The Puppet Masters

Bitcoin rallied 3.5% today. But the real story is what didn’t happen.

For four months, crypto traders have watched the same movie every morning: Bitcoin pumps overnight during Asian and European sessions, builds momentum, and then gets absolutely slammed right around 10:00 AM Eastern as the US cash market opens. Hundreds of millions in leveraged longs, liquidated and overnight gains erased.

Traders started setting alarms for it. They called it the 10AM Slam.

Today? Silence. No dump. No cascade. Bitcoin ripped through $66,300 while the Fear & Greed Index sat at 11: Extreme Fear. Over $323 million in leveraged positions liquidated, but this time it was the shorts getting squeezed, not the longs getting harvested.

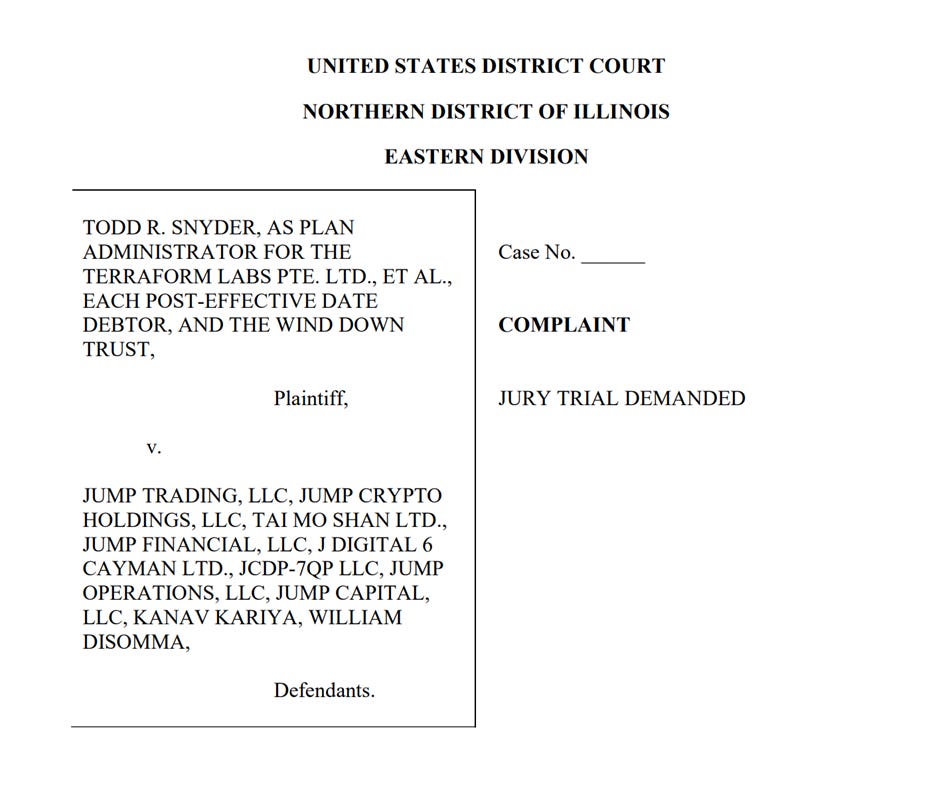

The timing is not subtle. Two days ago, Terraform Labs’ bankruptcy administrator Todd Snyder filed an 83-page lawsuit in Manhattan federal court against Jane Street Group, accusing the firm of insider trading, front-running, and market manipulation during the $40 billion Terra/Luna collapse. The same Jane Street that crypto Twitter has spent months pointing to as the architect of the daily 10AM Bitcoin suppression.

Jane Street’s relationship with Terraform dates back to 2018. Activity surged in 2022 when Bryce Pratt, a former Terraform intern who joined Jane Street in September 2021, allegedly created a private group chat titled “Bryces Secret” with a Terraform software engineer and the head of business development. The lawsuit calls this a back-channel for material non-public information.

May 7th, 2022: Terraform secretly withdrew 150 million UST from Curve3pool, the primary liquidity pool supporting UST’s dollar peg. No public announcement. Within ten minutes, a wallet allegedly linked to Jane Street withdrew an additional 85 million UST from the same pool. 235 million dollars yanked in ten minutes. Regular traders had zero warning.

The combined withdrawal crushed the pool. UST depegged. LUNA hyperinflated from $80+ to zero in days, and $40 to $50 billion was destroyed. The contagion triggered Three Arrows Capital, Voyager Digital, and contributed to the chain reaction that brought down FTX.

SPONSOR: Bitcoin is freedom money, but only if you control your keys.

Partnering with Bitcoin Well, the world’s first publicly traded non-custodial Bitcoin company, ensures this freedom.

They send Bitcoin directly and instantly to your wallet.

No middlemen. No permission needed. Whether you’re stacking sats or making large moves via their OTC desk (Infinite by Bitcoin Well), you remain in control. Self-custody is essential.

Ready to buy Bitcoin the way it was intended? Head to bitcoinwell.com and enable your independence. Use this link https://app.bitcoinwell.com/signup?referral=peruvianbull to sign up and start stacking today!

Now let’s get back to it!

On May 9th, as the depeg accelerated, Pratt initiated a group message with Do Kwon and Jane Street representatives, expressing interest in bidding on Luna or Bitcoin. Kwon replied that Jump Trading co-founder Bill DiSomma should have already contacted them regarding a Terraform fundraise. This reads less like a rescue offer and more like a firm positioning itself while holding all the cards.

Manhattan prosecutors reviewed Telegram chats between Jump, Jane Street, and Alameda about a proposed UST rescue. In December 2025, Snyder filed a separate $4 billion suit against Jump Trading, alleging they “actively exploited” Terraform via a backdoor deal to inflate UST before pulling support. Jump is reportedly in the new Jane Street complaint, accused of leaking insider information.

The lawsuit questions not Kwon’s guilt, but whether Jane Street, knowing the collapse was imminent, used insider advantage to profit before the $40 billion wipeout and subsequent contagion.

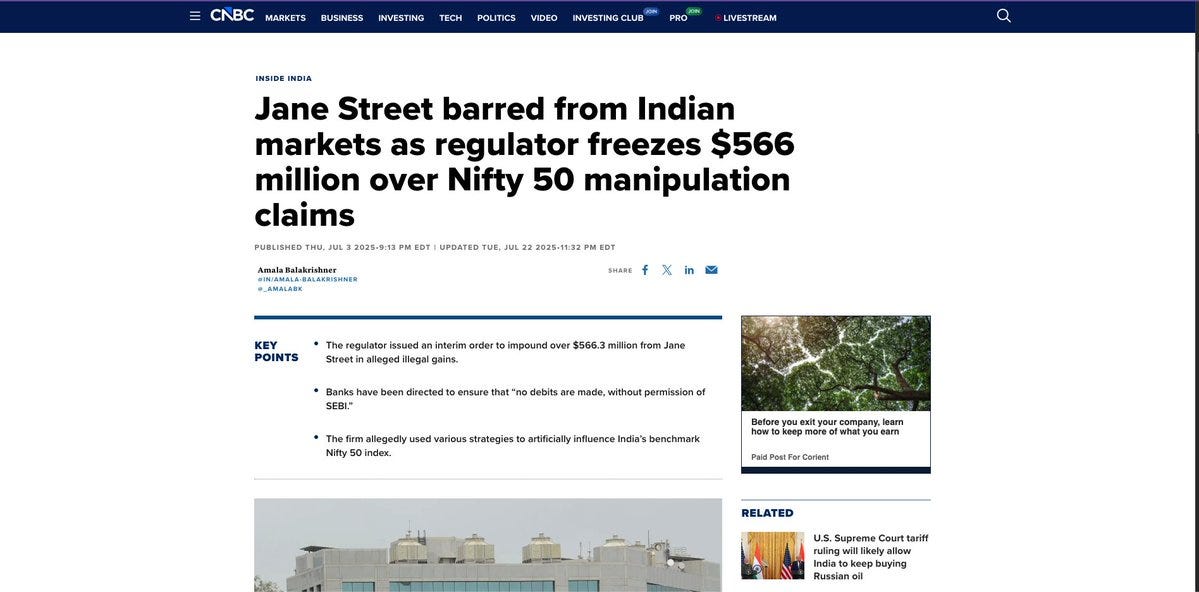

India’s securities regulator also barred it from its markets last July for manipulating the Bank Nifty index. The same Jane Street that serves as the primary authorized participant and market maker for BlackRock’s IBIT, the world’s largest spot Bitcoin ETF.

An insider on crypto Twitter claimed Jane Street was forced to shut down their trading algorithms. Jane Street called the accusations “baseless, opportunistic claims.” But the tape tells a different story. As Coinpedia noted, the 10AM selling pressure paused the day after the lawsuit dropped, and Bitcoin surged.

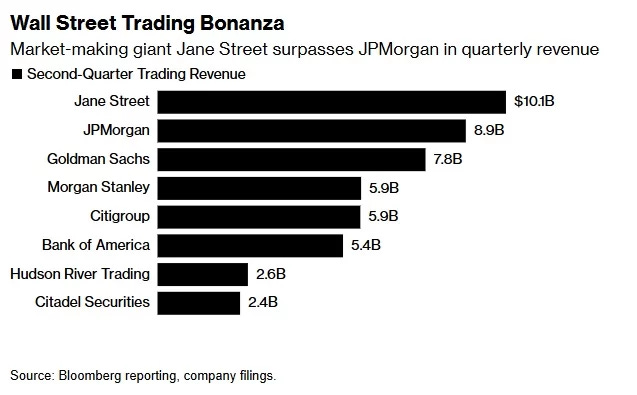

This isn’t an isolated data point. It’s one thread in a pattern stretching across three continents, multiple asset classes, and the better part of a decade, from a single firm that pulled in over $10 billion in net trading revenue in a single quarter.

Let’s pull on the thread.

Most people outside of finance have never heard of Jane Street. That’s by design.

This isn’t Goldman Sachs with CEOs doing CNBC hits and shaking hands with senators. Jane Street operates from 250 Vesey Street in Lower Manhattan with no CEO, no standard hierarchy, no public face. The firm runs like an “anarchist commune,” governed by 30 to 40 senior executives who collectively steer a machine generating more trading revenue than most of Wall Street’s blue chips.

The numbers are staggering. In 2024: $20.5 billion in net trading revenue, $13 billion in net income, surpassing both Bank of America and Citigroup’s entire trading desks. Then 2025 happened. Q2 alone: a record $10.1 billion, beating every major Wall Street bank including JPMorgan at $8.9 billion. Q3: another $6.83 billion.

SPONSOR:

Taking self-custody of your Bitcoin has never been more critical, and that’s exactly why the team at Blockstream has created the perfect solution: the Jade Plus hardware wallet.

Use Code PB10 for 10% off your JadePlus Wallet! Click the Link here.

Through three quarters, $24 billion year-to-date, already exceeding the full-year 2024 record. Jane Street employs roughly 3,000 people. JPMorgan employs over 300,000. The revenue-per-employee math is almost incomprehensible.

Founded in 1999 by four ex-Susquehanna traders, Jane Street started trading ADRs before expanding into ETFs, fixed income, futures, commodities, and options. By 2024, the firm accounted for 41% of all bond ETF trading volume in the US and traded across 200+ venues in 45 countries.

The alumni network tells a story. Sam Bankman-Fried worked at Jane Street until 2017 before founding Alameda Research and FTX, which collapsed in a $32 billion fraud. Caroline Ellison, Alameda’s CEO, also came from Jane Street.

SBF even funneled $400 million from Alameda to Modulo Capital, a hedge fund founded by two former Jane Street traders. The firm wasn’t directly implicated in FTX’s fraud. But it’s served as a finishing school for people who went on to cause catastrophic damage in crypto markets, and the regulatory heat isn’t limited to crypto.

When BlackRock filed its S-1 for a spot Bitcoin ETF in late 2023, two names appeared as authorized participants: JPMorgan Securities and Jane Street. This wasn’t ceremonial. It was structural.

Authorized participants are the only entities that can create and redeem ETF shares. They sit between the spot Bitcoin market and the billions flowing through IBIT. Each creation basket requires delivery of approximately 22.72 bitcoins. The AP is the plumbing.

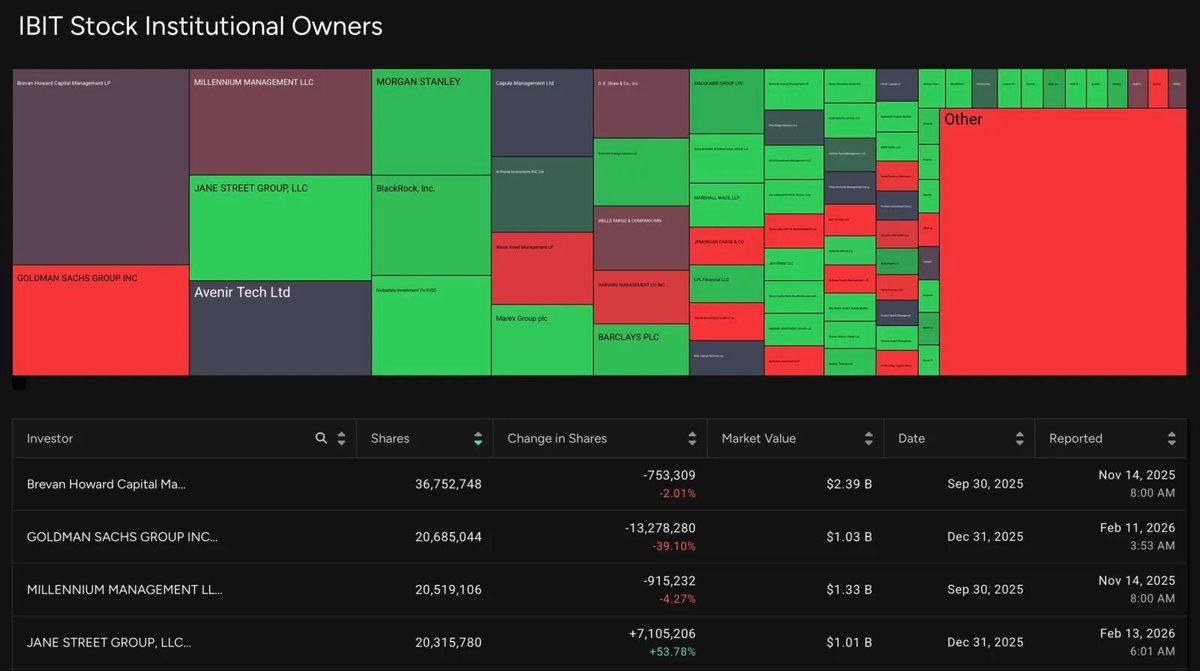

Jane Street’s Q4 2025 13F filing disclosed 20.3 million shares of IBIT (~$790 million), after adding 7.1 million shares ($276 million) in Q4 alone. At peak exposure, nearly $2.5 billion in IBIT. A 13F only shows certain long equity positions; it doesn’t reveal short positions, options books, or futures hedges. As analyst Nik Bhatia put it: Jane Street owns IBIT so it can “write options, arbitrage, and do everything else a quantitative trading shop does to make fast money.”

The AP role gives Jane Street real-time visibility into creation and redemption flows, the ability to arbitrage between spot BTC and ETF NAV, and the structural capacity to influence price in the most liquid hour of the trading day.

This is the same structural advantage that market makers in gold ETFs have exploited for years; the difference is that Bitcoin’s 24/7 trading and extreme leverage environment makes the potential for exploitation even greater.

(Important distinction: Coinbase Custody is the actual Bitcoin custodian for IBIT. Jane Street doesn’t hold the Bitcoin. But as the AP and lead market maker, it doesn’t need to; it controls the flow. It’s the difference between owning the vault and owning the only road to the vault.)

When BlackRock launched IBIT, the crypto world celebrated institutional adoption.

What they didn’t reckon with was what comes packaged with institutional infrastructure: authorized participants, market makers, and HFT desks arbitraging across spot, futures, ETFs, and options simultaneously. The same class of firms that have been caught manipulating gold, silver, interest rates, and equity indices for decades now sit at the center of Bitcoin’s price formation.

From November 2025 through January 2026, spot Bitcoin ETFs shed approximately $6.18 billion in net capital, the longest sustained outflow streak since launch. Total AUM has dropped 30.5% since January, falling from about $117 billion to $81.3 billion. The average cost basis for ETF holders sits around $90,200; with BTC in the mid-$60,000s, virtually every ETF buyer is underwater. This is supposed to be a bull cycle year, one year post-halving. Gold is above $5,000. Silver is ripping. Central banks are accumulating hard assets at record pace. Bitcoin should be participating in this move.

The fact that it isn’t, while the entity with the most structural power over its price discovery is accused of manipulation across three jurisdictions, tells you something fundamental about where we are in the cycle.

Gold was suppressed for decades via the London Gold Pool and bullion bank shorting. JP Morgan’s precious metals desk was convicted of eight years of spoofing, leading to the imprisonment of its heads of Global Precious Metals and Gold Trading for one and two years, respectively. The suppression’s eventual failure caused violent repricing.

After the London Gold Pool collapsed in 1968, gold surged from $35 to $850 in twelve years. When modern suppression cracked in 2024, gold went from $2,060 to over $5,000 in under two years. The longer the suppression, the more violent the repricing across all markets and time periods.

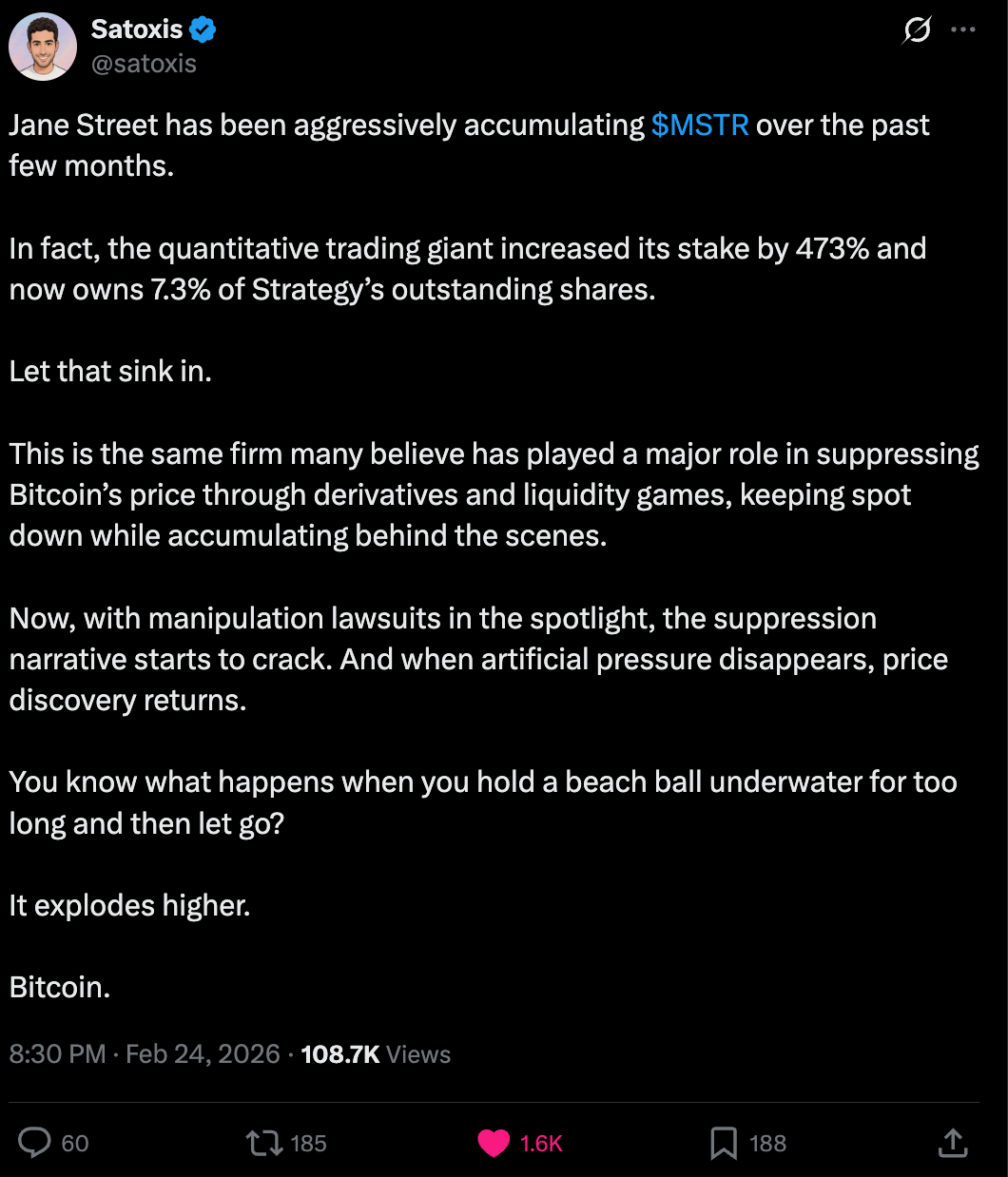

Then there’s MicroStrategy. In that same Q4 filing, Jane Street boosted MSTR holdings by 473%, accumulating 951,187 shares (~$121 million) while BlackRock and Vanguard were divesting billions. MSTR functions as a leveraged Bitcoin proxy holding 717,000+ BTC. Why dump Bitcoin at the cash open every morning while accumulating a leveraged long on the same asset?

The answer only makes sense if you can influence the entry price.

Starting around November 2025, traders documented a near-daily pattern: Bitcoin grinding higher through Asian and European sessions, then getting crushed within 30 to 60 minutes of the US market open.

In December 2025, BTC dropped from ~$89,700 to $87,700 within minutes of the open, liquidating $171 million in leveraged longs. On December 12th, BTC dropped $2,000 in 35 minutes, wiping $40 billion from market cap.

But consider the mechanics. Bitcoin trades 24/7 while IBIT only trades US hours.

This creates a daily window where the ETF must “catch up” to overnight spot moves. If an authorized participant knows the flows, it can sell aggressively into the open, trigger stop-losses and liquidations across the leveraged long complex (over $93.5 billion in crypto futures open interest heading into this week), buy back cheaper, fill creation orders at the depressed price, and pocket the spread. A 2% dip liquidates hundreds of millions. For a firm with Jane Street’s balance sheet, engineering that dip at a predictable time is routine.