Panic in Tokyo

The world’s most stable bond market is breaking down, and almost no one is paying attention.

For three decades, Japan’s government bond market served as the bedrock of global finance: predictable, low yielding, and utterly boring.

Generations of traders built careers on the assumption that JGBs simply did not move. The Bank of Japan had crushed volatility so thoroughly that the 10 year yield hovered near zero for years at a time, making the entire asset class functionally irrelevant to anyone seeking returns.

That era is now over.

In the span of twelve months, Japanese government bonds have transformed from a sleepy backwater into the most consequential fixed income market on Earth. Yields have surged across the entire curve, prices have collapsed, and a generation of institutional investors find themselves staring at tens of trillions of yen in unrealized losses. The BoJ’s retreat from decade long intervention has exposed a market utterly unprepared to price risk, and the implications extend far beyond Tokyo.

This is not a technical adjustment. This is a structural break in one of the foundational pillars of global finance.

I’ve been warning about this for years, but it appears the move has accelerated quickly in recent weeks.

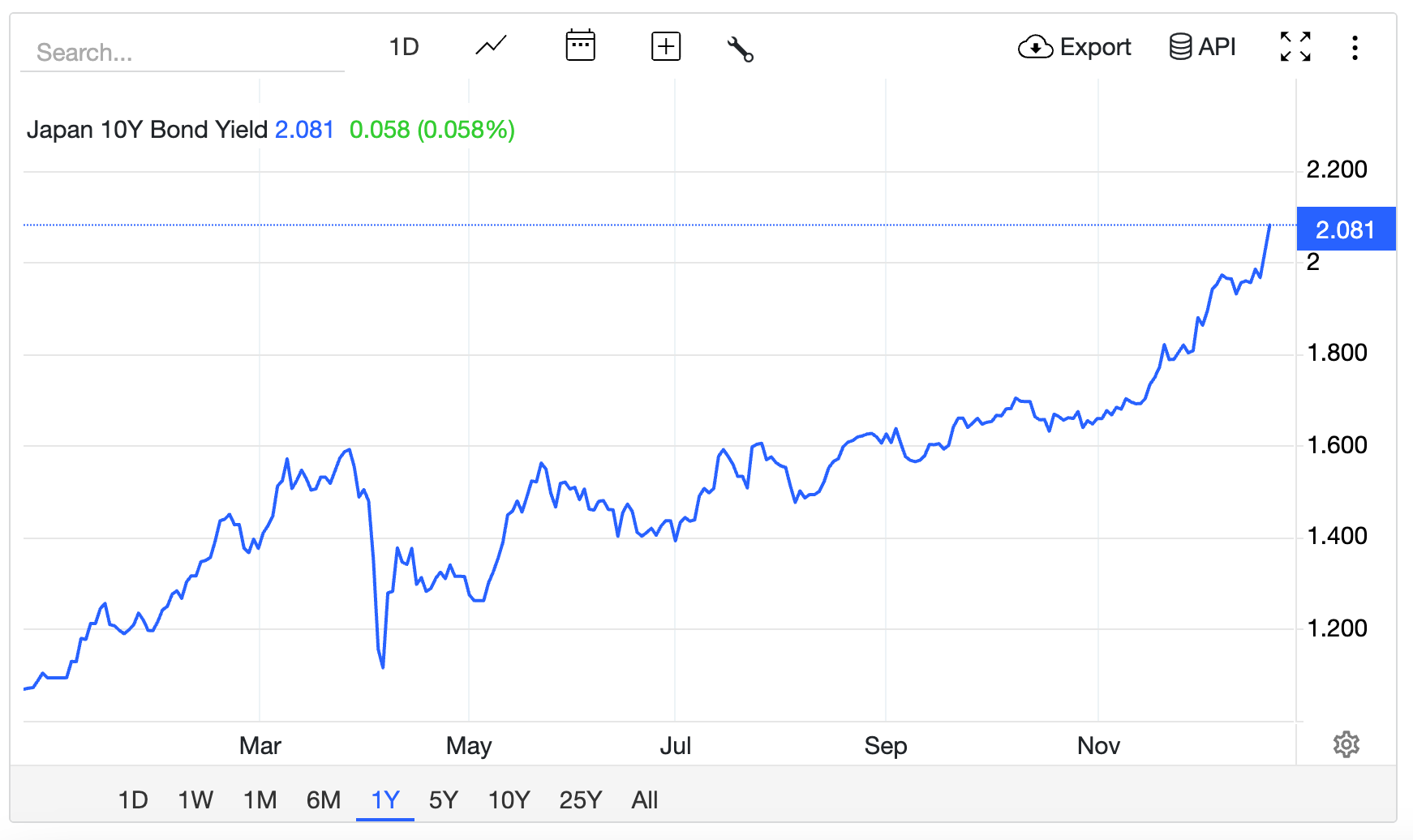

This week, Japan’s 10 year government bond yield crossed above 2% for the first time in twenty six years following the Bank of Japan’s December rate decision, reaching levels not seen since 1999. The benchmark 10 year yield has gained more than 90 basis points over the past twelve months, a staggering move for an instrument that barely budged for most of the previous decade.

Source: Trading Economics

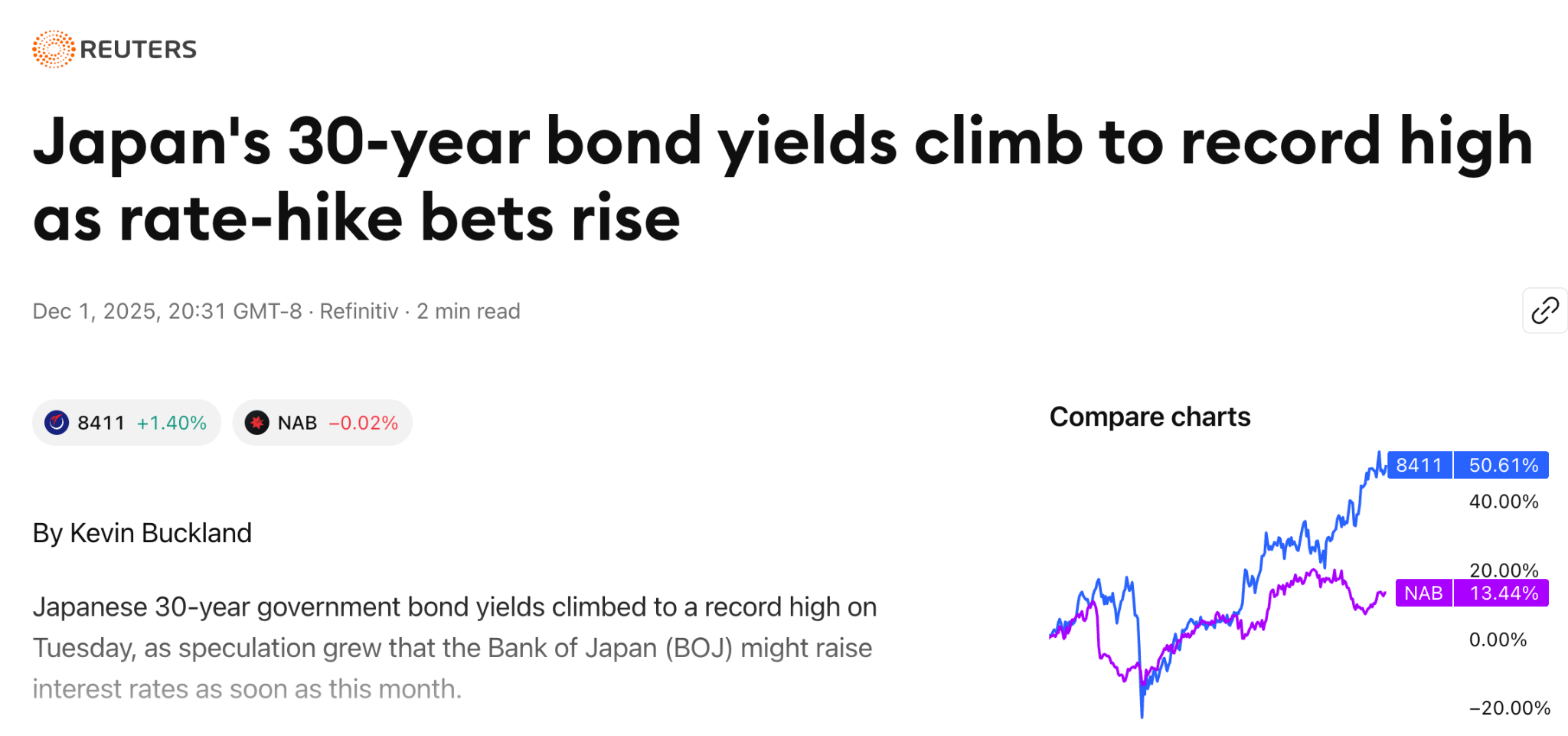

But the truly alarming action has occurred in the long end of the curve. The 20 year JGB yield reached 2.975% after the BoJ’s December meeting, its highest level since 1999, while the 30 year yield climbed to a fresh all time record of 3.445%. The 40 year yield, introduced only in 2007, has similarly reached unprecedented territory above 3.5%.

Source: TradingView

Even the short end has moved sharply. Japan’s 2 year yield rose to its highest level since 2008 following comments from BoJ Governor Kazuo Ueda that brought a December rate hike into focus. The 5 year yield reached a 17 year high. The entire Japanese yield curve has been repriced, and the repricing is accelerating.

What makes this especially remarkable is the sheer size of the market being repriced. Japan’s government bond market totals approximately 1.06 quadrillion yen, roughly $7.8 trillion at current exchange rates. This is the second largest sovereign debt market in the world, and it has experienced more volatility in 2025 than it saw in the previous fifteen years combined.

SPONSOR:

Taking self-custody of your Bitcoin has never been more critical, and that’s exactly why the team at Blockstream has created the perfect solution: the Jade Plus hardware wallet.

Secure your Bitcoin this holiday. 21% off all Blockstream Jade devices.

Use Code PB10 for an additional 10% off your JadePlus Wallet! Click the Link here.

For those unfamiliar with fixed income mechanics, a brief reminder: bond prices and yields move in opposite directions. When yields rise, the market value of existing bonds falls. Due to something called convexity, this relationship is particularly punishing for long duration instruments, where a one percentage point increase in yield can translate into a price decline of 15% or more for a 30 year bond.

The math is unforgiving. Japanese institutional investors, pension funds, and life insurance companies have accumulated massive positions in long dated JGBs over the past decade, drawn by yield curve control policies that made duration risk seem manageable. Those positions are now underwater, and the losses are mounting with each basis point move higher in yields.

Consider this: a 30 year JGB purchased in late 2020 when the yield stood near 0.6% has experienced a price decline of roughly 40% as yields have surged above 3%. An investor who bought 40 year paper yielding 0.5% has seen even more catastrophic losses. This is not theoretical; these are real positions held by real institutions, and the losses are staggering in aggregate.

That’s the insane power of convexity. We’re talking about potentially trillions of dollars of losses on JGBs spread throughout the Japanese banking and financial system.

The clearest evidence of market stress came in May 2025, when Japan’s 20 year bond auction attracted the weakest demand since 2012. The “tail” on that auction, measuring the difference between the lowest and average accepted prices, reached its widest level since 1987, a clear signal that buyers were demanding significant concessions to take down the debt.

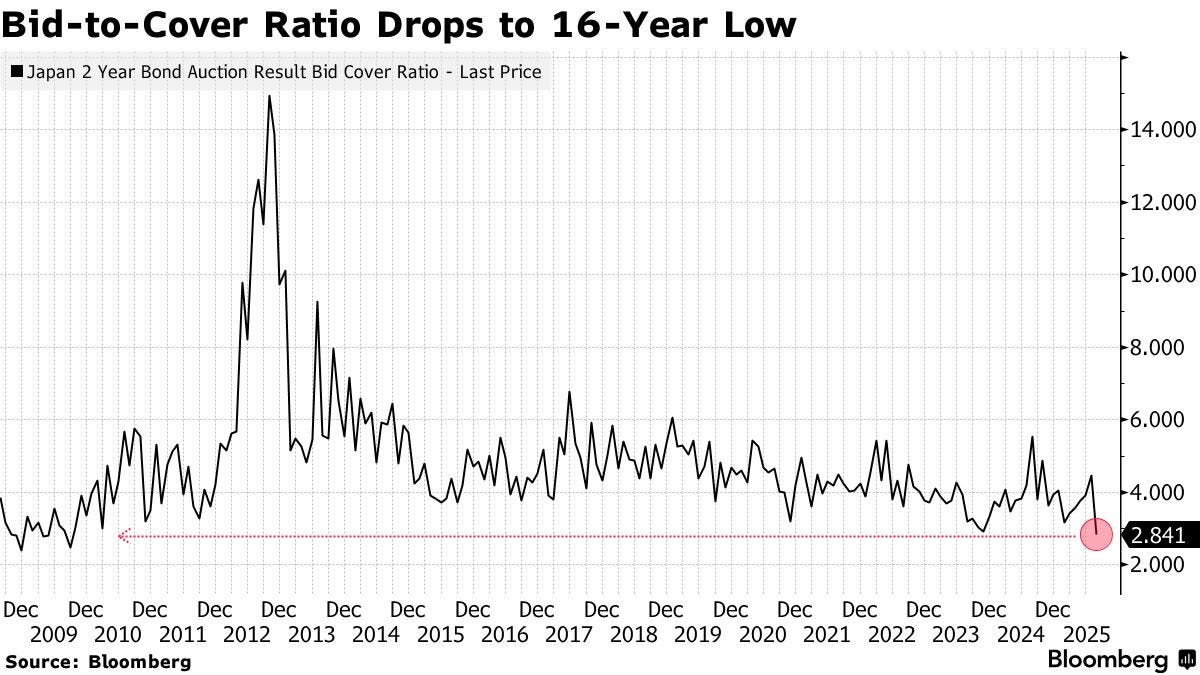

And it’s not much better in the two year bond market. As you can see, bid-to-cover there recently dropped to a 16 year low.

The rout in that auction drove up the 20 year yield by roughly 15 basis points in a single session, pushing it to the highest level since 2000, while the 30 year yield climbed to the highest since that maturity was first sold in 1999. The 40 year yield hit a record high ahead of its own auction the following week, which also showed weak demand amid fiscal concerns.

The Ministry of Finance was forced to respond. Following the disastrous auctions, officials circulated a survey among major bond buyers and announced they would consider reducing issuance of super long bonds to manage the rising yields. This provided temporary relief, but the fundamental problem remains: there are simply not enough buyers at current yield levels to absorb the supply of Japanese government debt.

Traditional domestic buyers, particularly life insurers, have grown cautious. Japanese life insurers held approximately 13% of total outstanding JGBs as of early 2025, making them the second largest investor group after the Bank of Japan. But heightened volatility and low liquidity have deterred these insurers from buying more of Japan’s sovereign bonds, increasing upward pressure on yields.

The proximate cause of Japan’s bond market upheaval is the Bank of Japan’s gradual withdrawal from its role as buyer of last resort. For years, the BoJ acted as what market participants termed the “whale” of the JGB market, gobbling up massive amounts of sovereign bonds to suppress yields through its Yield Curve Control program and quantitative easing operations.

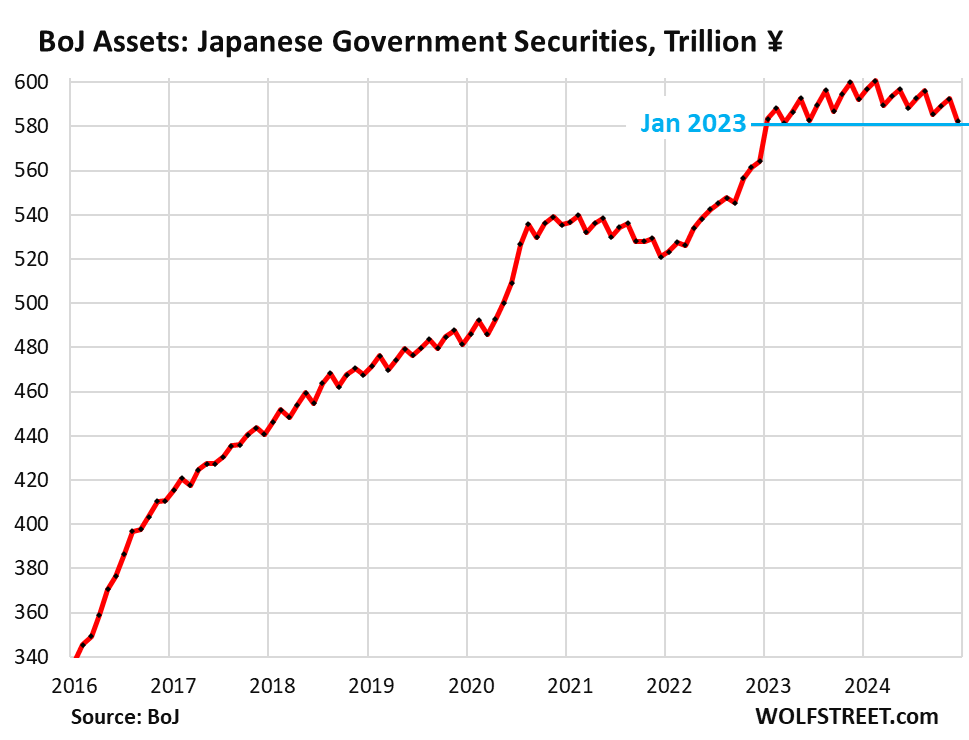

Source: Wolf Street

At its peak, the BoJ owned more than 50% of all outstanding JGBs and more than 70% of certain issuances. This dominance had a paradoxical effect: by removing so much supply from the market, the BoJ created the illusion of stability while actually building up enormous latent selling pressure.

The unwind began in earnest in July 2024, when the BoJ announced a quantitative tightening plan aimed at halving monthly purchases from approximately 6 trillion yen to 3 trillion yen by March 2026. As of the central bank’s June 2025 statement, the BoJ reduced the planned amount of monthly JGB purchases to about 2 trillion yen by January to March 2027, cutting the amount by roughly 400 billion yen each calendar quarter through early 2026, then slowing to 200 billion yen reductions per quarter thereafter.

The BoJ has already shed 18 trillion yen ($114 billion), or 3.1%, from its peak JGB holdings reached in February 2024. Its holdings now stand below where they were in January 2023. This is a historic shift; for the first time in over a decade, market forces rather than central bank intervention are determining where JGB yields trade.