No Exit

The June 16 rate hike is already priced in. The yen is still at 160. Someone should tell the Bank of Japan.

The market has been waiting months for this.

A Bank of Japan rate hike, the one that finally closes the carry trade, strengthens the yen, and puts this whole ugly saga to bed.

Governor Ueda delivered the pre-announcement two weeks ago, on Wednesday June 3rd at the Kisaragi-kai meeting in Tokyo. He pivoted so hard toward inflation-fighting rhetoric that Reuters called it a “new phase” in his five-year term.

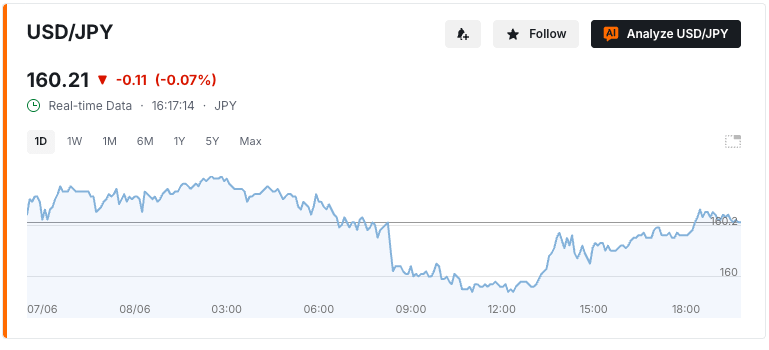

Markets immediately priced an 80% probability of a move at the June 15-16 meeting. The yen ticked up briefly to 159.40 on the news.

By Friday, it was back above 160.

There’s a word for what Tokyo is experiencing right now- a Chinese finger trap.

This is the kind that tightens the more you struggle. And boy, have the Japanese been struggling.

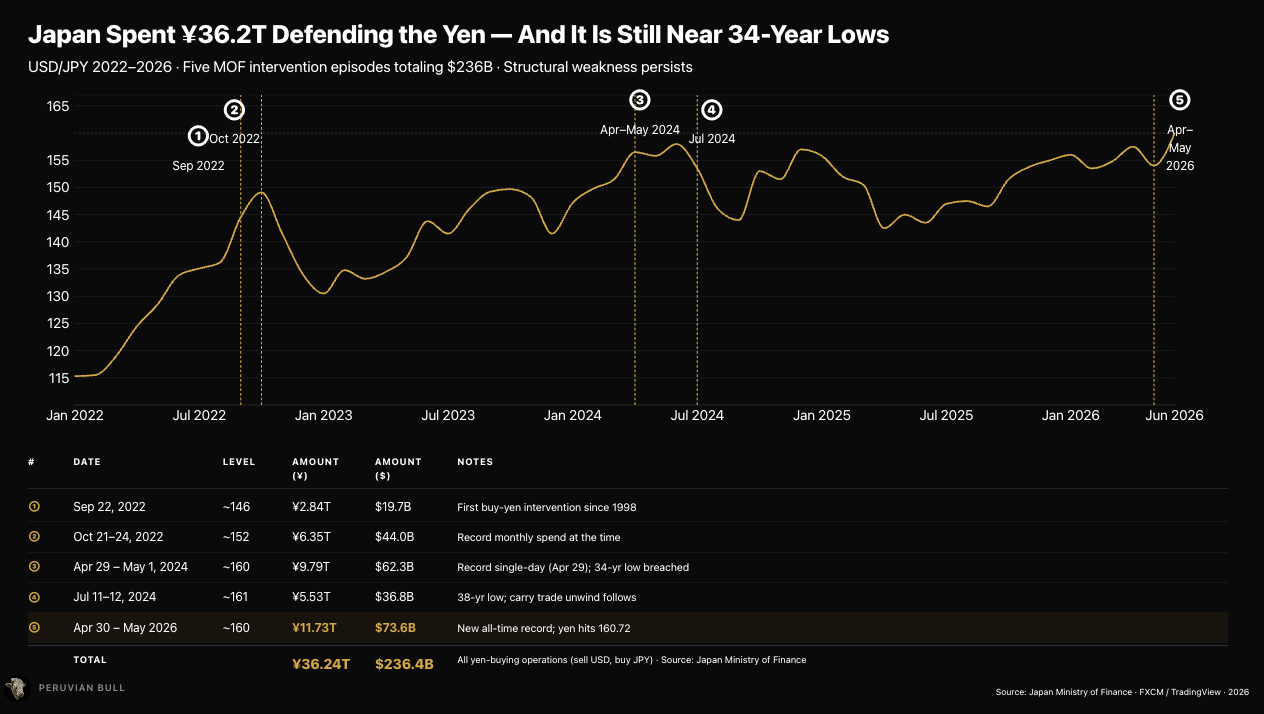

Japan spent ¥11.73 trillion ($73.6 billion) in currency interventions between April 28 and May 27, a record in the modern era, and the yen underperformed every single one of its G10 peers in May. The BOJ is now five days away from hiking rates for the first time to 1% in over three decades. And the pair is trading at 160.31 as I write this. The medicine isn’t working.

Every piece of analysis on the yen over the past two years returns to the same root cause: the interest rate differential. Japan at 0.75%, the United States at 3.75% to 4%.

A 300-basis-point spread that makes borrowing yen and parking the proceeds in Treasuries a near-riskless carry. The yen is the world’s funding currency precisely because it costs almost nothing to maintain that position.

The June 16 hike to 1% changes this differential by exactly 25 basis points.

The spread would move from roughly 300bps to 275bps.

[At 275 basis points, the carry trade doesn’t close. It barely notices. Oh and by the way- most carry traders locked in long term debt rates long before the current (tiny) hiking cycle. This doesn’t impact them]

To understand why, you need to understand how carry trades die.

They don’t die because the differential narrows slightly; they die because the differential turns negative, or because something external forces mass position liquidation.

August 2024 is the canonical example: the BOJ hiked from 0.1% to 0.25% in July 2024, a 15-basis-point move, and within six days the Nikkei dropped 12%, the yen surged from 158 to 142, and cross-asset vol spiked across every major market. That wasn’t caused by a closing differential. It was caused by traders caught offside, a one-way bet that suddenly reversed. The CFTC’s Commitments of Traders data currently shows speculative accounts have rebuilt substantial net short yen positions, but analysts note they are not yet at the extreme levels seen before prior interventions. The crowded boat hasn’t capsized yet.

The current move is priced in already. The carry trade community has had six months to see this hike coming. Traders who were going to exit already exited; those still short the yen are short knowing the hike is coming.

That’s why even Ueda’s most hawkish speech in his tenure produced a rally that lasted approximately four hours before fading back to 160.

“Even if the BOJ raises rates in June, any rebound in the yen will be limited,” said Rinto Maruyama at SMBC Nikko Securities. “Intervention is buying time, not turning the tide,” said Masahiko Loo of State Street Investment Management. “The real pivot has to come from the BOJ.” The problem: the real pivot isn’t coming.

Everyone is focused on whether the hike saves the yen.

The better question is what the hike breaks on the other side.

Japan’s outstanding government debt as of fiscal year 2026 sits at approximately ¥1,344 trillion. As I laid out in Panic in Tokyo, Japan’s own Ministry of Finance has published the arithmetic: a one percentage point increase in interest rates adds roughly ¥3.7 trillion to annual debt servicing costs three years out.

That’s per 100 basis points.

Every quarter-point hike adds roughly ¥925 billion in structural fiscal drag that compounds as debt rolls over.

The BOJ is now being forced to choose between two forms of fiscal self-destruction: the slow burn of yen devaluation destroying household purchasing power, or the faster burn of rising rates destroying debt sustainability.

Neither is a good outcome.

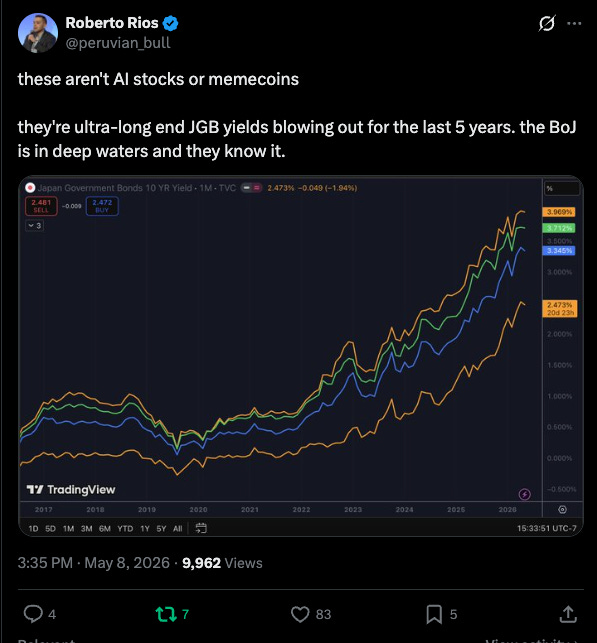

The 10-year JGB yield touched 2.8% in mid-May, the highest since 1996. Sitting at 2.66% as of Friday, it has come off the highs but remains at multi-decade levels. The 30-year hit record yields earlier this year; the 40-year reached an all-time high of 4.23% in January before retreating. These aren’t just abstract financial metrics. They are the rate at which Japan’s government has to refinance its debt as older, cheaper obligations mature. The average coupon on outstanding JGBs remains far below current market rates, meaning every year of refinancing locks in higher interest expenses that never go away.

Ueda is aware of this.

In his June 4 speech, he acknowledged it directly: timely rate hikes, he argued, could “anchor market confidence and prevent destabilising jumps in bond yields.”

The logic being that a small hike now, by showing the BOJ is serious about inflation, prevents a larger loss of confidence later that forces yields even higher. It’s a reasonable thesis. The problem is that the bond market has read the same fiscal projections the BOJ has, and it’s pricing in a trajectory that rate hikes alone won’t fix.

For readers of this Substack, the intervention math from Last Warning is already familiar, so I won’t re-litigate it here beyond what’s essential to the new argument.

The headline: Japan deployed a record ¥11.73 trillion ($73.6 billion) in currency market operations between late April and late May. Bloomberg’s analysis of Bank of Japan current account data broke it into two operations: roughly ¥3.86 trillion on April 30 and approximately ¥4.68 trillion around May 7, with further operations in the weeks following. The yen rallied from 160.73 to as strong as 155, then ground back above 159 within the same month.

What’s new: Japan’s foreign exchange reserves stood at ¥1.37 trillion at the start of 2026, at a four-year high, before the intervention cycle began. The April intervention alone would have consumed roughly 5% of that reserve base. Multiple operations through May push the consumption toward 8-9%. Japan still has a large war chest, but every intervention cycle that fails to hold the line makes the next one more expensive in credibility terms even before you count the actual dollars spent.

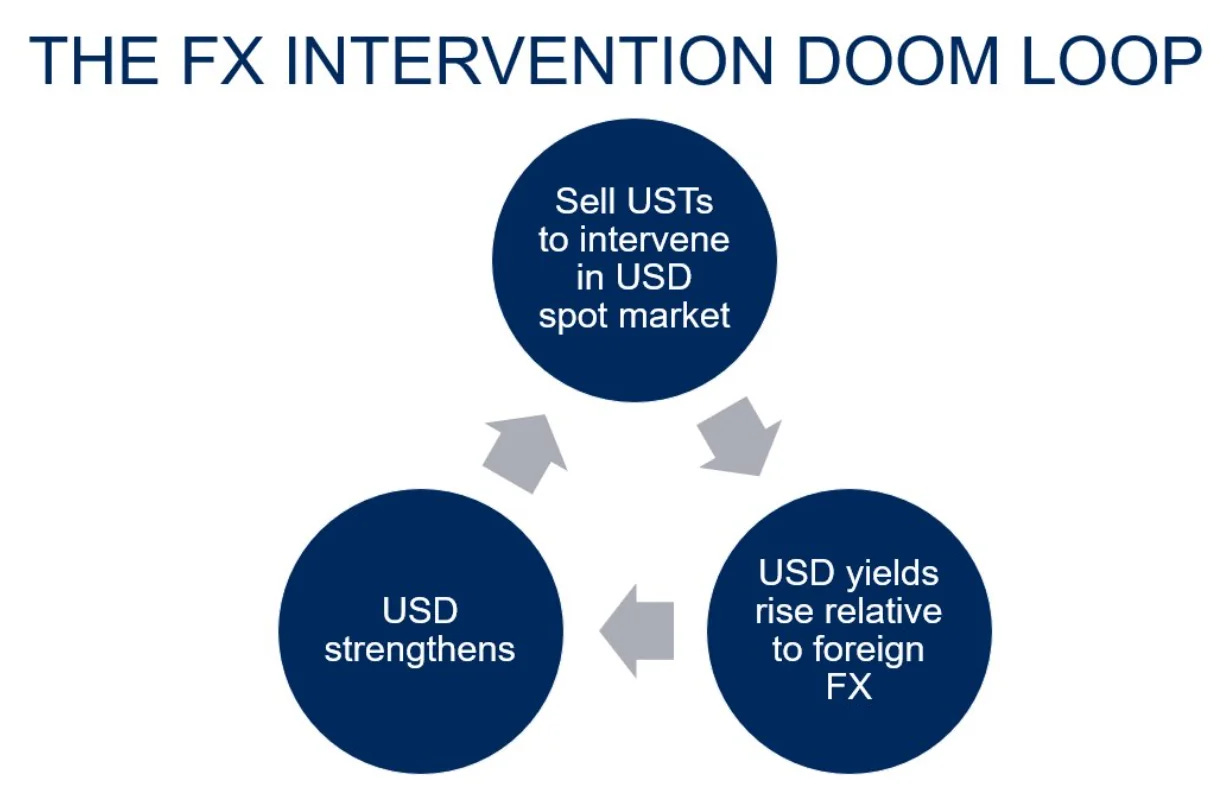

The deeper problem: Japan’s reserves are not as liquid as the headline figure suggests. The majority is invested in U.S. Treasuries and other foreign bonds. Selling those bonds into the market to fund yen-buying operations means the MoF is simultaneously selling Treasuries (putting upward pressure on U.S. yields) and buying yen (providing temporary support to the currency).

The moment Treasury Secretary Bessent or any Fed official objects to what amounts to coordinated currency intervention affecting U.S. bond markets, the political calculus changes. Bessent already signaled as much in May, noting that Ueda would do “what he needs to do” regarding rate policy, which is diplomatic language for “we’d rather see rate hikes than dollar sales.”

Source: Japan Ministry of Finance, Bloomberg BoJ current account data

And to make matters worse, that will exacerbate the yen weakness issue. Due to the FX intervention doom loop, sales of US Treasuries will push up yields which will increase carry trade pressure on Yen shorts.

Ueda’s June 4 speech was the clearest signal he’s ever given.

The language shifted from “gradual normalization” to active warnings about inflation overshooting. He cited the Iran war’s energy shock as pushing oil-driven inflation into second-round effects; meaning it’s no longer just about fuel prices, it’s about wages adjusting upward in response to a higher cost of living, embedding inflation structurally into the economy. That’s the scenario the BOJ has been most afraid of for two years.

To his credit, the logic is internally consistent. Wholesale inflation in Japan hit a three-year high in April, and real wages rose 1.9% in April, the fourth straight month of gains. The data supports a hike. The board split 6-3 in April with three members wanting to hike immediately. By June, 28 of 34 economists surveyed by Reuters are forecasting a move. This is as close to a consensus hike as Japan gets.

But here’s what Ueda can’t say out loud: even if he hikes to 1%, and even if the board signals a path toward 1.5% or 2% over the next 12-18 months, the rate differential with the U.S. remains so wide that the carry trade rebuild is structurally incentivized every time the yen rallies. Japan’s interest rate is the ceiling, not the floor. Without Fed cuts to bring U.S. rates down from 3.75%, or some exogenous shock that forces global risk-off, Tokyo is pushing against a permanent structural headwind.

But while everyone debates the yen, the real tell is in the JGB market.

The bond market is not pricing a gentle normalization path where the BOJ hikes slowly to 1.5% over three years and everything settles. It’s pricing something closer to a credibility crisis.

The 10-year JGB yielding 2.66%, a level not seen since 1996, is pricing a scenario where Japanese inflation remains elevated and the fiscal situation doesn’t improve.

The 40-year yield at nearly 4% is pricing a scenario where long-term holders of Japanese government debt demand substantial compensation for the risk of holding a government that is running FY26 total spending at ¥120 trillion against a debt-to-GDP ratio of 263%.

Here’s the feedback loop that matters.

When JGB yields rise, several things happen simultaneously.

The cost of servicing Japan’s debt increases, worsening the fiscal deficit. Life insurers and pension funds that are sitting on massive unrealized losses from their JGB portfolios face increasing capital pressure, which may force them to sell further.

The BOJ’s own balance sheet, which exceeds 120% of GDP in size, takes mark-to-market losses on its holdings.

And the government faces higher financing costs on every new issuance, which must occur continuously since Japan’s debt is being refinanced on a rolling basis every year.

All roads lead to more QE and more debasement (eventually).

(The insurer angle deserves more attention than it’s getting- but I’ll cover this in a future article)

Another fun fact-every 100 basis points of JGB yield increase creates paper losses on the BOJ’s portfolio equivalent to roughly 1.2% of Japan’s GDP.

The current yield curve has risen 150-200 basis points across most tenors from where it was 18 months ago.

The IMF’s own 2026 Article IV consultation flagged this explicitly: a faster-than-expected rise in yields could lead to the realization of valuation losses on asset holdings and increase liquidity needs, warning that regional banks in particular face “limited shock-absorbing capacity” from securities losses.

The BOJ is trying to thread a needle between “not hawkish enough” (yen keeps weakening, inflation keeps rising) and “too hawkish” (JGB market breaks down, fiscal crisis accelerates).

I will not sugarcoat it, the June 16 hike is probably priced in.

The yen may rally briefly to 157, perhaps 155 if there’s a hawkish forward guidance surprise. Then the structural drivers reassert themselves: the rate differential remains wide, energy import costs remain elevated, fiscal expansion continues, and the JGB market continues to price a debt trajectory that demands either monetization (yen-negative) or eventual restructuring (also yen-negative, in its own way).

The honest answer to “what happens after June 16?” is: the BOJ either continues hiking aggressively toward 2%, or it doesn’t. If it does, JGB yields rise further, debt service costs escalate, and the fiscal doom loop accelerates toward the crisis phase I described in The Japanese Maginot Line three pieces ago. If it doesn’t, the rate differential stays wide enough that the carry trade rebuilds and the yen returns to 160 within weeks of any hike-driven rally.

There is no path from 0.75% to 1.0% that solves the yen problem. There might be a path from 0.75% to 3.0% that does, but Japan’s debt-to-GDP ratio of 263% means 3.0% rates would cost the government something in the range of 15% of GDP in annual interest alone. That’s not a policy option. That’s a sovereign debt crisis.

There is a version of this story where the BOJ keeps hiking, the U.S. economy eventually slows enough to force Fed cuts, and the differential closes from both ends simultaneously, giving the yen a genuine path back to 140 or 130. That scenario requires a soft landing in the U.S., resolution of the Iran conflict, and a Japanese government that voluntarily accepts fiscal tightening while its debt is rolling over at higher rates.

Three simultaneous miracles.

The more likely scenario is the one the bond market is pricing: yield curve stress that forces a reckoning between Japan’s fiscal commitments and the cost of its debt.

When that reckoning arrives, it won’t look like a currency crisis. It will look like a bond market crisis that becomes a currency crisis, which becomes a banking crisis, which becomes something that doesn’t have a clean name yet.

And the Bank of Japan will be ready to respond, with some new monetary policy- like they always do.

The whipsaw from 159.40 back above 160 after Ueda's pivot tells the whole story here. Markets clearly don't believe the BOJ has the stomach to actually follow through, despite the "new phase" rhetoric at Kisaragi-kai.

What's fascinating is how the carry trade has become this self-reinforcing trap where even credible hawkish signals get fade within days because speculators know the BOJ is caught between crushing their own exporters and letting the yen collapse further.

If they do hike and it actually sticks this time, what happens to all those levered positions that have been built on the assumption that Japanese rates stay pinned at close to zero indefinitely?

https://www.imdb.com/title/tt0174708/