest of the MMFs to prevent a systemic run. The deposits draining out of the system can be weathered by the large banks. However, regional banks and credit unions don't have the amounts of credit that the bulge brackets do, and have a risk of deposit flight as the rates they offer are nowhere near competitive with a MMF.

The financial crisis that Yellen claimed would never occur in our lifetime has already begun… and the Fed is claiming to remain committed to tapering. All while the signals are blinking red.

Nothing on this Post constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person.

The shadow banking map from old snapshot at archive.org https://web.archive.org/web/20130810002710/https://www.newyorkfed.org/research/economists/adrian/1306adri_map.pdf

Just in case, there’s some repetition in this post, see

Obsessed with understanding it, he worked day and night for weeks, building a map of how it works,