The Mirage

The war is over, oil is falling, and the S&P 500 just hit another all-time high. At some point you have to ask: what exactly is the market pricing?

Pull up any financial terminal right now and you’ll see green. The S&P 500 was up 1.53% yesterday. The Nasdaq surged past 2%. Oil is falling.

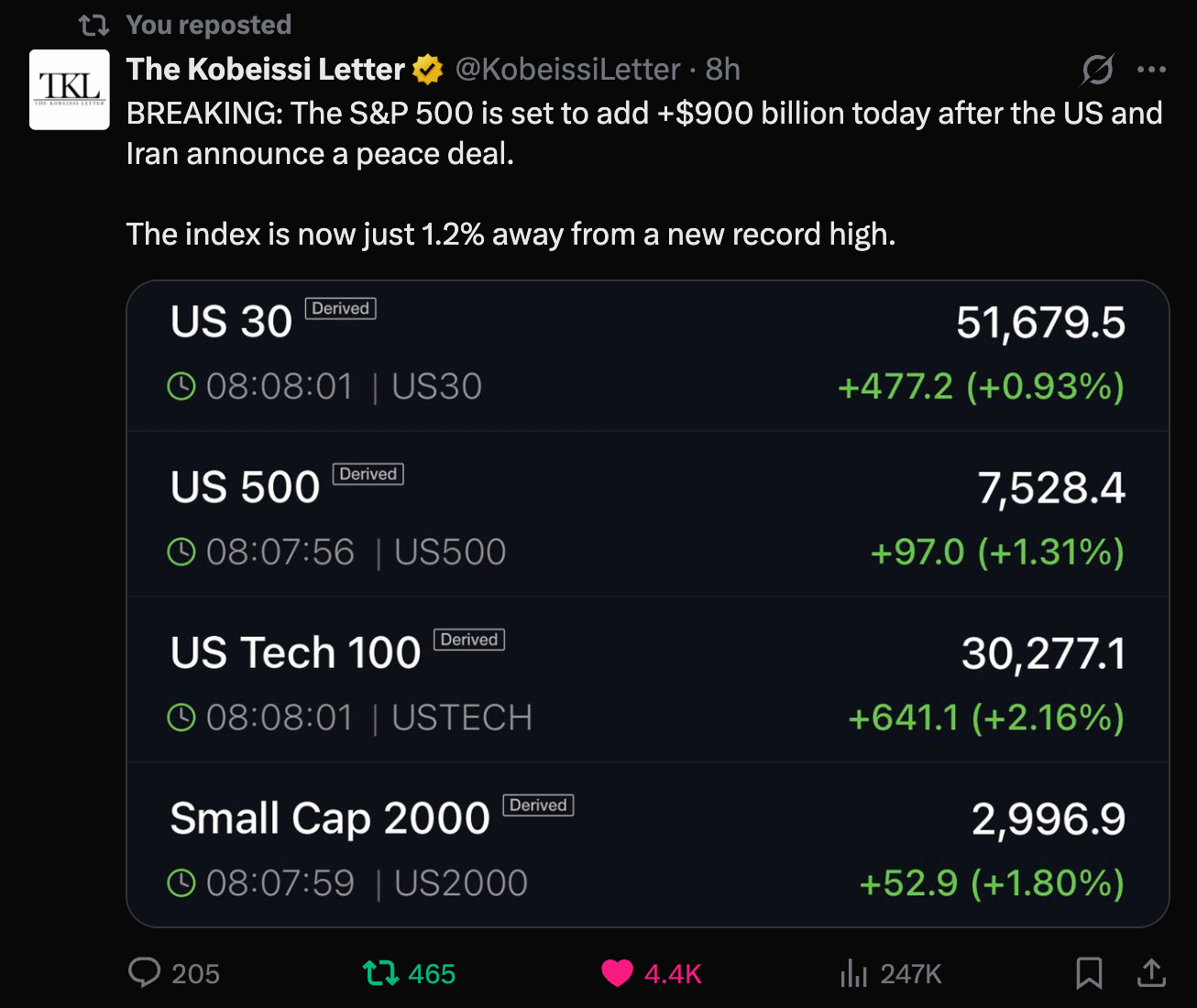

Trump posted a Truth Social over the weekend announcing a “tentative peace deal” with Iran, and by Monday morning the algos had already decided the world was fixed. The Dow went up over 385 points. XLK, the tech ETF, ripped 3.15%. CNBC has the war graphic replaced with a peace graphic and is running a segment on the soft landing.

I’ve been watching financial markets long enough to recognize this feeling. It’s the feeling of a room full of people who’ve been holding their breath for four months, finally exhaling.

The problem is what they exhaled into.

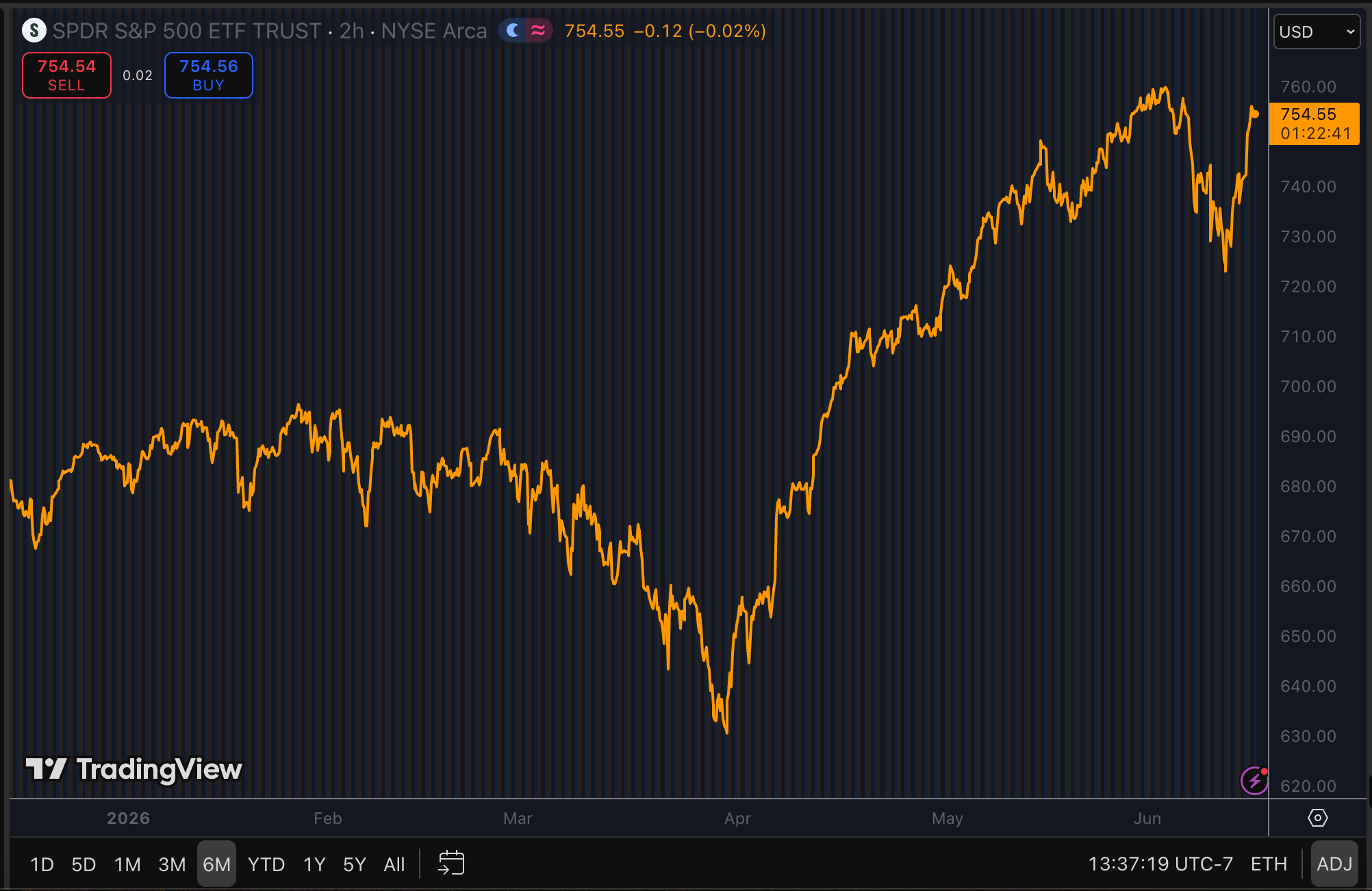

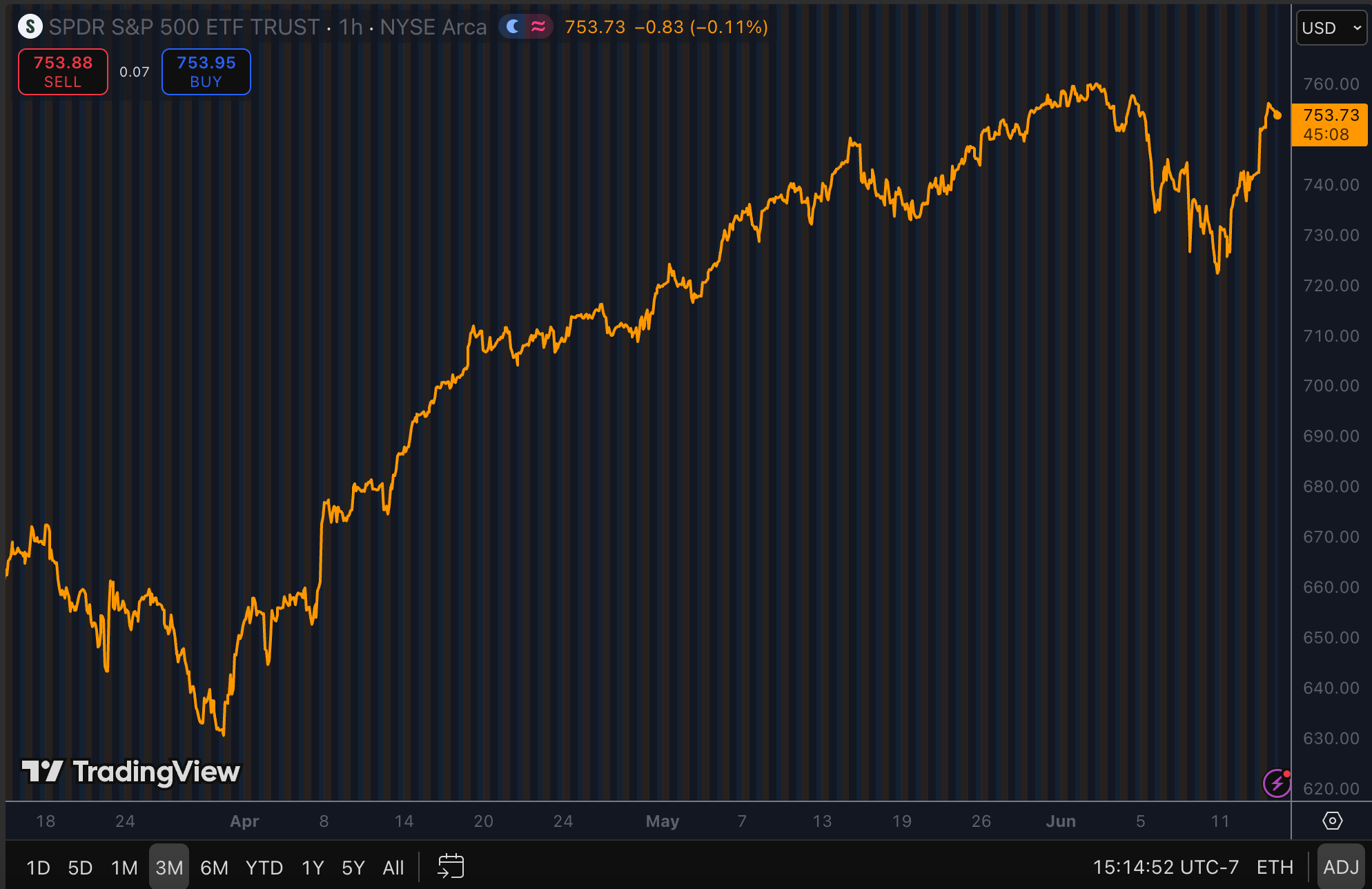

The S&P 500 is up 10.2% since the Iran war began in February.

Through the oil shock, the Hormuz closure, three months of re-accelerating inflation, and Treasury auctions in March that were quietly the weakest in years. The stock market went up through all of it. And now that the shooting has mostly stopped, it’s going up more.

The fact that equities shrugged off one of the largest macroeconomic deteriorations of the decade, and then rallied harder when it ended is crucial.

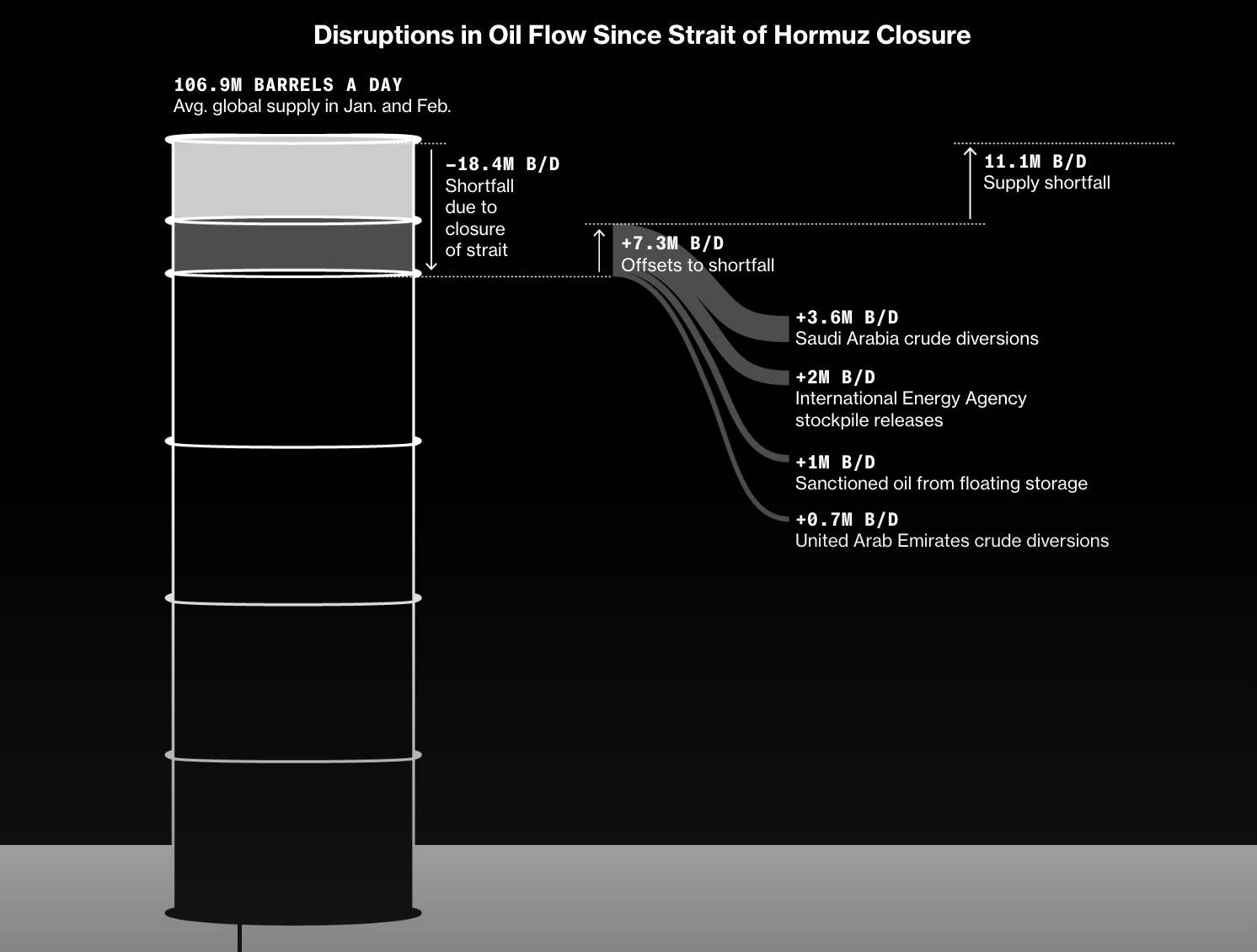

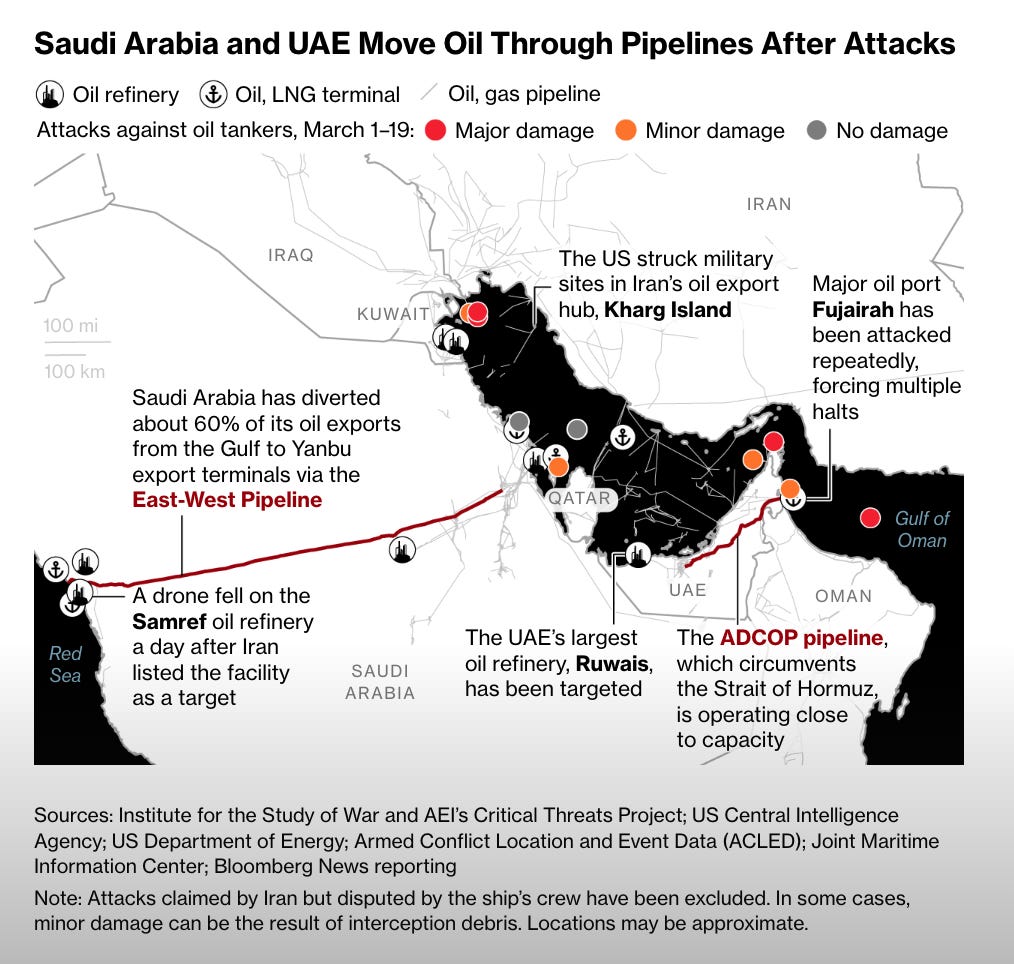

On February 28th, coordinated US-Israeli strikes hit Iranian nuclear facilities under “Operation Epic Fury.” The Iranian Revolutionary Guards responded the way by declaring the Strait of Hormuz closed and attacking civilian shipping, a chokepoint through which roughly 20% of all global oil trade passes every single day.

The economic transmission was immediate. Bloomberg tracked US CPI rising from 2.4% in February to 3.4% in March, with estimates approaching 3.8% by April. The Fed, which spent most of 2025 congratulating itself on its victory over inflation, revised its PCE forecast up to 2.7% for the year and sat on its hands at 3.5-3.75%, unable to hike into a supply shock and unable to cut while re-accelerating prices made that politically impossible.

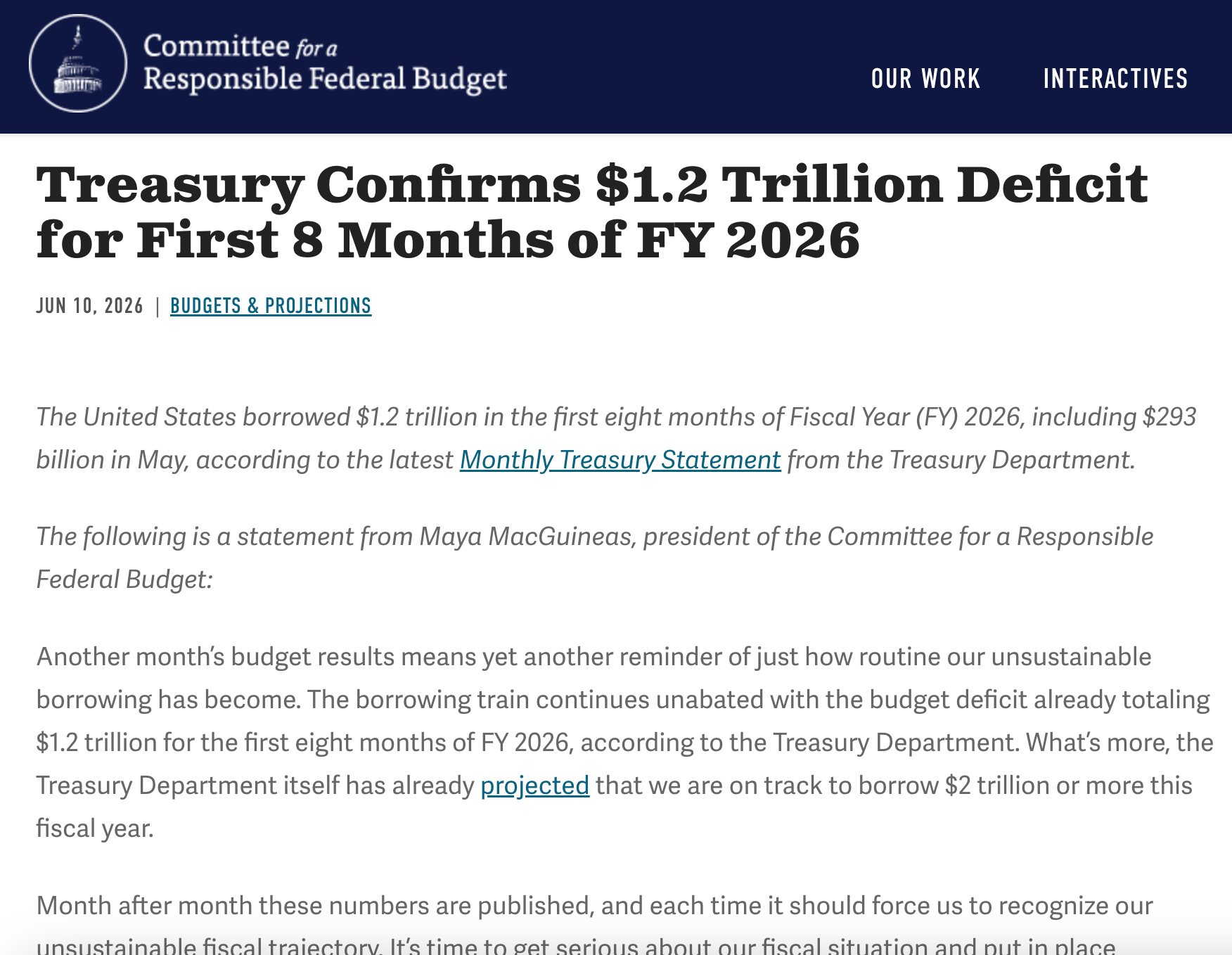

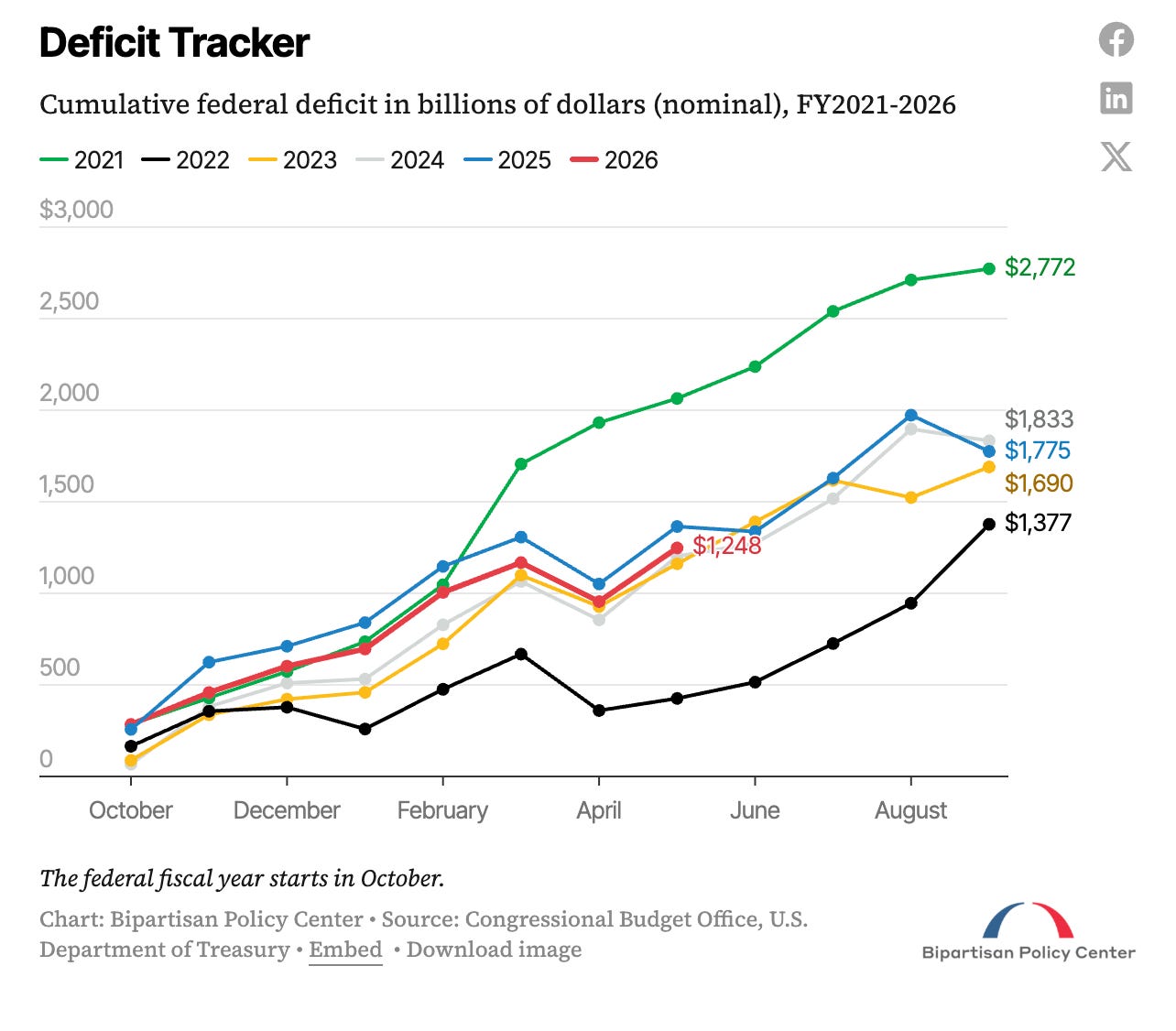

The IMF cut its 2026 global growth outlook from 3.3% to 3.1%. The US ran $1.2 trillion in deficit spending in just eight months, while publicly held debt crossed 100% of GDP in March for the first time. And in that same month, quietly, primary dealers absorbed 24% of a 2-year note auction, roughly twice their normal share; a stress signal in the Treasury market that virtually nobody in the financial press reported on.

Every single one of those data points represents a deterioration from where we started the year: Inflation higher, growth lower, fiscal position worse, monetary policy frozen, Treasury market under strain.

And the S&P 500 finished the period up 10.2%.

That is not a resilience story, it’s a disconnection story. And the peace deal euphoria you’re watching today is just the latest chapter in it.

When Operation Epic Fury began, large institutional investors and hedge funds didn’t just sell equities; they built substantial short positions and bought protection at scale. Charles Schwab’s analysts noted that hedge fund short positioning reportedly increased significantly through the war phase, with several broker-dealers flagging large defensive books being constructed across equities and airline stocks. Options markets priced in tail risk. Energy calls got bid up. The VIX spiked nearly 20% in a single week when the Hormuz closure became clear.

The baseline positioning entering April was deeply defensive: short the market, long oil, hedge everything.

Then on April 7th, Trump announced the two-week ceasefire. The next morning, the Dow gained more than 1,300 points, its best session since April 2025. Nvidia, Meta, Tesla, AMD, and Micron each surged between 4% and 10%. Delta soared 6% after posting earnings that morning.

The energy sector gave back a chunk of its war gains overnight.

Nothing changed about the economy in those 24 hours.

Oil was still elevated, inflation was still running above 3%, and the fiscal deficit was still on its way to $2 trillion. What changed was that the specific tail risk every fund had hedged against, a sustained Hormuz closure producing an uncapped energy price spiral, contracted suddenly. And when a crowded defensive positioning trade reverses that fast, the short-covering looks indistinguishable from a bull market.

The S&P went on a nine-week winning streak. Record close on April 15th. Record close on April 21st. Record close in May. The market didn’t re-rate the economy upward; it re-rated the tail risk probability downward. Those are completely different things.

The sector rotation makes this explicit.

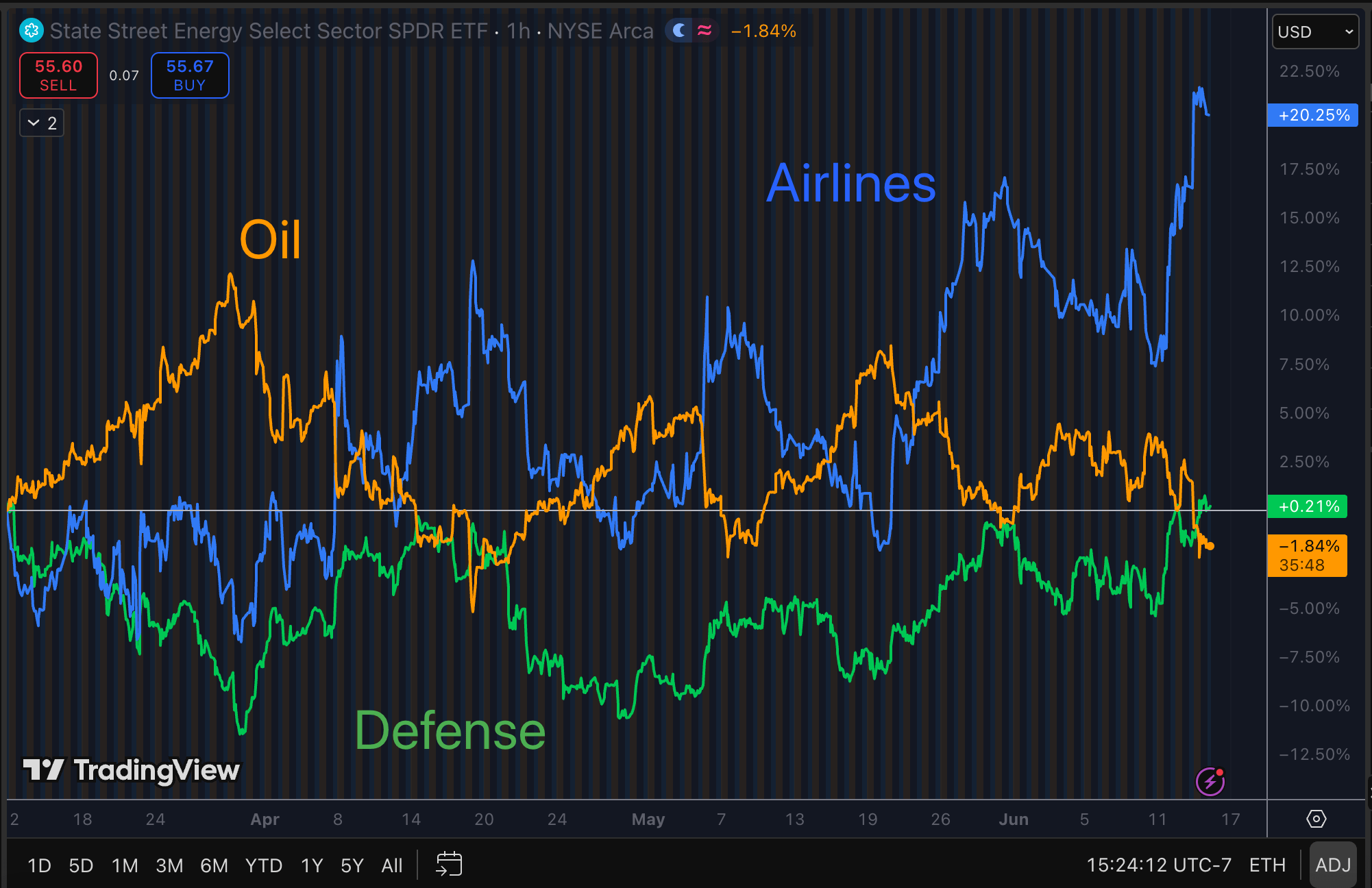

Energy was up nearly 30% through the war phase; since the ceasefire it’s given back nearly 4%. Airlines were down almost 19% during the war; they’re up 22% since. Defense names mirror it exactly.

The money didn’t flow into sectors pricing in a stronger economy; it rotated out of the sectors that had been pricing in a specific geopolitical risk. That’s not fundamental re-rating. That’s positioning unwind.

Today’s move is the same thing, one level up. The peace deal announcement sent Technology up 3.15% while Energy fell 3.75%. The market is pricing out the last remaining war premium. When that premium is fully gone, what’s left is the underlying bid: the structural, liquidity-driven, positioning-sensitive market that existed before February 28th and will exist after June 15th.

But where is that bid coming from?

The prevailing explanation for equity resilience will point to earnings.

SPONSOR:

Bitcoin is freedom money, but only if you control your keys.

Partnering with Bitcoin Well, the world’s first publicly traded non-custodial Bitcoin company, ensures this freedom.

They send Bitcoin directly and instantly to your wallet.

No middlemen. No permission needed. Whether you’re stacking sats or making large moves via their OTC desk (Infinite by Bitcoin Well), you remain in control. Self-custody is essential.

Ready to buy Bitcoin the way it was intended? Head to bitcoinwell.com and enable your independence. Use this link https://app.bitcoinwell.com/signup?referral=peruvianbull to sign up and start stacking today!

Now let’s get back to it!

And the earnings data is genuinely strong: 85% of S&P 500 companies beat Q1 estimates versus the five-year average of 78%, with aggregate profit beats averaging 16.7% against the historical 7.3%. That’s not fabricated.

But it requires context: the S&P 500 is now nearly half technology and AI-adjacent companies by market cap, and those companies are structurally insulated from oil price shocks in a way that the broader economy is not. Nvidia doesn’t care if Brent is at $120.

Microsoft’s Azure margins don’t compress when jet fuel spikes. Google Cloud Platform revenues are projected to hit $84.8 billion in 2026, a 44% annual increase, regardless of what happened in the Strait of Hormuz. So when the financial press points to earnings resilience as validation that the market’s war-era performance was justified, they’re using data from the quarter of the economy most insulated from the shock to draw conclusions about the whole economy.

The consumer discretionary sector, airlines, regional banks, small businesses, anyone actually exposed to elevated fuel costs and re-accelerating consumer price pressure: their experience of the last four months looked nothing like Nvidia’s. And those names are underrepresented in an index that’s been increasingly concentrated in tech for the better part of a decade.

The deeper issue is that the equity market has, for most of the post-2008 era, been a liquidity price rather than an economic price.

As I’ve argued in Net Liquidity and in the Dollar Endgame series, the correlation between the Fed’s balance sheet and S&P performance has run near 0.9 for most of the past decade and a half. If you divide the S&P 500 by the Fed’s balance sheet since the Global Financial Crisis, the line is nearly flat.

(I also covered this in depth in Financial Gravity here on Substack, read this piece for the full explanation)

The real growth in equity prices over that period has been financed by reserve creation, not by productivity gains or fundamental earnings improvement.

The Iran war didn’t break that relationship. It just temporarily introduced geopolitical noise into a market that’s primarily responding to something else: the structural bid that flows from trillions of dollars worth Fed reserves sitting in the banking system, reaching for yield.

None of that makes the underlying macro situation better. And this is what’s getting lost in the current euphoria.

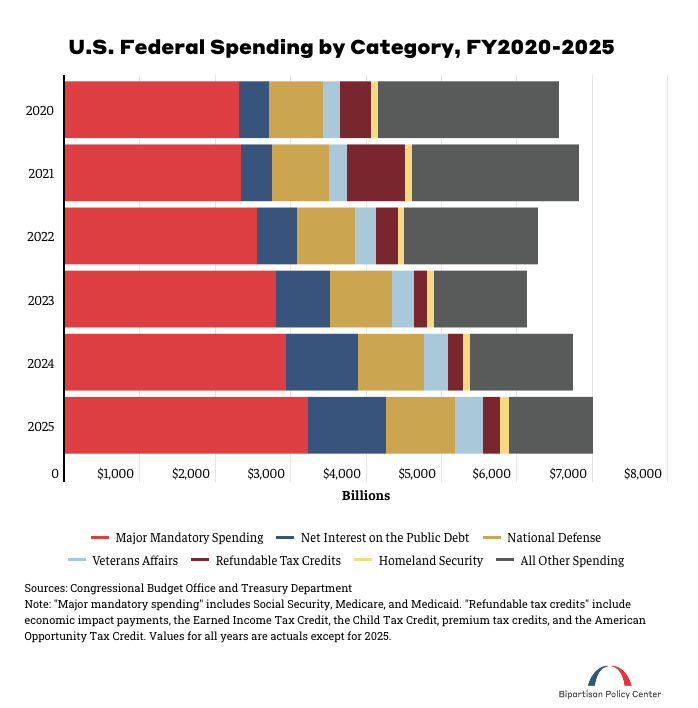

The fiscal position today is worse than it was on February 27th. The federal deficit hit $1.2 trillion in eight months and is on pace for $2 trillion or more for the fiscal year, a figure that reflects war costs, strategic reserve releases, sanctions relief disbursements, and the compounding interest on a national debt that the GAO projects will reach 123% of GDP by 2036. The national debt held by the public crossed 100% of GDP in March- the gross national debt is over 120% of GDP. Interest payments on that debt already exceed defense spending, and are growing much faster than the economy.

None of those facts changed because Trump announced a peace deal on Sunday.

The inflation picture didn’t change either, at least not in the way the market is assuming.

Energy disinflation will show up in coming CPI prints as oil falls; that part is real and it will look positive in the headline numbers. But energy prices filtering through into retail gasoline takes 2-4 weeks, and the transmission of the war’s oil shock into service costs, freight rates, manufacturer input prices, and ultimately wages takes months.

Those effects are already embedded in the cost structure of the US economy. They don’t reverse because Hormuz reopened.

Franklin Templeton noted just this week that core inflation continues running above 3% versus the Fed’s 2% target, with the bond market now fully pricing out any 2026 cut and a hike in early 2027 starting to look consensus. A Fed that can’t cut and might be forced to hike is not a supportive backdrop for the P/E multiples the market is currently assigning tech.

The bond market, which tends to be less impressed by geopolitical narrative than equities, is making this exact point. Today, on what equity markets are treating as the best news in months, the 10-year Treasury yield fell just 2 basis points to 4.459%.

The 30-year sits at 4.958%.

If the peace deal were genuinely resolving the macro uncertainty, if inflation was about to sustainably fall back to target and the Fed could return to cutting, yields would drop 10-15 basis points at minimum.

Instead the bond market barely moved. It’s saying: we see the geopolitical headline, we’re not changing our assessment of the underlying inflation and fiscal trajectory.

The equity market is celebrating; the bond market is not. One of them is wrong.

And then there’s the peace deal itself. The June 14-15 memorandum explicitly defers Iran’s nuclear enrichment limits, its highly enriched uranium stockpile, sanctions relief, and frozen asset releases entirely to follow-on negotiations.

The hard questions, the ones that produced this war in the first place, got kicked down the road. This is a 60-day ceasefire extension, not a treaty. Markets are pricing it as resolution. Polymarket has $344 million traded on the permanent peace deal question with the resolution date still genuinely unclear.

The probability that the nuclear enrichment dispute produces another escalation within 12 months is not zero. Equities are pricing it very close to zero.

What the market is pricing is the absence of the bad thing. What it is not pricing is the presence of a good thing. That is not the same situation as a genuine economic improvement, and markets historically do not sustain levels built on the removal of headwinds rather than the emergence of real tailwinds.

I’ve argued in pieces like Printer is Coming and The Taper is Dead that the United States is on a trajectory toward fiscal dominance: the point at which the government’s borrowing needs constrain the Fed’s ability to manage inflation, where the choice between price stability and Treasury market stability gets forced into the open.

The Iran war accelerated that trajectory, but it didn’t create it- and the peace deal doesn’t reverse it.

Jesus Christ. The S&P 500 is that far gone into AI related stocks? Holy shit man