The Fracture

As the postwar global order disintegrates, the world’s great powers are quietly choosing sides; and commodities are the new ammunition.

On January 3, 2026, the United States military executed a mission culminating in the arrest of Venezuelan President Nicolás Maduro, a man who had overseen the collapse of what was once one of the most productive oil states in the Western Hemisphere.

Within eight weeks, on February 28, the United States and Israel launched a joint military operation against Iran, killing Supreme Leader Ali Khamenei and much of the senior military leadership in a sustained campaign of airstrikes that President Trump warned could last weeks.

One common thread that nobody in the mainstream financial press wants to say out loud: Venezuela holds the world’s largest proven oil reserves at 303 billion barrels. Iran holds the fourth largest, plus controls the southern shore of a strait through which 20% of global petroleum liquids consumption transits every single day.

That’s not coincidence- that’s a grand strategy.

As I laid out in Sword of Damocles and the Dollar Endgame series, the weaponization of the dollar system was always going to trigger a counter-reaction.

The freezing of Russian reserves, the SWIFT ejections, the secondary sanctions: every one of these tools was a signal to the rest of the world that dollar-denominated assets held abroad could be confiscated at the stroke of a pen. The counter-reaction isn’t coming, it’s here.

And what we’re watching unfold across multiple theaters simultaneously isn’t a series of isolated foreign policy decisions; it’s the violent reorganization of a global order that has been quietly dying since 2008.

And commodities are the ammunition.

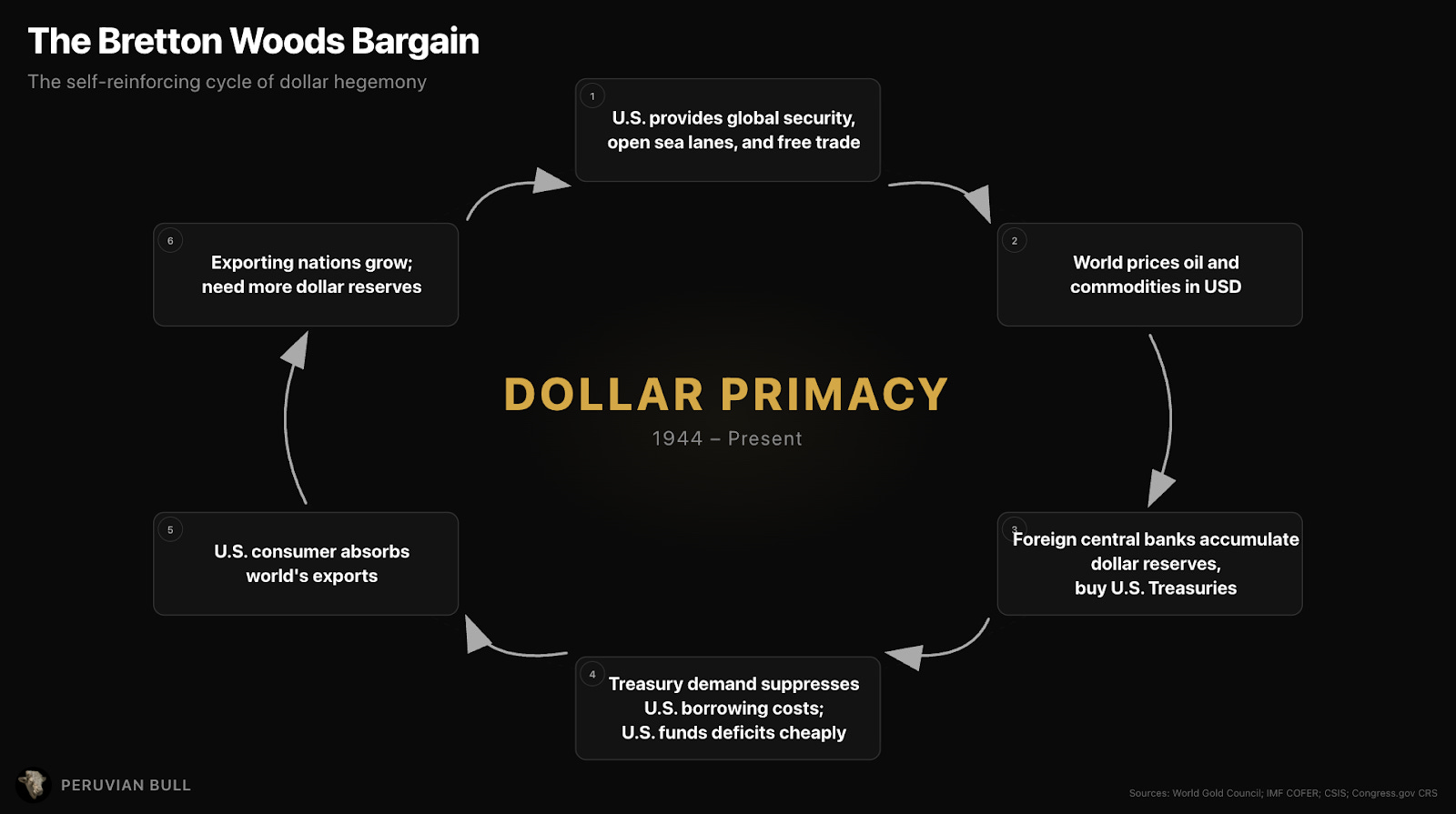

The postwar Bretton Woods system (and its zombie successor, the petrodollar recycling arrangement) rested on one core assumption: that the United States would provide global security, open sea lanes, and free trade in exchange for dollar primacy.

Every nation would hold Treasuries, price oil in dollars, and accept the Federal Reserve as the de facto central bank of the world. In return, the American consumer would absorb the world’s exports, and the U.S. Navy would keep the shipping lanes open for everyone.

This bargain is now being renegotiated.

With force.

Look at Venezuela.

SPONSOR: Bitcoin is freedom money, but only if you control your keys.

Partnering with Bitcoin Well, the world’s first publicly traded non-custodial Bitcoin company, ensures this freedom.

They send Bitcoin directly and instantly to your wallet.

No middlemen. No permission needed. Whether you’re stacking sats or making large moves via their OTC desk (Infinite by Bitcoin Well), you remain in control. Self-custody is essential.

Ready to buy Bitcoin the way it was intended? Head to bitcoinwell.com and enable your independence. Use this link https://app.bitcoinwell.com/signup?referral=peruvianbull to sign up and start stacking today!

Now let’s get back to it!

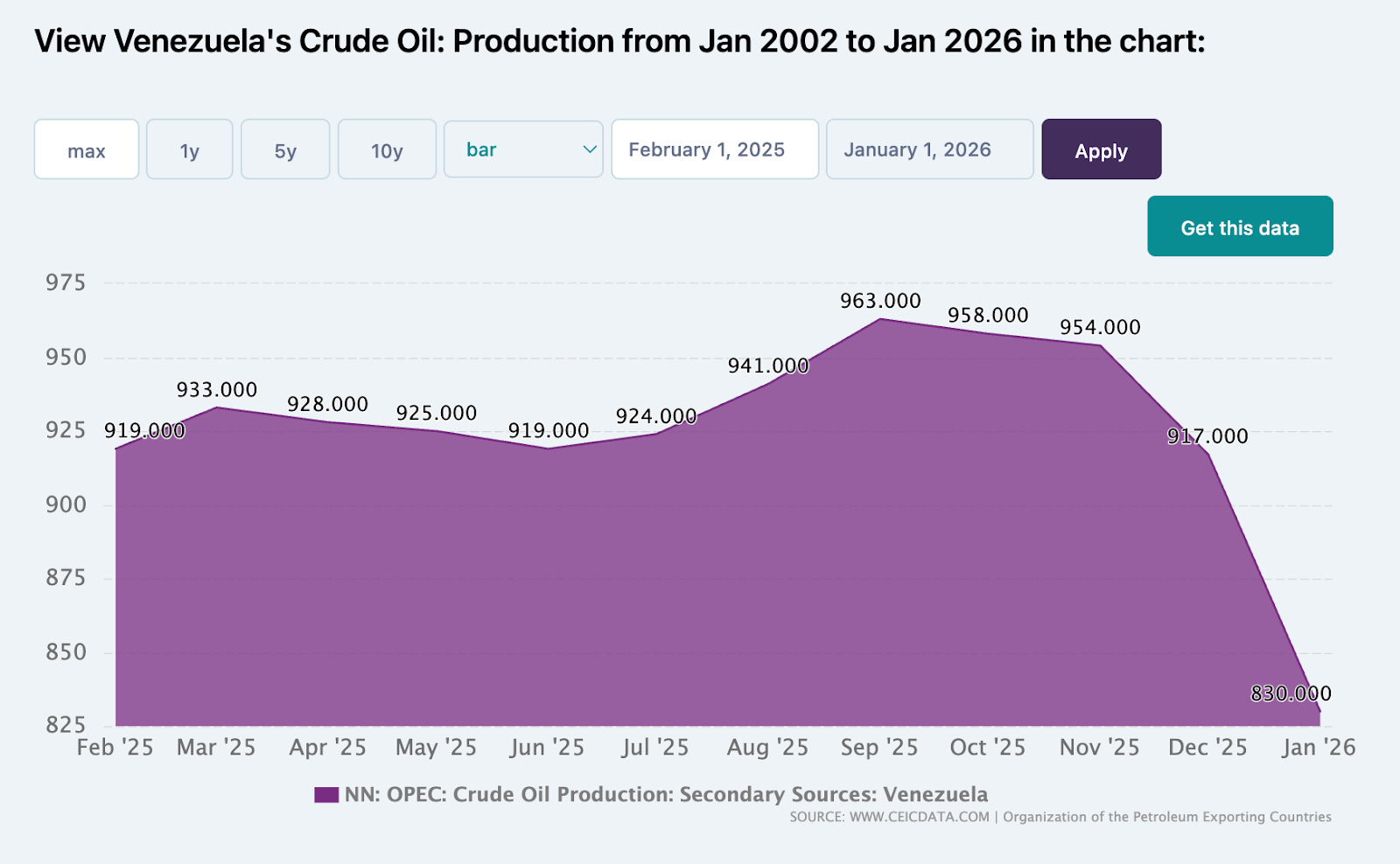

Hugo Chávez took power in 1999 with crude oil production running at approximately 3 million barrels per day. By the time Maduro was dragged out of Caracas in January, production had collapsed to roughly 830,000 barrels per day: a 72% decline driven by corruption, mismanagement, sanctions, and the systematic looting of PDVSA, the state oil company. Three hundred billion barrels of proven reserves sitting in the ground, and the country can barely pump a third of what it managed a quarter century ago.

Source: OPEC via CEIC Data

The Council on Foreign Relations estimates that restoring Venezuelan output to even 1.5 million barrels per day would require $10 to $20 billion in investment and several years of rehabilitation. Getting it back to its former levels? $100 billion over a decade, with the full participation of major U.S. oil firms like Chevron, ExxonMobil, and ConocoPhillips.

Secretary of State Rubio has reportedly noted that limiting “the involvement of U.S. foreign adversaries” is a central Administration focus. China and Russia both have billions invested in Venezuelan oil infrastructure; this is a direct challenge to their interests on the doorstep of the Western Hemisphere.

Monroe Doctrine 2.0.

Now turn to Iran. On June 22, 2025, the United States struck three Iranian nuclear facilities (Fordow, Natanz, and Isfahan) during the Twelve-Day War with Israel, deploying B-2 Spirit stealth bombers carrying GBU-57A/B bunker busters alongside Tomahawk missiles from a submarine. That was the appetizer. On February 28, 2026, the full meal arrived: a sustained joint U.S.-Israeli military operation code-named Operation Epic Fury that killed the Supreme Leader, destroyed military infrastructure across 24 of Iran’s 31 provinces, and targeted the IRGC leadership wholesale.

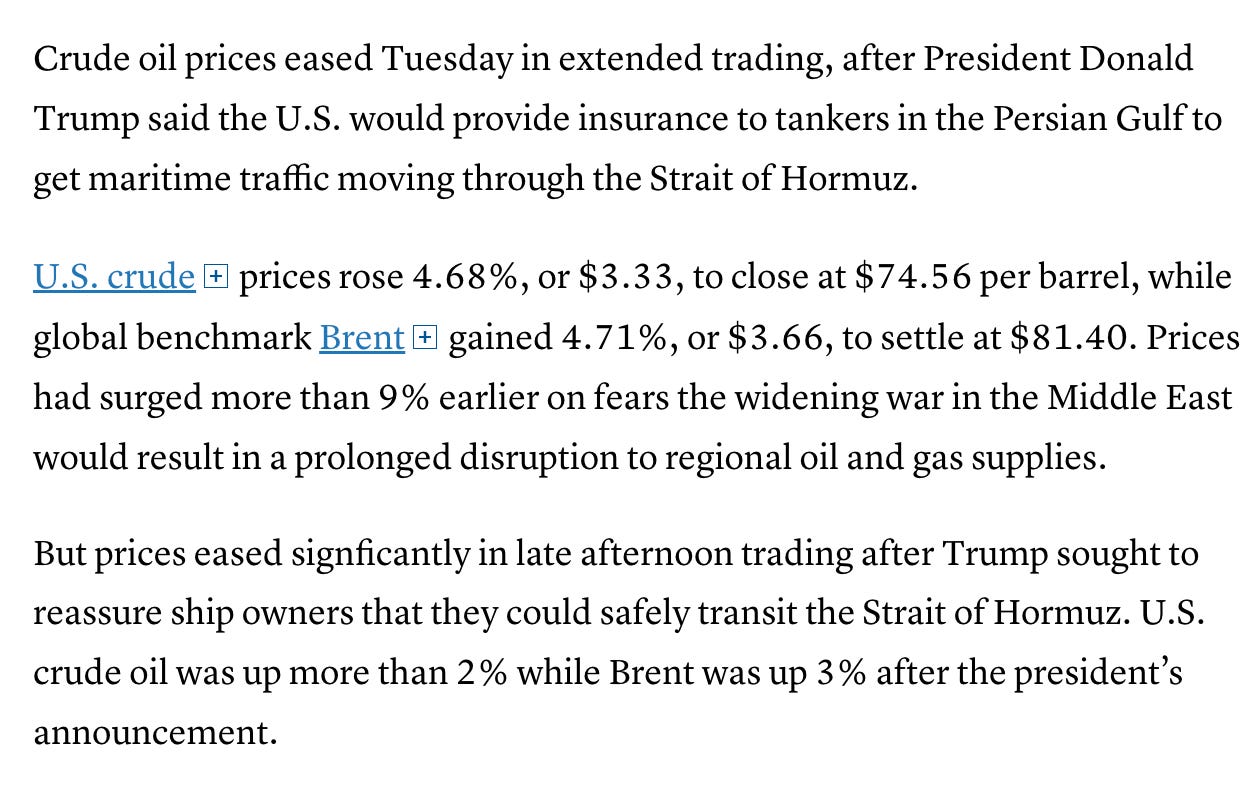

Iran retaliated immediately: missiles fired at Israel, U.S. military bases across all six Gulf Cooperation Council countries, and drone strikes on civilian airports in Kuwait and Bahrain. The IRGC declared the Strait of Hormuz closed. Shipping traffic through the strait dropped over 80% essentially overnight.

Brent crude surged above $82, its highest level since the June 2025 strikes, and analysts at both Barclays and UBS warned that sustained disruption could push prices above $100 or even $120 per barrel.

Source: U.S. Energy Information Administration

Here is the critical framing that most analysis misses. Venezuela and Iran are not separate stories. They are two prongs of a single strategic pivot: the United States is not withdrawing from the world. It’s reorganizing the world around bilateral power relationships where commodities and the dollar are the levers. The “rules-based order” still exists; it’s just that the rules are being rewritten in real-time by the country that wrote the original ones.

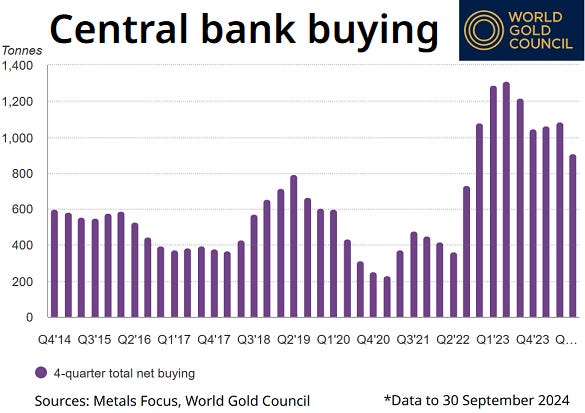

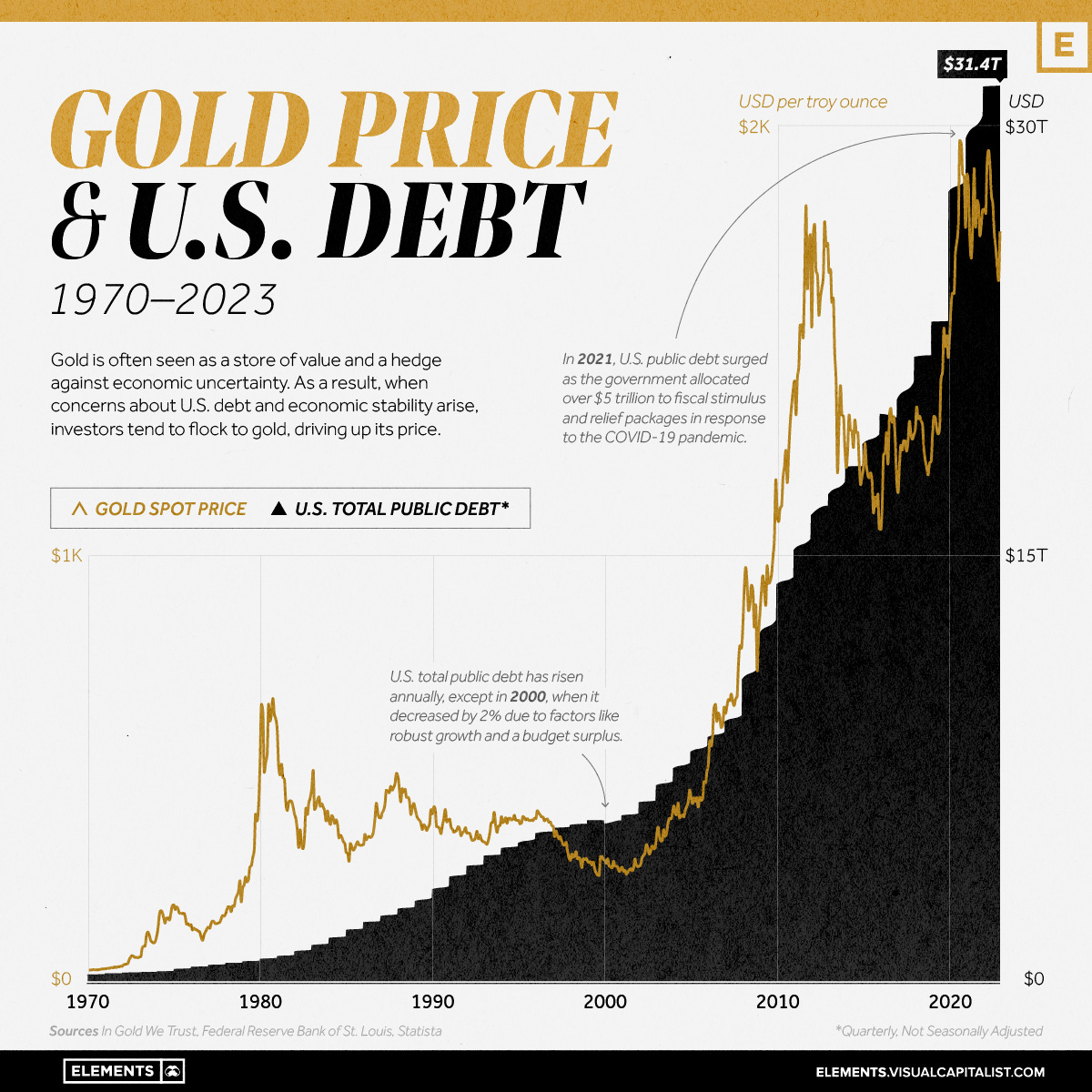

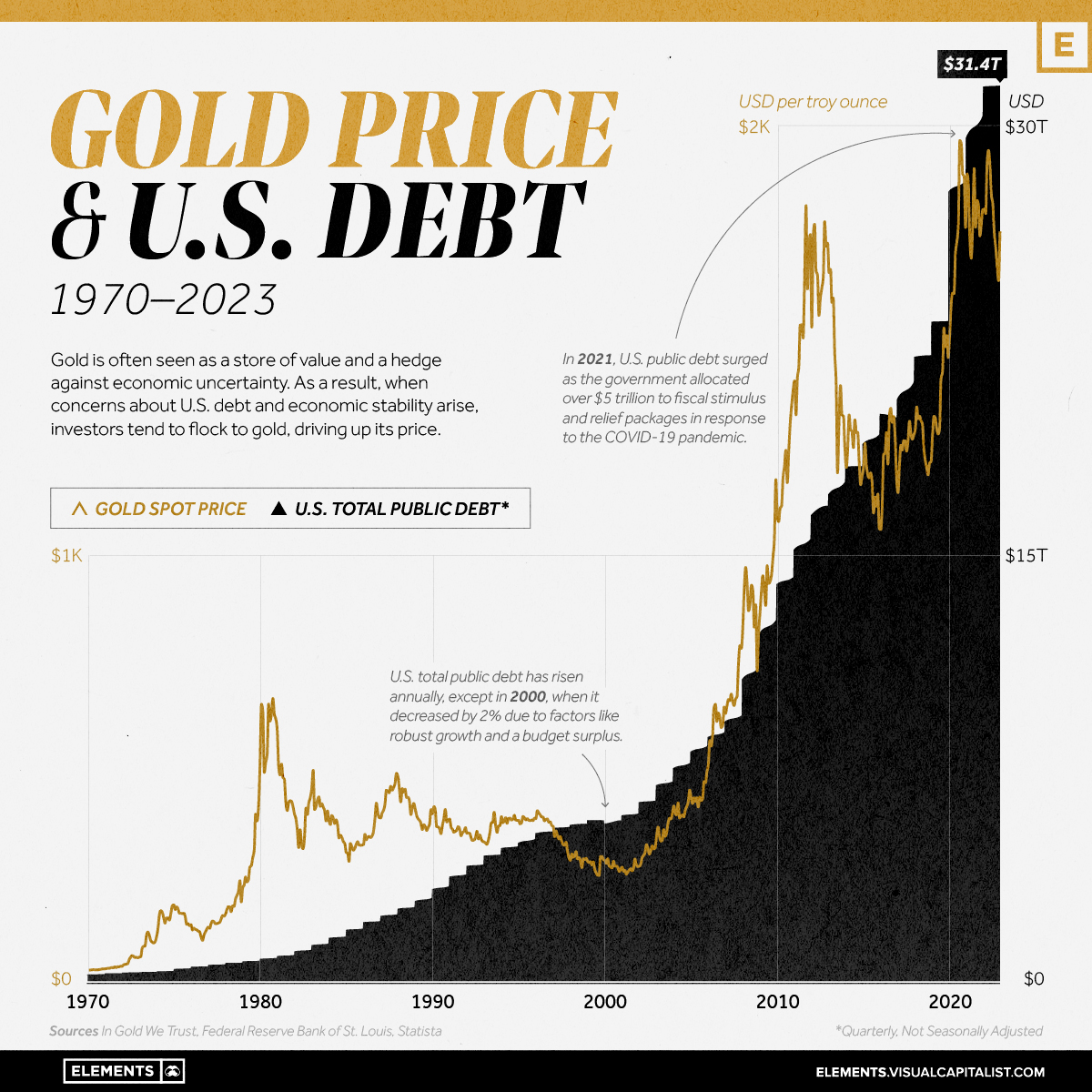

The freezing of approximately $300 billion in Russian Central Bank reserves in February 2022 was the Rubicon moment. Not because of what it did to Russia (Moscow had already been building buffers since 2014, and pivoted quickly to a shadow fleet of 350 tankers and Chinese yuan settlement). The real damage was epistemic: every non-aligned central banker on the planet watched the world’s “risk-free” reserve asset get confiscated because of a political disagreement, and recalculated.

The response has been staggering.

Central banks purchased 1,082 tonnes of gold in 2022, the highest since records began in the 1950s. They followed that with 1,037 tonnes in 2023 and 1,045 tonnes in 2024: three consecutive years above 1,000 tonnes, a pace roughly double the prior decade’s average. In 2025, despite gold hitting multiple record highs (surpassing $4,000 per ounce), central banks still added 863 tonnes, with the National Bank of Poland leading at 102 tonnes. The World Gold Council’s 2025 survey found that 95% of respondents expected global gold reserves to increase over the next year; a record 43% planned to increase their own holdings.

Source: World Gold Council / Metals Focus

None planned to reduce them.

This isn’t portfolio diversification. This is strategic de-dollarization with a very specific catalyst: the demonstration that the “rules” can be changed retroactively when Washington decides it’s convenient.

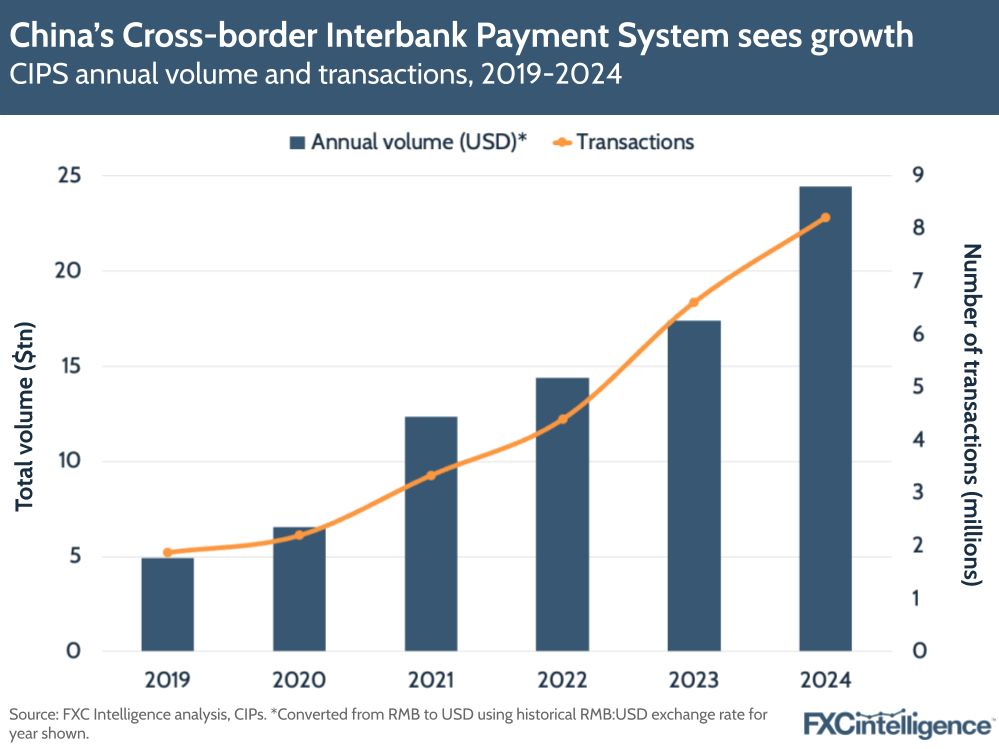

As I wrote in BRICS: A Ghost Threat?, the BRICS bloc itself remained largely toothless, lacking the institutional depth and payment infrastructure to mount a real challenge to dollar dominance. They couldn’t make a fiat to compare with the greenback. But the ghost is becoming corporeal in other ways.

China’s Cross-Border Interbank Payment System (CIPS) now connects over 1,400 financial institutions across more than 100 countries, with transaction values growing by 75% in 2021 alone. It’s still a fraction of SWIFT’s 11,000 member network, and it still relies partly on SWIFT messaging for cross-border settlement, making it vulnerable. But the trajectory is unmistakable: every sanction, every asset freeze, every SWIFT ejection accelerates the migration.

De-globalization doesn’t mean less trade. It means less efficient trade. Supply chains are being rerouted along geopolitical fault lines, and the bottlenecks are already screaming in the data. What follows is a survey of the critical chokepoints that will define the investment landscape for the next decade.

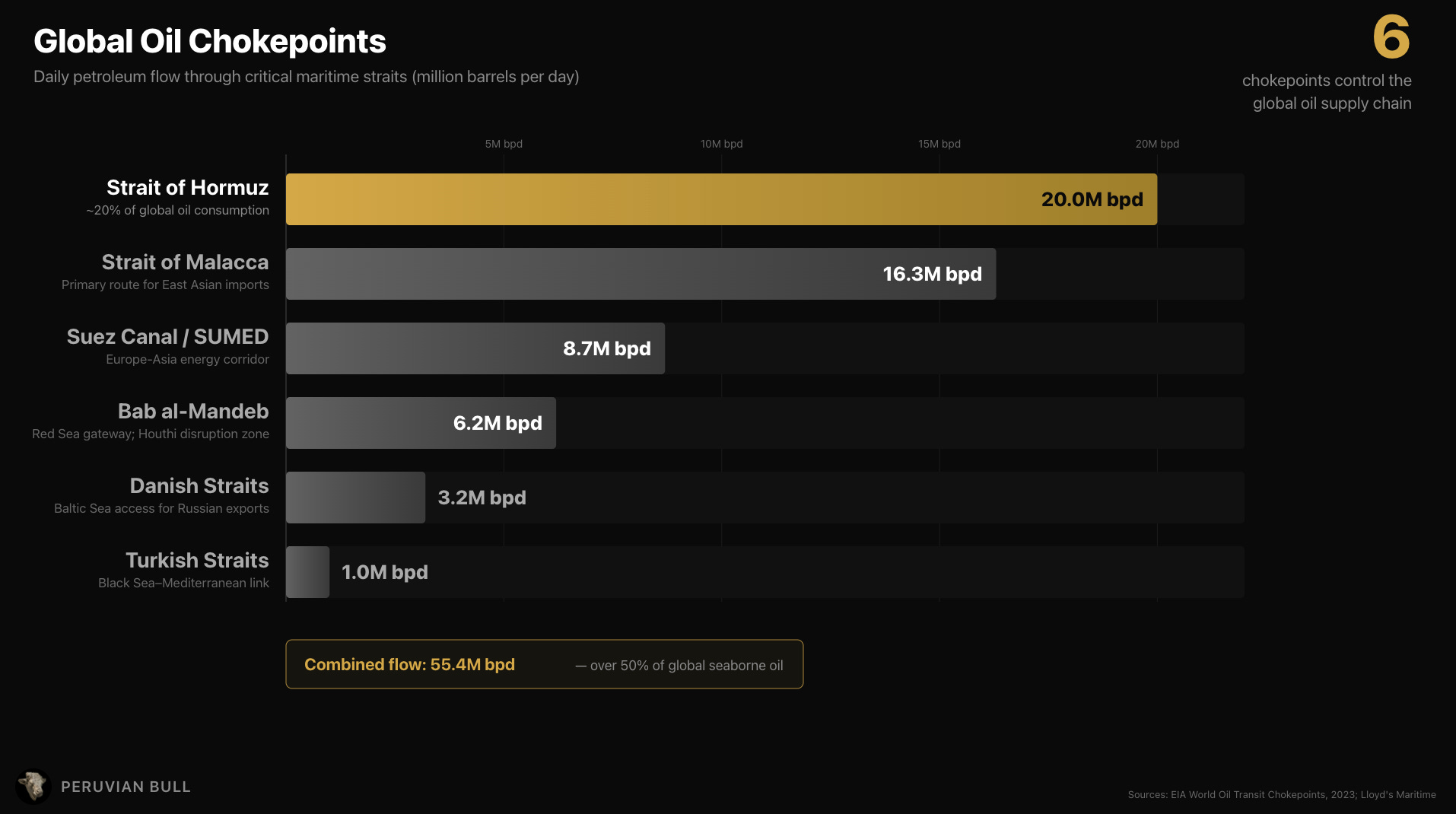

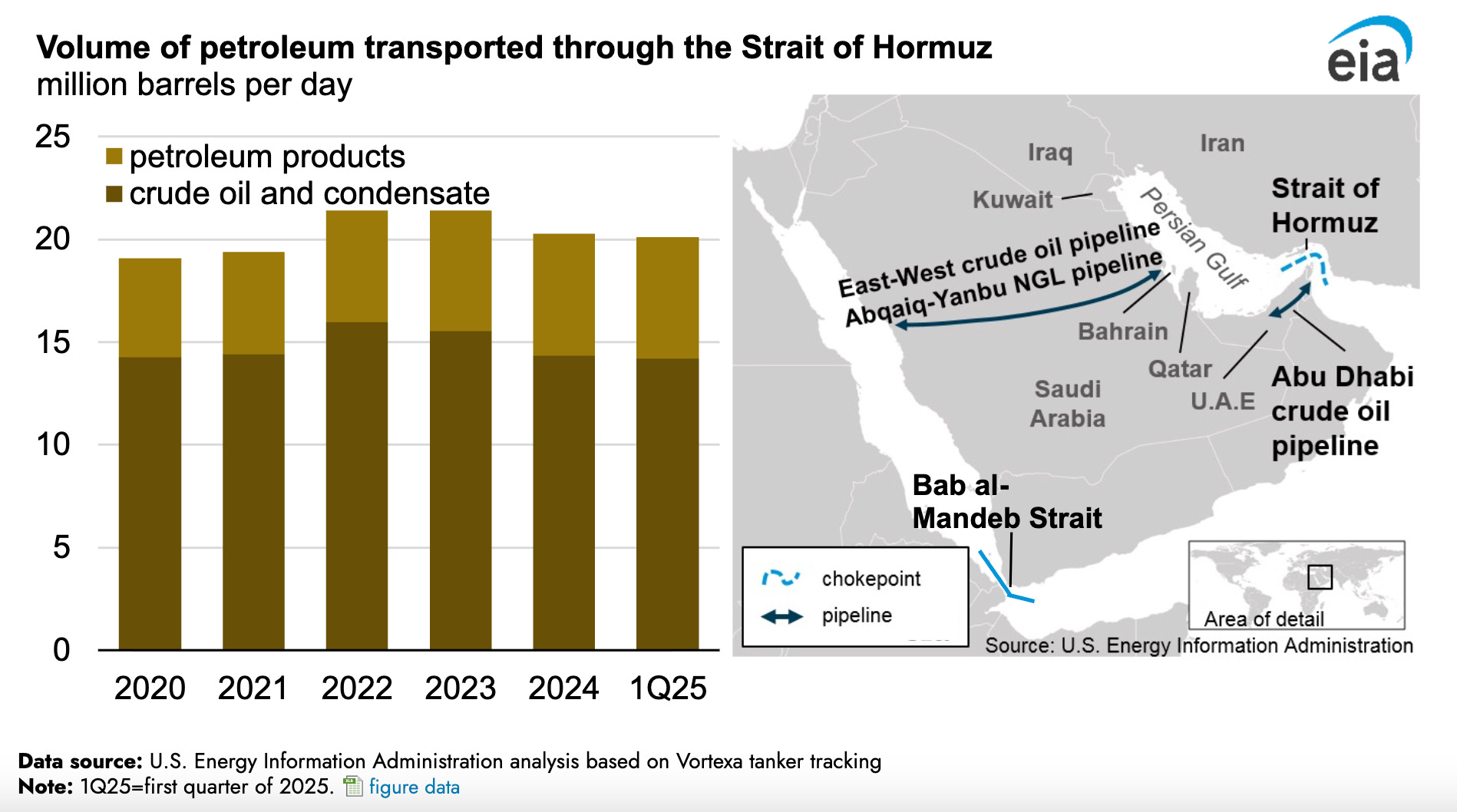

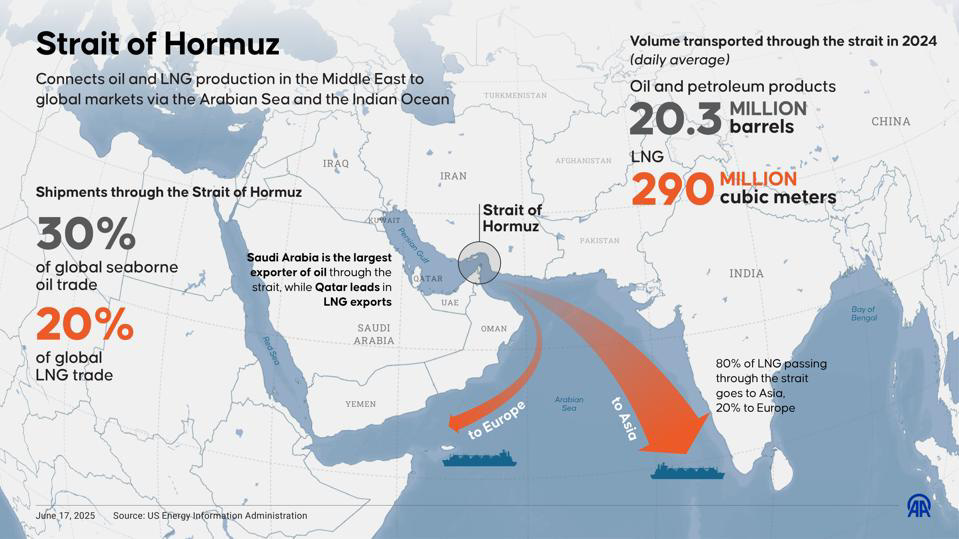

The immediate crisis is obvious. The Strait of Hormuz: roughly 100 miles long, 21 miles wide at its narrowest navigable point, with two-mile shipping lanes in each direction.

Through this passage flows approximately 20 million barrels per day of oil, representing about 20% of global petroleum liquids consumption and over a quarter of all seaborne oil trade. Asian economies are catastrophically exposed: China receives 37.7% of all crude transiting the strait, India 14.7%, South Korea 12%, Japan 10.9%.

Saudi Arabia and the UAE have bypass pipelines (the East-West Pipeline at 5 million bpd capacity and the Abu Dhabi Crude Oil Pipeline at 1.5 million bpd), but combined, they can only reroute roughly a third of total Gulf export flows. Iraq, Kuwait, and Qatar have no comparable alternatives. That leaves close to 14 million barrels per day structurally tied to a single maritime passage with no parallel infrastructure capable of absorbing the displaced volume.

As I write this, Brent crude has surged above $82 per barrel, up over 12% in a week, with European natural gas prices soaring 60% after Iranian drone attacks disrupted Qatar’s LNG operations. And this is with the “measured” reaction traders expect to be short-lived. What happens if it isn’t?

Source: CNBC / Trading Economics

The Strategic Petroleum Reserve, which the Biden Administration drained from 638 million barrels to roughly 370 million, has barely been refilled. OPEC+ agreed to a modest 206,000 barrel per day increase at an emergency meeting, but that’s a rounding error against the potential loss of millions of barrels per day if Hormuz remains effectively shuttered. S&P Global’s Jim Burkhard put it bluntly: if the reduction in tanker traffic continues for a week, “it will be historic. Beyond that, it would be epochal for the oil market.”

If oil is the crisis of the moment, copper is the crisis of the decade. And almost nobody in mainstream finance is talking about it with the urgency it deserves.

SPONSOR:

Taking self-custody of your Bitcoin has never been more critical, and that’s exactly why the team at Blockstream has created the perfect solution: the Jade Plus hardware wallet.

Use Code PB10 for 10% off your JadePlus Wallet! Click the Link here.

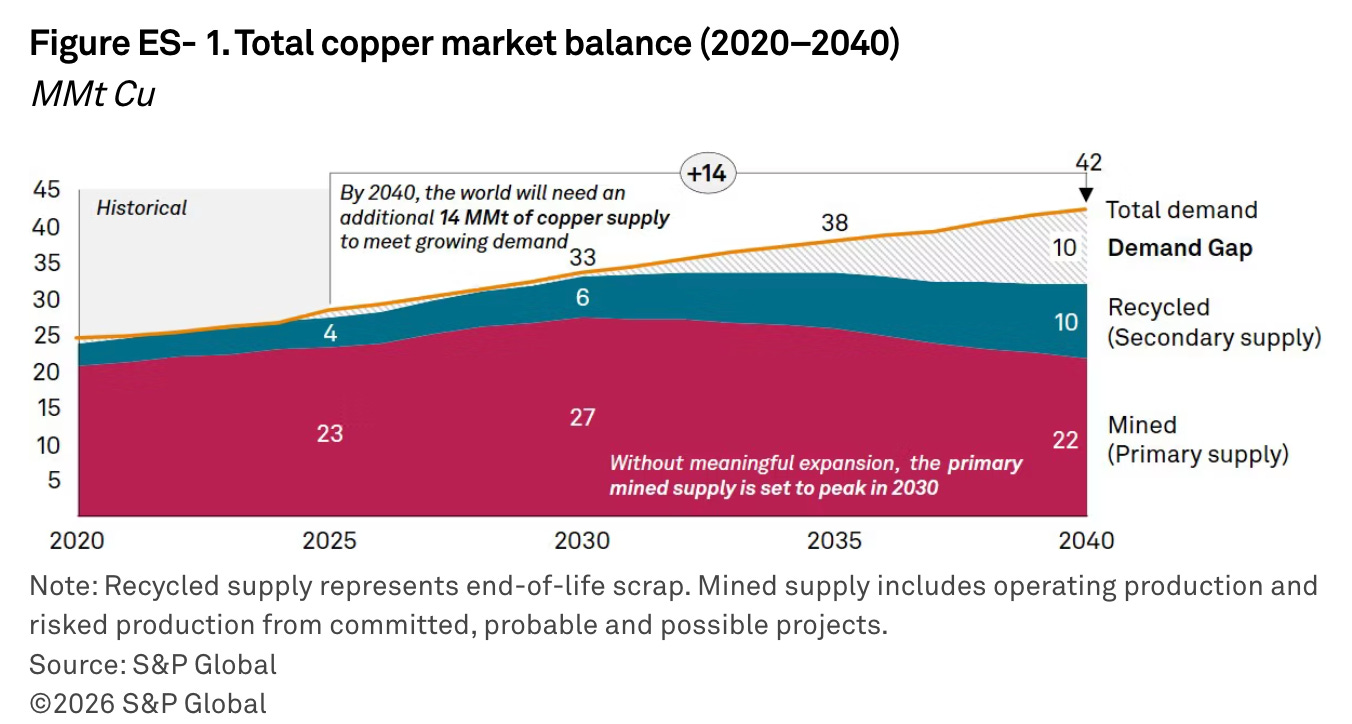

In January 2026, S&P Global released a comprehensive study titled “Copper in the Age of AI” that should have been front-page news everywhere.

The findings: copper demand is projected to reach 42 million metric tons by 2040, a 50% increase from current levels. Global production is expected to peak at 33 million metric tons in 2030 and then decline. The resulting supply gap: 10 million metric tons, or 23.8% of projected demand. Daniel Yergin, vice chairman at S&P Global, put the dilemma perfectly: “Copper is the great enabler of electrification, but the accelerating pace of electrification is an increasing challenge for copper.”

Separately, the International Energy Agency warned at the Critical Minerals Association conference in December 2025 that a 30% supply shortfall could materialize by 2035. The IEA’s critical minerals analyst, Shobhan Dhir, singled out copper as the mineral they’re “really concerned about,” noting that declining ore grades, rising capital costs, and 17-year average mine development timelines make rapid scaling effectively impossible.

Wood Mackenzie’s projections are equally stark: copper demand surging 24% to 42.7 million tonnes per annum by 2035, requiring more than 8 million tonnes of new mine capacity and 3.5 million tonnes from scrap.

Source: S&P Global, “Copper in the Age of AI” (January 2026)

Chile produces about 25% of global copper output. Peru adds another 10-12%. Together, these two countries anchor roughly 40% of mine supply, and both face water shortages, political instability, permitting delays, and environmental opposition. The DRC, the fastest-growing major producer, is increasingly in China’s orbit. The United States designated copper as a critical mineral in November 2025, tacitly acknowledging the strategic vulnerability. As Wood Mackenzie’s Charles Cooper warned: “If governments and investors fail to act, we risk turning the metal of electrification into the metal of scarcity.”

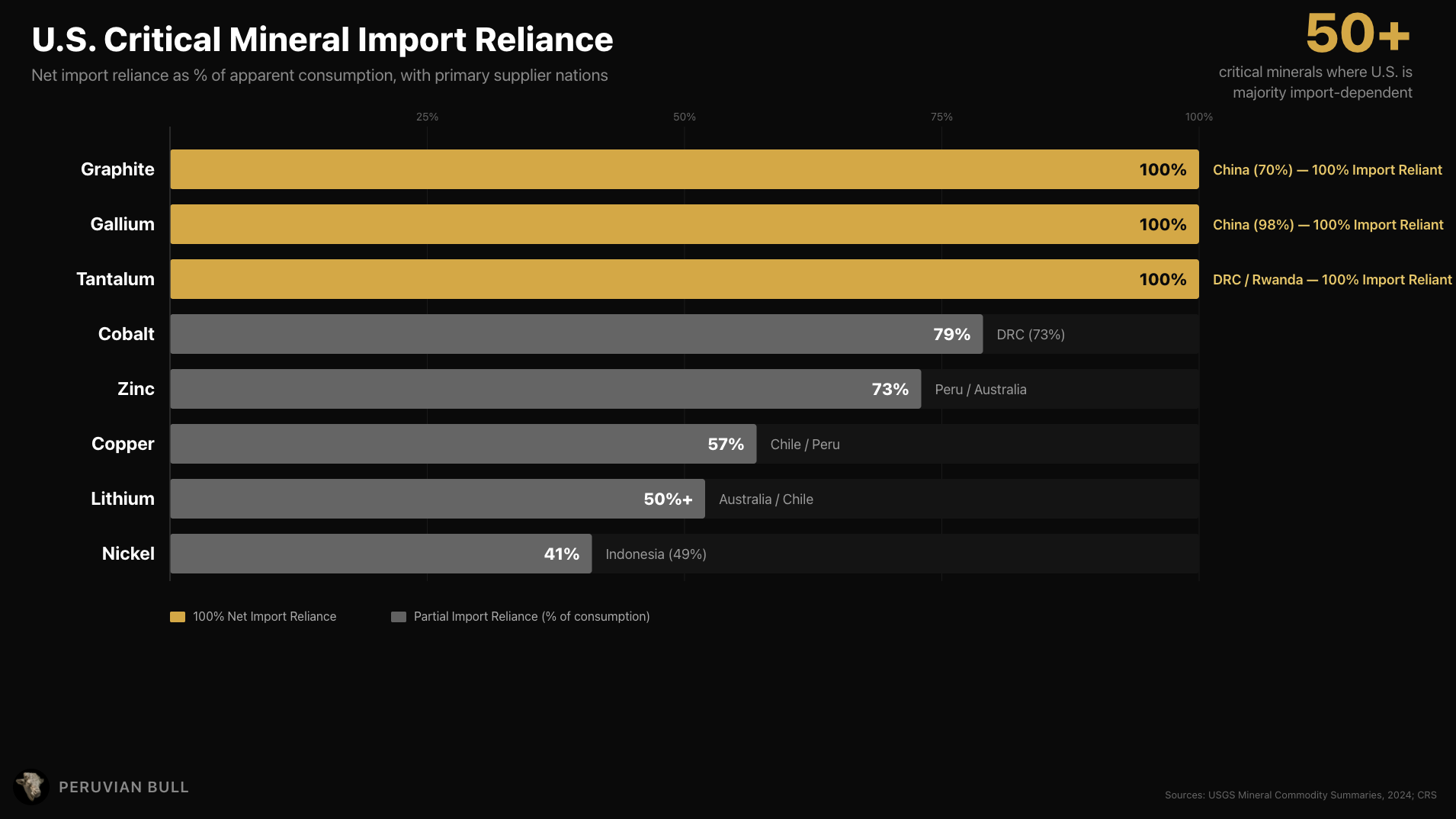

The commodity story extends well beyond energy metals. China controls more than 60% of global rare earth mining and roughly 90% of processing. Since 2023, Beijing has imposed export restrictions on gallium, germanium, and antimony, materials critical to semiconductors, night-vision technology, and armor-piercing munitions. The IEA’s December 2025 assessment found that removing China from supply calculations leaves the rest of the world able to meet only half its own demand for battery metals and rare earths.

Source: U.S. Geological Survey

This isn’t just an economic inconvenience. When the IEA’s Shobhan Dhir warns that the share of the top three refiners for major energy minerals climbed from 82% in 2020 to 86% in 2024, with “virtually all additional dominance accruing to the largest player,” he’s describing a weapon. And the largest player is China. Global defense spending could double to $6 trillion by 2040 according to S&P Global, and every advanced weapon system, every drone, every guided missile requires materials that flow through Chinese processing bottlenecks.

The irony would be darkly comic if it weren’t so consequential: the United States is fighting wars to secure commodity supply chains while simultaneously depending on its primary strategic competitor for the materials needed to build the weapons it’s fighting with.

Here is where the analysis converges on what matters most: your portfolio.

Every conflict, every export restriction, every supply chain rerouting adds friction. And friction, in an economic system, manifests as inflation. Not the “transitory” variety that the Fed insisted on in 2021, but the structural kind that embeds itself into the cost basis of everything.

Consider the transmission mechanism from the current Iran conflict alone.

Oil at $82 and rising flows directly into gasoline prices: the national average was $3.00 per gallon before the strikes. Transport costs rise; they get passed to consumer goods.

Natural gas surges 60% in Europe, pushing electricity costs higher, which raises manufacturing input costs, which feeds through to finished goods. Insurance premiums for shipping through the Persian Gulf are already spiking, adding basis points to the cost of every commodity that touches saltwater.

Now layer on the copper deficit.

Every EV, every solar panel, every data center, every grid upgrade costs more as copper prices climb above $13,000 per metric ton (fresh records as of January 2026). Silver at $80+ raises the cost of every solar cell, every electronic contact, every medical device. Rare earth restrictions raise the cost of permanent magnets, which go into everything from wind turbines to F-35 engines.

Source:Visual Capitalist

{kind=link}

This is the environment in which the Federal Reserve is trapped. The Fed has already lost control of its balance sheet to fiscal dominance. The Treasury needs to fund $2+ trillion annual deficits, and interest expense on the national debt now exceeds defense spending. Any aggressive tightening to fight commodity-driven inflation would blow out the deficit further through higher interest costs, crash the housing market (again), and trigger a recession that would ironically force... more QE.

It’s like slamming the gas and the brakes on the train at the same time.

The postwar order that enabled frictionless global trade, just-in-time supply chains, and the suppression of commodity prices through financialization is over. We are entering a period where physical possession of critical resources matters more than contractual claims on them. Where central banks buy gold not for “diversification” but for sovereign survival.

The world is fracturing along geopolitical lines, and the fractures run right through the commodity supply chains that the global economy depends on. Every fracture is inflationary. Every inflationary impulse forces the central banks deeper into the trap.

And every step deeper into the trap makes hard assets more valuable in relative terms.

Can you smell that? The printer is warming up.

And this time, Jerome won’t even get to pretend he had a choice.

Nothing on this Post constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person.

Nothing stops the Fed inflation train, but its increasingly looking like nothing stops the AI deflation train either. Looking forward to more of your content as these two trains collide.