Past the Event Horizon

The newest debt figures show the exponential rise of the national debt has only accelerated. Is there any hope for the beleaguered U.S. Treasury?

Black holes are fascinating things. Floating in the dark expanse of space, massive gravitational wells lurk, with gravitational forces so strong they bend and pull all matter towards their Singularity. The Event Horizon, the invisible dividing line beyond which even light itself cannot escape, surrounds a black hole- hence why it is “black”. Scientists are still not sure what exactly lies beyond this boundary, besides the obvious excruciating death of whatever decides to journey towards the Singularity.

This phenomenon in many ways is an apt metaphor for our current fiscal paradigm.

In early October, we got the first debt numbers for the government’s new fiscal year, which ends September 30th. Shockingly, the figures were much worse than expected- debt was up $204B in a single day and $347 over the weekend, bringing the total to $35.6T on October 2nd and $35.7T today.

That’s $105K for every single person in America, and $271K per taxpayer.

Many were asking me on Twitter how this could happen. In reality, it’s actually quite simple. The debt was racked up over the past several hundred years, by politicians from both parties, during wartime and peacetime. The debt began to explode after 2008, and even more so after 2020, as the government spent lavishly on COVID relief and PPP loans.

Then inflation came, and after a year of “it’s just transitory” pronouncements, something had to be done.

So Powell began the fastest rate hike cycle in history, blowing even Volcker out of the water with the speed of the increases- hoping to do just as the infamous 1980s had done, and break the back of inflation.

The Fed succeeded (sort of), and inflation moderated. However, the new price to be paid was the ratcheting interest expense cost on the national debt. In November of 2023, Bloomberg reported for the first time that the annualized cost of U.S. debt would surpass $1T for the first time in history.

This is the disastrous result when you hike 500 basis points within 18 months on a debt load over $33T. And sadly, this is only accelerating.

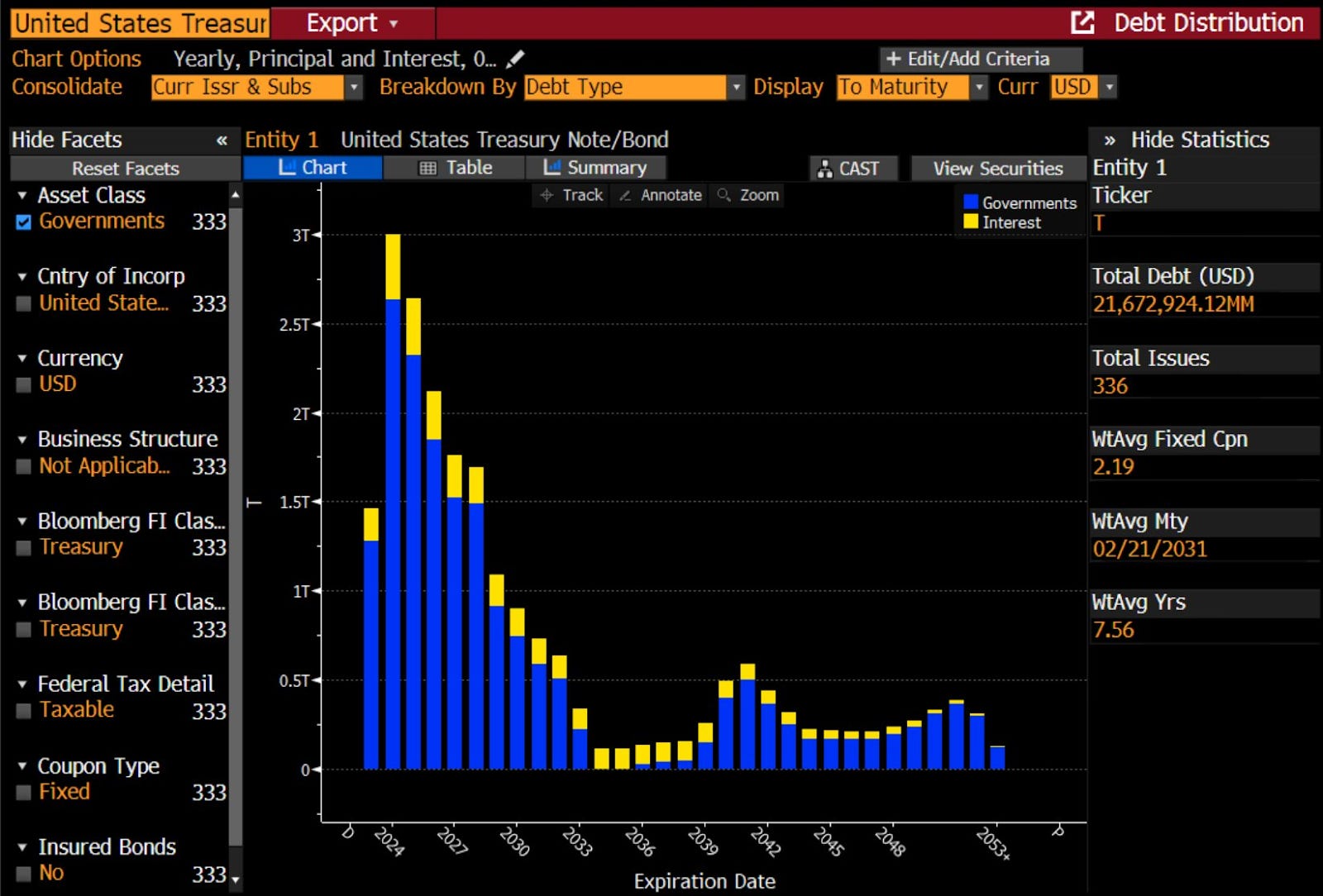

With a massive $7-9T of debt rolling over during this hiking cycle, all these securities are being refinanced at much higher rates, causing interest payments to spike. The Treasury must refinance all debt securities because they can no longer functionally pay them off; this means they are rolled continuously into the future, new debt offerings paying off maturing ones. As the interest rate rises on the debt, so do the payments, which means more debt must be issued, often only when the balloon payment comes due at the end of the life of the bond, which causes huge increases in the national debt periodically, like we saw at the beginning of October.

With all this debt refinanced at these higher rates, we should expect more spikes in the national debt to come. This will only add to the acceleration of the parabolic debt growth that we have already been witness to, despite the admonitions of the CBO, which are too conservative already.

The Treasury has been changing their issuance schedule as demand has shifted in the past few years. This began last year, as changes to the Quarterly Refunding showed reduced issuance on the long end and increases in bill issuance on the short end. In fact, an astonishing 71% of all government spending in the first 3 months of this year was funded by T-bills! This trend is continuing this year as well, as we can see here from this auction table from Treasury. Issuance of the 10yr, 20yr, and 30yr bonds is falling by 3 billion for each issuance over this 6 months period, and the only bond that is seeing a growth in supply are the FRNs, which stands for Floating Rate Notes. These instruments pay a variable interest rate that is set to the discount rate of the most recent 13-week Treasury bill issuance, plus a spread which is determined by the discount rate on the FRN itself at auction.

These securities mature in two years, making them similar to 2 yr Treasury notes.

Functionally, this is how you deal with low demand on the long-end of the yield curve; simply reduce issuance. But these actions are the stuff of poor countries, economic backwaters like Venezuela or Argentina. The rule of thumb for state treasury financing is 80/20: 80% funding on the long end and 20% on the short end. This is done because there simply isn’t enough demand for long term debt from investors. Nobody wants to lend to irresponsible sovereigns for any period longer than a year or two.

Look at Turkey’s maturity profile as an example. Here, literally 85% of the maturities have to be rolled over in under 8 years, with the highest amount under the 5 year mark.

This is the stuff of banana republics.

More evidence for the U.S. entering an emerging market crisis came a few weeks ago during a Macrovoices podcast with one of my favorite analysts, Luke Gromen. On the surface, Erik Townsend notes that foreign holdings of U.S. Treasuries are going up- ostensibly, the Almighty Dollar remains King and no matter how horrible the domestic fiscal situation is, foreigners will always buy our bonds.

U.S. Treasuries will ALWAYS be in demand.

Right?

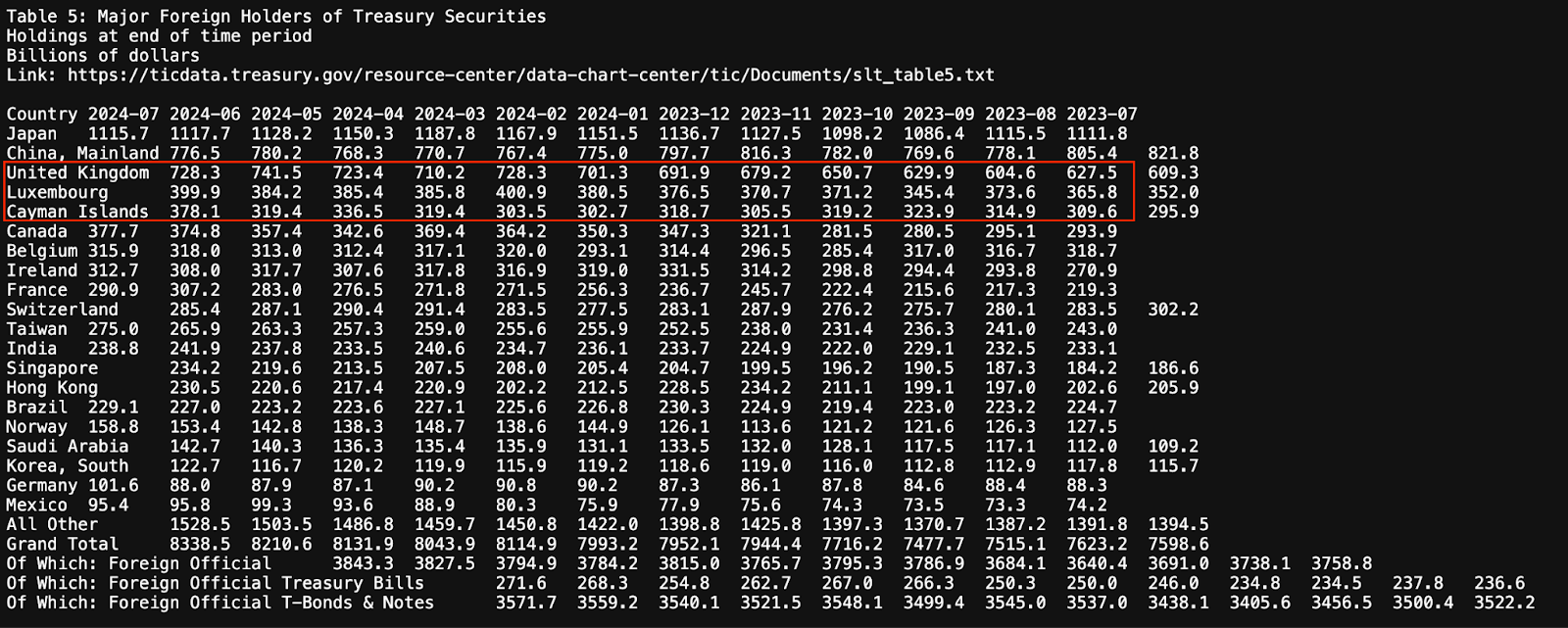

Gromen points out that the U.S. has shifted from being financed by patient creditors, such as central banks and Japanese pension funds, to relying on more unpredictable creditors based offshore. The headline news that dollar bulls paraded around was that foreign holdings of U.S. Treasuries hit a record high, but upon a closer look, it revealed that major creditors like Japan and China, the top two holders, have been selling U.S. Treasuries throughout the year. Japan remains the largest foreign holder, followed by China, but both have reduced their holdings.

The third largest creditor is the UK, which is surprising given that the UK is dealing with twin deficits and a fiscal situation comparable to the U.S. The true reason behind their large holdings is London’s status as a global financial hub, meaning the purchases come largely from investors and hedge funds, who are more profit-driven and less stable than central banks. Similarly, the fourth largest creditor, Luxembourg, is a small tax haven, also reflecting a shift towards family offices and hedge funds. See the Treasury TIC data below:

The fifth largest holder is the Cayman Islands, a small island with just 68,000 people, yet Gromen points out they accounted for more than half of foreign U.S. Treasury purchases in July, likely through hedge funds and other tax shelters. Ireland, ranked seventh, also acts as a tax haven for U.S. corporations, which is why their holdings of Treasuries have increased as well.

Overall, since 2014, Luke states the U.S. has moved away from being financed by stable, politically motivated creditors like global central banks to relying more on private, profit-seeking entities in tax havens.

This is worrying because this trend is part of what a country experiences in their transition to banana republic- not only do they shift the issuance of their bonds to the short end, but the makeup of investors who buy their bonds changes also. Hedge funds, family offices, and other professional investors come in to buy and trade bills and short term bonds, but most of these firms won’t hold them for the long term. The pension funds leave, and the traders fill their place.

This is happening as the U.S. moves past the Monetary Event Horizon, something I discussed in a piece with the same name last July. This is a concept I created for the financial point of no return- where the financial gravity of the debt grows so large that not even the powerful U.S. Treasury can escape. Functionally, there can be multiple event horizons: the point at which annual debt growth exceeds GDP growth, or when debt to GDP exceeds 120% (something Hindenburg Research found has caused an inflationary crisis or depression in 54 out of 55 countries in the last 150 years, with the only exception being Japan), or when interest on the debt exceeds tax receipts.

Each of these are progressively worse event horizons, with the last one being crucial since it means the debt will functionally NEVER be paid off.

In October of 2021, Gromen pointed out in another Macrovoices podcast that U.S. true interest expense (which he defines as gross interest + entitlements + defense spending) reached an astonishing 111% of federal tax receipts: meaning all taxes taken by the government couldn’t even cover the interest on our liabilities!

Luke now points out that even when you cut out defense spending which makes this calculation more conservative, the gross interest on the debt and unfunded liabilities now is close to 100% of tax receipts. Recently, this figure was 120% of July receipts and an incredible 150% of August receipts! These are worse months than average for Treasury income, but this paints a grim picture.

What this means is that the United States is quickly hurtling past the point of no return, with debt levels quickly going parabolic due to the ratcheting effect of the debt. This trend is EXPONENTIAL, with no signs of slowing down. In fact, we’ve added over $2.7T of debt in just the last year.

Last year, in preparation for a presentation on the Dollar Endgame, I ran a polynomial regression analysis on public Treasury data with the help of my intern- we found the actual equation that reflects the true growth rate of our national debt. You can see the equation here:

Let’s look at it in a graph format for the visually inclined:

This graph is based on actual Treasury data pulled from FRED- the red dots are debt levels by quarter, with a large jump in 2020 as government spending ramped up during the COVID pandemic.

As you can see, this is an exponential problem. Which means it’s going to get worse, and increasingly worse, every single year. This is hard for most humans to grasp; we’re used to thinking in linear systems with static relational variables.

But many will retort that the Congressional Budget Office (CBO) knows this, and they’ve produced forecasts warning that we are on an unsustainable path. Nothing new, right?

“In CBO’s projections, the federal budget deficit in fiscal year 2024 is $1.9 trillion. Adjusted to exclude the effects of shifts in the timing of certain payments, the deficit amounts to $2.0 trillion in 2024 and grows to $2.8 trillion by 2034.

Relative to the size of the economy, debt swells from 2024 to 2034 as increases in interest costs and mandatory spending outpace decreases in discretionary spending and growth in revenues. Debt held by the public rises from 99 percent of GDP this year to 122 percent in 2034, surpassing its previous high of 106 percent of GDP.”

However, even these somber predictions are made through rose-colored glasses. If you look closely at my graph, you can see the blue line tracing upwards, which is the model’s prediction for the next 5 years. Using our own equation, we find that the U.S. reaches $40T in total debt in the middle of 2027, something that the CBO doesn’t expect to happen until 2031.

Revision (10/16/2024 4:17pm PST):

The debt figures used by the CBO only reference debt held by the public, while our initial model used total U.S. debt. Once adjusted, we still find that we reach $40T in total debt two years sooner than the CBO predicts. Although not as drastic as the initial comparison, the point is still true.

The national debt path is parabolic, and the process has already begun. As all polynomial functions go, this one will get worse and worse with time.

The shifts in issuance and the types of creditors buying our debt are just more warning signs along the path towards financial ruin; gravestones that mark the place where many a sovereign have died before. As we continue, debt levels will grow exponentially, flooding the system and forcing Treasury and the Federal Reserve to make new drastic changes to swallow the ever-growing torrent of bonds.

As I stated in the Dollar Endgame book:

“The terrifying truth is that we’re not approaching the event horizon.

We’ve already passed it.”

What a fantastic look into the "business end" of the monetary machine!

The sinister reality is: this was all by design.

It appears the plan is to devalue US Debt by devaluing the US Dollar. Trump wants to protect USD but the US-wing of the 300 / Club of Rome are content with a great transfer of wealth from America to China, pockets of Europe and globalist concerns in general.

The printing will continue until morale improves.

So what’s the prevailing investment thesis to profit from a US debt crisis? Commodities, crypto, and what?