Shades of 2008?

Warning signs are brewing in the commercial property market, and contagion is already beginning to spread to Europe. Are we seeing the CRE version of the Financial Crisis?

The commercial real estate market is currently facing a perfect storm. Over the last two years, the impact of stricter financial conditions on the value of commercial properties has been exacerbated by trends like teleworking and e-commerce. These have significantly reduced the demand for office and retail spaces, leading to increased vacancy rates.

Prices have experienced a decline throughout the sector, and the current cycle of monetary policy tightening has contributed to a rise in delinquency rates on loans backed by these properties.These obstacles become even more formidable with the looming high volume of refinancing obligations. The Mortgage Bankers Association estimates that approximately $1.2 trillion of commercial real estate debt in the United States is set to mature within the next two years. The majority of these loans are held by banks and investors who own commercial mortgage-backed securities (CMBS).

The Association states:

The analysis estimates that of $4.4 trillion of outstanding commercial/multifamily mortgages, $728 billion (16%) matures in 2023 with another $659 billion (15%) maturing in 2024. Hotels/motels see the largest share maturing in 2023 (34%) followed by office (25%). Multifamily is the property type with the smallest share of outstanding mortgage maturing this year, (9%).

Among capital sources, 26 percent of the outstanding balance of loans held by credit companies and other investor-driven lenders will mature this year, as will 23 percent of the balances held by depositories and 22 percent held in CMBS. Only 7 percent of life company loans and 2 percent of GSE/FHA loans come due this year.

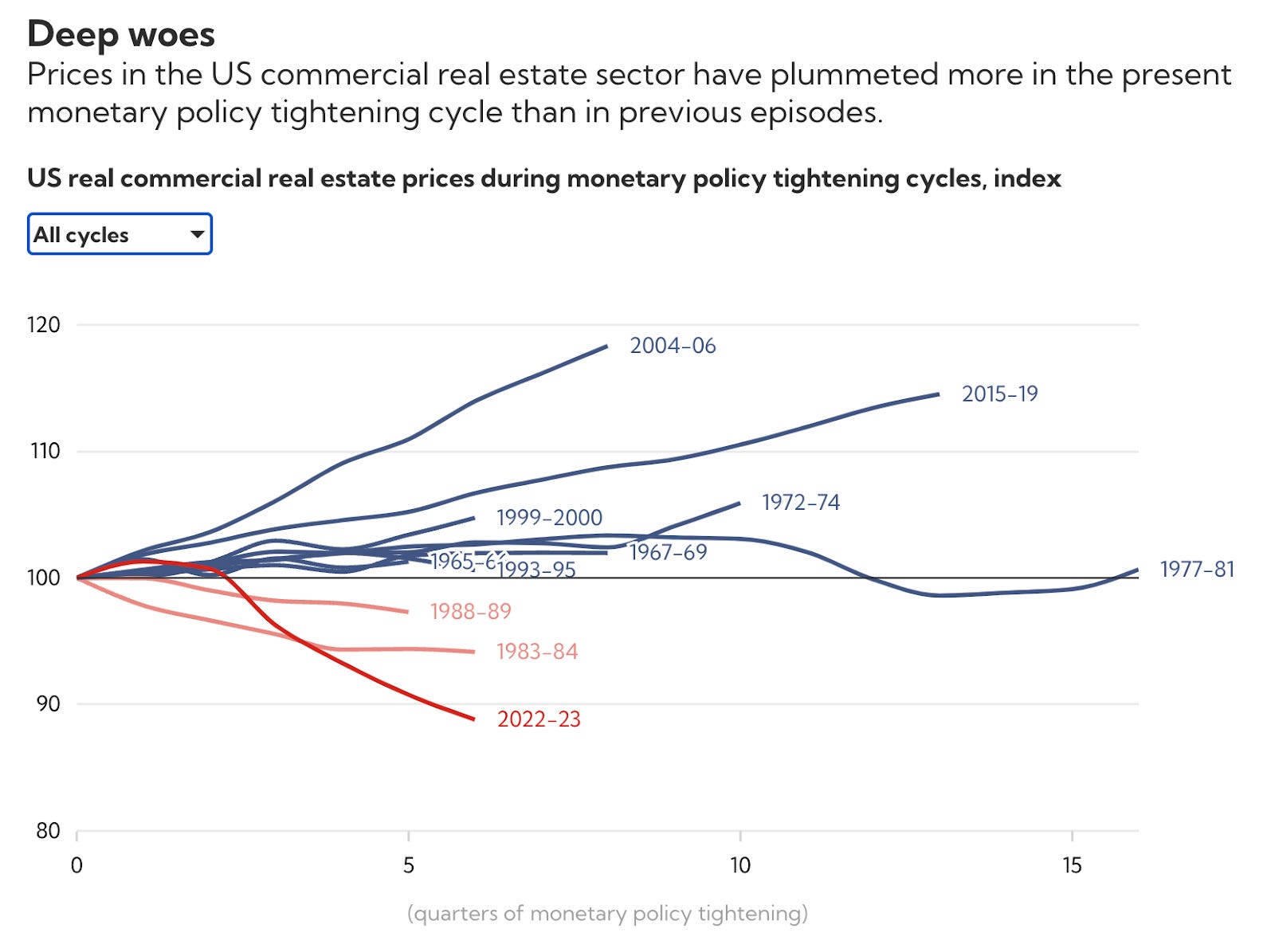

In the US, which is the world's largest commercial property market, prices have experienced an 11 percent decline since the Federal Reserve initiated interest rate hikes in March 2022. This decline has effectively destroyed the gains observed in the two years leading up to the tightening cycle.

Morgan Stanley's Chief Investment Officer, Lisa Shalett, has sounded an alarm regarding commercial real estate lending rates. Even if interest rates remain steady, the projection is that new lending rates for commercial real estate (CRE) will surpass existing mortgage rates significantly. This forecast will affect a considerable number of banks, with an estimated 190 facing challenges akin to those witnessed by Silicon Valley Bank. Small- and medium-sized banks, constituting a substantial portion of CRE lending, are particularly susceptible in this scenario.

She stated:

“Commercial property prices have already turned down, and Morgan Stanley analysts forecast prices could fall as much as 40%, rivaling the decline during the 2008 financial crisis. These kinds of challenges can hurt not only the real estate industry, but also entire business communities related to it.”

Smaller and regional banks in the US are at a higher risk, being nearly five times more exposed to the commercial property sector than their larger counterparts. The commercial property sector also presents risks in other areas, such as Europe, where many of the same dynamics seen in the US are also in effect.

In fact, we’ve seen signs of this already.

A large German lender Deutsche Pfandbriefbank (PBB) assured investors early in February that it was in good health after its stock price plunged. It is down 38% year to date, and 59% from a year ago. The bank has significant exposure to U.S. commercial real estate, around 15% of its book, and has reported that loss provisions for 2023 were €215M, compared to €44M in 2022.

The AT1 bonds of several German banks have begun plunging, including PBB. These bonds are perpetual interest bonds, meaning that investors don’t get back their principal but instead are paid continual coupons.

The bank itself said the current chaos is the

“greatest real estate crisis since the financial crisis.”

The bank tried to comfort the markets over their liquidity coverage ratio, emphasizing that it was twice what regulators require and would allow the bank to survive for 6 months without additional funding. But despite these statements, the bank saw one of its larger shareholders, the RAG Foundation, cut their ownership from 4.5% to 2.9% on February 9th.

Worries about PBB have extended to other German banks with exposure to CRE. Aareal Bank AG bonds, in particular, have seen a decline of approximately 4 cents in the past two weeks and are currently quoted at 80 cents on the euro. In November, the bank admitted a more than 300% jump in the value of non-performing loans in the US compared to the previous year.

To the shock of absolutely no one, another usual suspect is in trouble.

Deutsche Bank reported in early February that its losses in commercial real estate would be more than four times bigger than a year earlier. Its own analysts, however, are downplaying the risks at their and other German banks.

Julius Baer, a private bank in Switzerland, announced the resignation of Chief Executive Philipp Rickenbacher following the provision of approximately $700 million on loans to the Austrian property landlord Signa Group, which the bank deemed may not be recovered. In response, the group has decided to close down the unit responsible for issuing the loans.

In Japan, the contagion was also evident as Aozora Bank's shares experienced a maximum limit crash on Thursday, February 1st. This occurred following the company's projection of a full-year loss attributed to overseas real estate loans and its caution that it might take years for the stabilization of the US office market.

The lender adjusted its earlier projection of a ¥24 billion ($164 million) profit for the fiscal year ending in March to a net loss of ¥28 billion. This led to a fall of over 21 percent in the bank's shares in a DAY, which had been trading near a five-year high prior to the announcement.

Aozora clarified that the majority of its office loans are situated in major cities like Chicago and Los Angeles, constituting 6.6% of its overall loan portfolio. The bank holds a U.S. office-loan portfolio valued at $1.89 billion.

Lending in the commercial real estate sector is contracting to levels not seen in recent history, posing a threat of increased defaults on maturing debt and a significant drop in the construction of new warehouses, apartments, and various other types of properties.

However, the stories abound of office buildings in prime locations selling for deep losses:

Brokers in Manhattan have started to sell debt tied to an office building owned by Blackstone Inc. at a discounted rate of approximately 50%.

In December, a prominent office tower in Los Angeles sold for approximately 45% less than its acquisition price a decade ago.

Also in December, the Federal Deposit Insurance Corp. sold approximately $15 billion in CMBS, secured by New York City apartment buildings, at a whopping 40% discount.

The declining property values in the United States are resonating globally, as top-tier American cities were once considered attractive for international lending. Offices were regarded as extremely secure investments supported by high-quality assets featuring long-term leases and increasing rents. As we discussed with the property contagion in Europe and Asia, this is backfiring on foreigners.

In December, offices made up 41% of the value of distressed properties in the United States, totaling nearly $86 billion, as reported by MSCI. The potential distress, indicating the decline in an asset's current financial condition, spans almost $235 billion across all property types.

Apartments rank top of the list of potential distress, accounting for over $67 billion. More than 30% of this is buildings acquired in the past three years, often at the highest prices.

Certain lenders are covertly attempting to sell loan portfolios linked to CRE. Capital One Financial Corp., for instance, successfully offloaded a substantial office loan portfolio the previous year and has been actively marketing portfolios that include both performing and non-performing debts associated with offices and apartments in New York. Additionally, the Canadian Imperial Bank of Commerce is seeking buyers for approximately $316 million worth of loans tied to U.S. properties.

Several banks have been setting aside additional funds as a precaution against declining property values and possible defaults. Wells Fargo & Co. had allocated $3.9 billion for potential losses in commercial property by the end of the previous year, an increase from $2.2 billion the year before. U.S. Bancorp, the largest regional bank by assets, raised its reserves for credit losses in the fourth quarter by $111 million, a 28% hike compared to the previous year, citing commercial real estate concerns.

Major prime banks are better equipped to handle the upheaval due to their substantial reserves set aside for potential losses, along with their ability to leverage credit and capital lines in the markets and directly with the Fed. But, the challenges could be a lot more severe for smaller to medium-sized banks.

According to a report by Morgan Stanley on February 14, regional banks hold 70% of the commercial real estate debt due by 2025 that appears on bank balance sheets. The report also notes that regulatory changes affecting regional lenders could increase their liability costs and restrict their capital deployment capabilities, further increasing vulnerability.

All this comes as the Fed prepares to wind down the BTFP in March, which is up to $164B this month as banks and financial institutions post bonds and are lent funds at par, not the market value, of the collateral.

Admittedly, so far the crisis has not yet appeared to pose large risks to the financial system. In early February, Treasury Secretary Janet Yellen expressed concern over losses in the commercial real estate sector but described the situation as “manageable,” echoing sentiments shared by Fed Chair Jerome Powell during a "60 Minutes" interview on February 4. However, views vary widely, with real estate investor Barry Sternlicht forecasting office losses up to $1 trillion, a much more severe outlook.

Will they be correct? Or will their statements come back to haunt them, similar to the pronouncements made by previous Fed Chairman Ben Bernanke that “subprime is contained” and poses “no risk to the broader economy”? Time will tell.

Wouldn’t the fed cutting rates work against their fight with inflation? Especially since it’s still not under control. Might as well let this shit ride and blow up than making money worth less and less for everyday Americans.

Then again, when banks lose, everyone loses since they are ok with socializing losses. Capitalism is failing.

I'm both a beneficiary and a former director in the superannuation industry. Here in Australia it is mandatory contributions from workers. So, we have massive fund balances mostly drawn upon from government to fund not only the superannuation /pensions of the workforce but also to fund political promises. Much of which is invested in CRE. What comes next should be obvious.