QE is Coming

Markets are front-running a new wave of liquidity injections from the Fed.

Gold and Bitcoin are ripping to fresh all-time highs, even before the Fed begins their long-awaited easing cycle. Is this bull market exuberance? Or a warning of something to come?

This week, investors watched with rapt attention as Bitcoin rallied to a new all time high above $69,000. The last time BTC traded here was almost 3 years ago on November 10, 2021- in the middle of a Fed easing cycle.

It ripped up before being slammed back down to $59k, a $10k daily handle. Most of this price action appears to have been selling pressure from several large whales who started dumping once the previous all time high was broken.

The huge surge in bitcoin's value is mostly due to the significant purchasing activity by the recently launched U.S.-based spot bitcoin Exchange-Traded Funds (ETFs), marking a historic rally. When these ETFs began operations on January 11, bitcoin's price was around $45,000. Despite a short-lived downturn to the $39,000 range, often referred to as a "sell the news" dip, bitcoin's price swiftly soared past $50,000 by mid-February. The ETFs have been seeing massive inflows, easily 10x that of the gold ETFs. In fact, some days have seen gold ETFs being drained and BTC ETFs rising by a similar amount.

Gold itself is not doing too bad however- despite the gold ETF outflows, the price of the yellow metal is also soaring to an all time high. But why?

Bitcoin, and gold to a lesser extent, serve as inflation hedges on steroids. Essentially, these two alternative currencies, which have been hated by central bankers since time immemorial, have sniffed out currency games even before they have occurred. In August 2020, just as the Fed was ramping up QE, gold had soared to its previous ATH of $2,070, getting ready for another round of inflation that would come 12 months later. However, it spent the next few years in retracement and consolidation before roaring back in the last few months.

The fact that these two assets are breaking all time highs without a catalyst- no Fed QE cycle, no cutting rates, no bank failures- is massively bullish. It is also indicative that the markets are front-running something that will force the Fed to do one of these things- something I pointed out in my January newsletter:

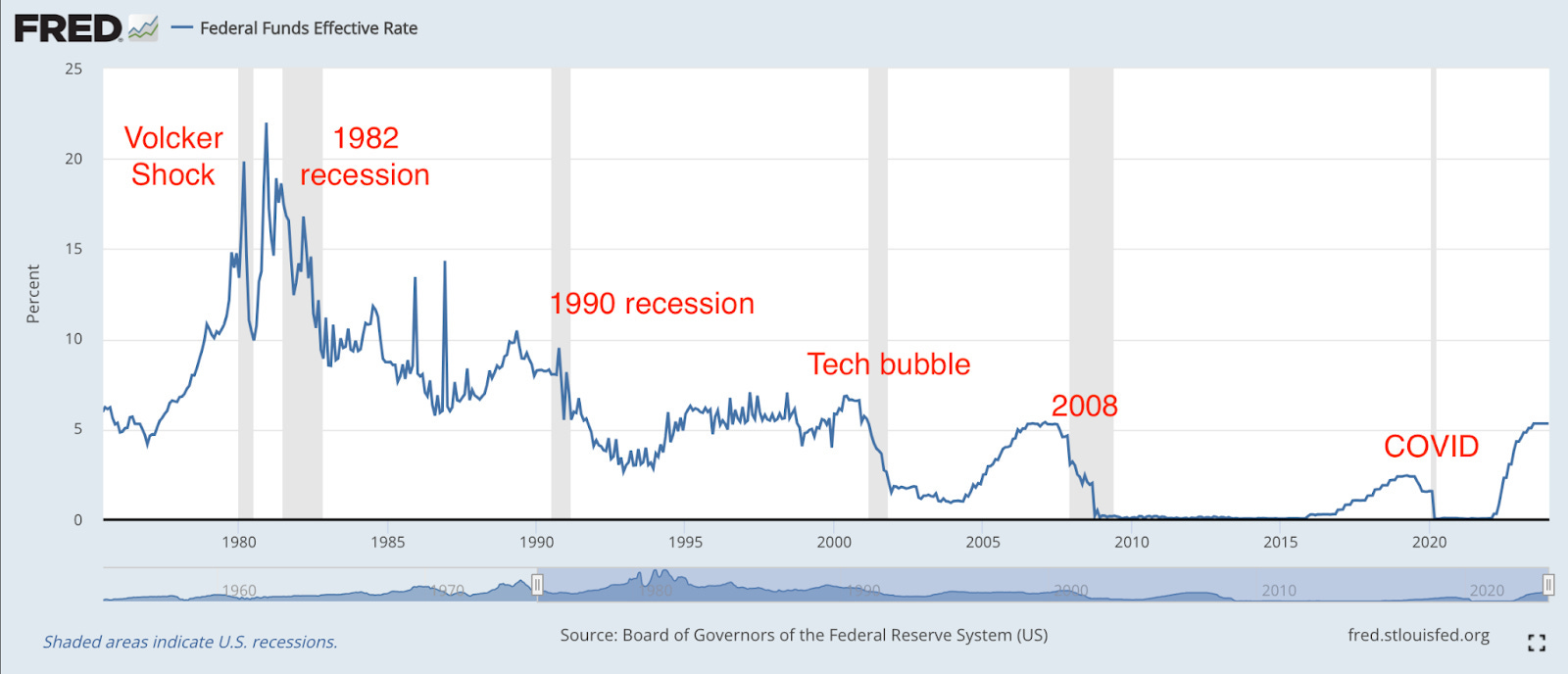

To begin with, the Fed has never done a slow and steady cutting cycle. If you look at a historical chart of the Fed Funds rate, they have always hiked slowly until they reach a crisis, breaking something major in the financial system. So essentially the inverse is true.

The ONLY slow cutting cycle was 2 years in the mid- 1980s, when the repercussions of the Volcker Shock were being unwound, debt to GDP was 35%, globalization was in full swing and Japan was fully online buying hundreds of billions of Treasuries. So, with that exception, every time they have signaled a slow cutting cycle, but ended up panicking and frantically slashing rates as fast as they could- of course never predicting the crisis that would cause this reaction.

But front-running the Fed does not have to be the only answer. The actual solution might be staring us right in the face- and was already discussed in the aforementioned newsletter.

Net liquidity is RISING.

(You can read a longform post on Net Liquidity here- explaining the history and how to calculate it)

Despite the fact that the Fed has been on a supposed taper, and balance sheet reduction is on “autopilot” until inflation reaches Powell’s goal of 2%, the actual balance sheet mechanics beg to differ. This is mainly due to a large drawdown in Reverse Repo, the war chest that Powell built up during COVID and is being drained to help alleviate the funding pressures brought on by the Taper. In fact, this drawdown is accelerating, moving from a rate of roughly $50B a month in mid 2023 to a staggering $200B a month by December 2023. At this rate, the entire window will be drawn down to nothing in April.

It currently sits at $444B, down from $2.2T at its peak. RRP serves as a store of liquidity for markets, shoving excess funds onto the Fed’s balance sheet where they are locked out of the system. Crucially, the BTFP is also slated to end this month, with the Fed saying in a statement:

On January 24, 2024, the Federal Reserve Board announced (Off-site) the Bank Term Funding Program (BTFP) will cease making new loans as scheduled on March 11, 2024.

With these two sources of liquidity gone, the markets will be adrift, unmoored from the steady injections of cash from the Fed, with the only hope coming from the global liquidity tsunami forming in Japan and China. In fact, last month the People’s Bank of China injected money to stabilize the repo market. Normally, China's money market faces the risk of liquidity shortages ahead of the annual one-week Chinese New Year holiday in mid February, as bank customers withdraw more cash than usual for gifts and travel. However, the chance of a squeeze was lower this year, as Beijing injected 1 trillion yuan ($139 billion) into the financial system on February 5th. This move aims to “support the economy” during a significant economic contraction that started last year pushing China into deflation.

In Japan, the Nikkei Index also rallied to a new all time high- despite the fact that economic growth there is sluggish and inflation remains stubbornly high. Japan’s stock market now has finally eclipsed the peak made in December of 1989, after which the stock market bubble burst and traded sideways for 30 years. The only thing that revived the faltering equity index was the record monetary stimulus program pursued by the Bank of Japan.

All of these occurrences are indicative that markets are getting prepared for something big to break- and an even larger liquidity wave to follow. As I discussed in a stack post last November entitled Ayahuasca and the Simulacrum, the Fed has broken the fundamental pricing mechanism of the market. Prior to 2008, asset prices in general (mostly) reflected real supply and demand, and when economic contractions occurred, the indexes fell in tandem. After the record QE and TARP programs, markets fundamentally changed. With each crisis, the Fed met the sell wall with a tsunami of freshly printed money- training participants to NEVER fight the Fed. Buy the Dip

Now, the system is completely dependent on central bank liquidity- and it is getting ready for a new round of injections. The Fed never cuts slow and steady. What is going to break and how big will this next liquidity wave be?

I already see a (commercial real estate) canary in the coalmine….

Financial melt up after a well-timed, economic collapse on an election year? Is this a callback to an old re-run?? It feels like I’ve heard this story somewhere before…